/An%20image%20of%20a%20Tesla%20humanoid%20robot%20in%20front%20of%20the%20company%20logo%20Around%20the%20World%20Photos%20via%20Shutterstock.jpg)

After almost a full year of launching its robotaxi service in Austin in June last year, EV major (and increasingly AI giant) Tesla (TSLA) is set to expand the same to two more cities in Texas: Dallas and Houston. The service will be provided through the Model Y, like in Austin, with no safety monitors in the passenger seat.

Now, for any other company, a development akin to this might have resulted in a sharp share price movement. However, although Tesla's shares did move down by 2%, the wider market concerns were to blame. In fact, the news cycle around Tesla has been uncharacteristically quiet for some time now, with its mercurial CEO, Elon Musk, not grabbing as many headlines nowadays. This seems like a good thing for the shareholders, as any unnecessary attention has hurt shareholders' returns in the past. Moreover, Musk has his task cut out to justify his mammoth $1 trillion pay package, and thus, it would be prudent on his part to cut out any noise.

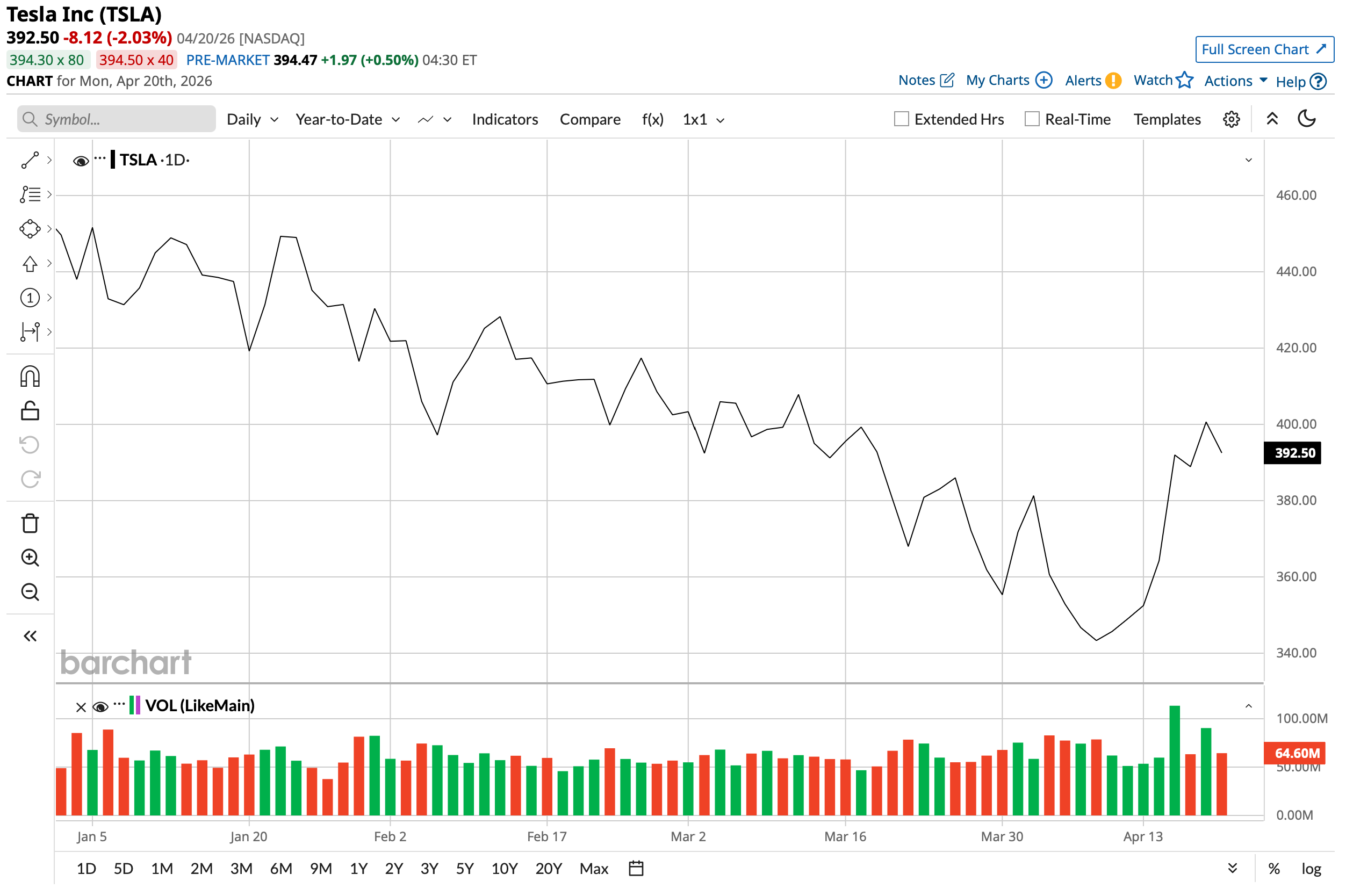

So, with expansion into Dallas and Houston, can TSLA stock arrest its decline for this year (down 13% on a YTD basis) and return to its winning ways? Let's find out.

