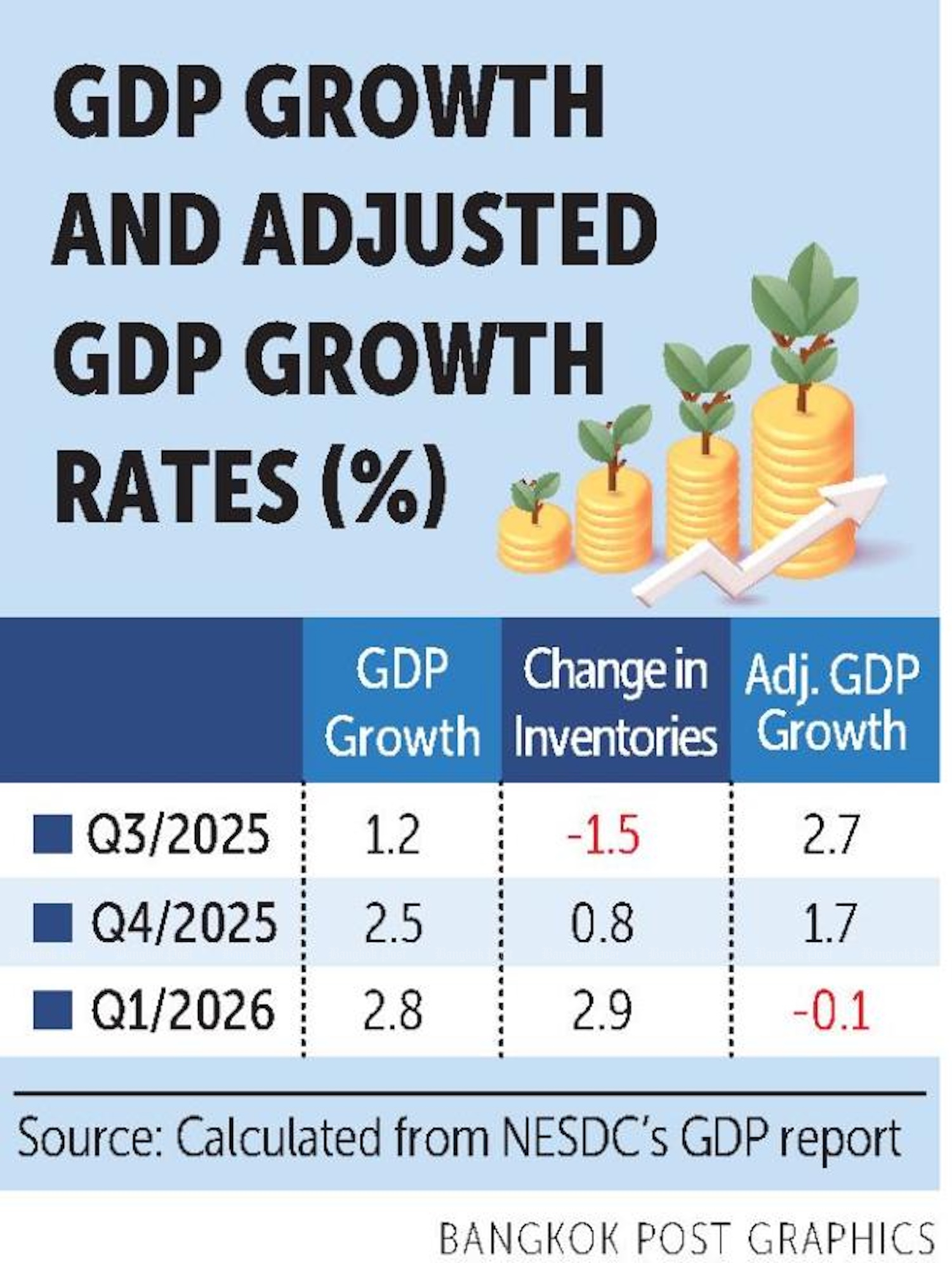

Thailand's quarterly GDP growth rate was 1.2% in the third quarter of 2025, rising to 2.5% in the fourth quarter and further to 2.8% in the first quarter of 2026, according to the National Economic and Social Development Council (NESDC).

Judging from these figures, most people would conclude the economy is on the path to recovery, as higher growth rates are generally associated with stronger economic performance. The government even campaigned under the slogan “Cannot take being richer anymore”. Today, that slogan appears to be little more than a joke.

One may well ask why, despite three consecutive quarters of improving economic growth, the government has had to distribute cash handouts twice to ease economic hardship — first through a 66-billion-baht programme in the fourth quarter of 2025 and then through a 172-billion-baht programme in the second quarter of 2026.

There was, admittedly, the excuse of an oil price shock this year. But what was the justification for last year’s handout? Even with the price shock, inflation remained below 3%, a level that should have been offset by rising incomes associated with GDP growth. On the surface, there appeared to be little need for government support.

A weakening economy? Does that not contradict the NESDC figures cited above? The answer lies in the accompanying table.

I will try to keep the discussion as non-technical as possible. GDP compilation is not widely understood by the public. While there are sound theoretical explanations behind the figures presented in the table, some concepts — such as the calculation of “contributions to growth” — are too complex for a newspaper column.

The GDP growth figures reported by the NESDC, like those published by agencies elsewhere, do not always provide a complete picture of economic conditions. One important component is “changes in inventories”, which economists classify as investment. As inventories accumulate, investment rises, and GDP growth increases. However, such an interpretation may not be appropriate under current circumstances.

The accumulation of inventories, particularly fuel stocks, may not reflect an expanding economy. Instead, it may simply indicate precautionary stockpiling to guard against future shortages or price increases. This may well have occurred in Thailand as tensions between the United States and Iran intensified during the first quarter of 2026 and global oil prices began to rise sharply.

If the temporary effects of stockpiling are removed, GDP growth for the quarter would be revised down to minus 0.1%. That could explain why many Thai households continued to feel economic pressure despite seemingly healthy GDP growth figures. (Story continues below)

The table above contains three columns. The first shows the GDP growth figures reported by the NESDC. The second measures the contribution of inventory accumulation to GDP growth. The third presents adjusted GDP growth after removing the effects of inventory changes. Based on the adjusted figures, it becomes clear the economy has been weakening rather than strengthening.

This conclusion is consistent with the reality experienced by consumers, whose spending power appears to be deteriorating by the day. Most Thai households would likely agree.

However, cash handouts are not an effective solution. They provide only temporary relief and come at a significant fiscal cost.

To date, few have questioned how the government and the Bank of Thailand (BoT) financed last year’s 66-billion-baht cash handout programme and the forthcoming 172-billion-baht Thais Help Thais Plus scheme. The claim that more than one trillion baht in excess liquidity exists within the financial system remains unsubstantiated.

If such excess liquidity were truly available, it would be readily visible in commercial banks’ balance sheets. I have found no evidence of it. Moreover, if such a large pool of idle money existed, bond yields would be driven close to zero.

Thai corporations would also be rushing to refinance their high-cost short-term foreign borrowings using cheap domestic funds. As of the fourth quarter of 2025, such external borrowing stood at US$69 billion, or more than 2.2 trillion baht.

I may know where these mysterious funds originate. They appear to come from the BoT’s printing presses. In the fourth quarter of 2025, the central bank issued 125.6 billion baht in new banknotes and a further 110.2 billion baht between January and April this year.

The theoretical consequence of excessive money creation is inflation and currency depreciation.

Normally, central banks avoid direct money printing because of its inflationary and exchange-rate risks. Instead, they rely on open market operations, purchasing government bonds from commercial banks. The resulting cash injections encourage banks to extend new loans, thereby increasing liquidity in the economy.

However, this mechanism appears ineffective in Thailand at present because commercial banks have entered what could be described as a zombie phase, showing little appetite for new lending. Printing banknotes, while riskier, may therefore have become the only available alternative.

Apart from the increasingly robust GDP figures, both the public and policymakers have also been encouraged by rapid export growth. Export values rose by 17.8% in the first quarter of 2026, making exports the supposed bright spot of the economy.

The key question, however, is whether Thailand is exporting products that it actually produces.

The surge in export growth was not matched by developments in the manufacturing sector, where output expanded by only 1% during the quarter. The figures simply do not add up.

How can a 1% increase in manufacturing output generate a 15.5% rise in export volumes? Even the electronics sector, which recorded export growth of 57.3%, saw production increase by only 8.3%.

The unavoidable conclusion is Thailand has increasingly become a re-export platform for products manufactured elsewhere.

As a result, imports rose by 33.1% in value terms during the first quarter of 2026, pushing the trade balance into a deficit of $303 million, compared with a surplus of $1.42 billion in the previous quarter.

This cannot be blamed on expensive oil imports, as higher fuel prices did not begin to affect Thailand until April, when the monthly trade deficit widened to $6.8 billion. The first-quarter figures were largely driven by re-export activity.

Based on this evidence, I challenge the BoT’s view that the trade deficit is merely temporary and will disappear once global oil prices return to normal.

In my view, the deficit reflects a deeper structural problem that will worsen as Thailand’s manufacturing base continues to erode.

Without recognising the true state of the economy — weakening underlying growth and a fragile export sector — policymakers will never be able to address Thailand’s economic problems effectively.

I am certain of that.