The Numbers Need To Back the Hype Soon

Tesla once again managed to edge past both revenue and earnings expectations during the quarter, though the underlying results told a more complicated story and left little room for enthusiasm.

For the fourth quarter of 2025, the company brought in total revenues of $24.9 billion, representing a 3% contraction from the year prior. Automotive revenues bore the brunt of the pressure, sliding 11% to $17.7 billion. Meanwhile, EPS settled at $0.50, a 17% drop from the same period a year earlier, though it did manage to clear the Street's consensus estimate of $0.45 by a narrow margin. That result extended Tesla's streak of year-over-year (YoY) earnings per share declines to four consecutive quarters, and when viewed across the last nine quarters, the company has only managed to beat earnings estimates on three separate occasions.

Worryingly, margin performance also weakened, with gross margins tightening to 5.7% from 6.2% in the comparable prior-year period. Further, operating cash flow fell 21% to $3.8 billion. The company ended the quarter with a cash position of $44.1 billion, which remains ahead of short-term debt of $31.7 billion.

Production and delivery numbers retreated, too, following a temporary boost that had stemmed from the expiration of federal electric vehicle tax credits. The company produced 434,358 vehicles during the quarter, a 5% decline on an annual basis, while deliveries tumbled 16% to 418,227 units. The situation deteriorated further heading into the first quarter of 2026, when Tesla reported production of 408,386 vehicles and deliveries of 358,023 units. While those figures came in below the consensus delivery estimate of 365,000 units, they did represent YoY improvements of 12.6% and 6.3% in production and deliveries, respectively.

There were, however, pockets of genuine strength scattered across the business. Active Full Self-Driving (FSD) subscriptions expanded 38% on an annual basis to reach 1.1 million in the fourth quarter. The energy segment continued to build momentum, with revenues climbing 27% to $12.8 billion. The Supercharger network also grew meaningfully, with the station count rising 17% to 8,182 locations while the total number of connectors increased 19% to 77,682.

From a valuation standpoint, TSLA continues to trade at a substantial premium relative to its sector. The stock's forward P/E multiple sits at 197.65, compared to a sector median of just 16.24. Similarly, its forward P/S ratio of 14.69 and P/CF multiple of 92.54 stand in stark contrast to sector medians of 0.94 and 10.13, respectively, reflecting expectations that remain lofty against a backdrop of softening fundamentals.

Paying $1.5 Trillion for an Exciting Future

Most of Tesla's current $1.5 trillion market cap is based on its exciting future projections. In my most recent analysis of the company, I had emphasized what the genuine expectations are around the company. Now, the clamor is building up for it to deliver.

The most immediate value trigger can be the much-anticipated IPO of Musk's space company, SpaceX. Touted to be the first trillion-dollar market cap listing in history, SpaceX literally has sky-high ambitions, with populating Mars being one of them. However, for the here and now, Starlink remains the primary cash cow of SpaceX for now. With revenues of about $4.42 billion made just from launches in 2025 and expectations of the same to reach roughly $20 billion this year, Starlink already has over 10,000 satellites in low Earth orbit (LEO), serving more than 10 million customers globally. Consequently, it has resulted in the company holding a near-monopoly on high-speed satellite internet, with competitors like Amazon’s (AMZN) Project Kuiper still in the early deployment phases.

Moreover, adding another layer to the growth narrative is Terafab, a joint initiative announced by Tesla alongside SpaceX and Intel (INTC). The project reflects Elon Musk's broader ambition to bring as much of the supply chain as possible under direct control. Terafab is designed as a fully vertically integrated semiconductor facility to consolidate logic, memory, and advanced packaging capabilities within a single production environment.

Notably, the facility has set an ambitious production target of between 100 billion and 200 billion custom AI chips on an annual basis. If realized at scale, this would substantially reduce Tesla's reliance on external suppliers such as Nvidia (NVDA) and TSMC (TSM). It could also lay the groundwork for an entirely new revenue stream, should the company choose to make its chip output available to third-party buyers and find itself with the production capacity to do so.

Finally, clarity regarding how far we are in the production and commercial use of Tesla's humanoid robot, Optimus, and what developments in its high-margin energy business are underway will also be watched with keen interest by market participants.

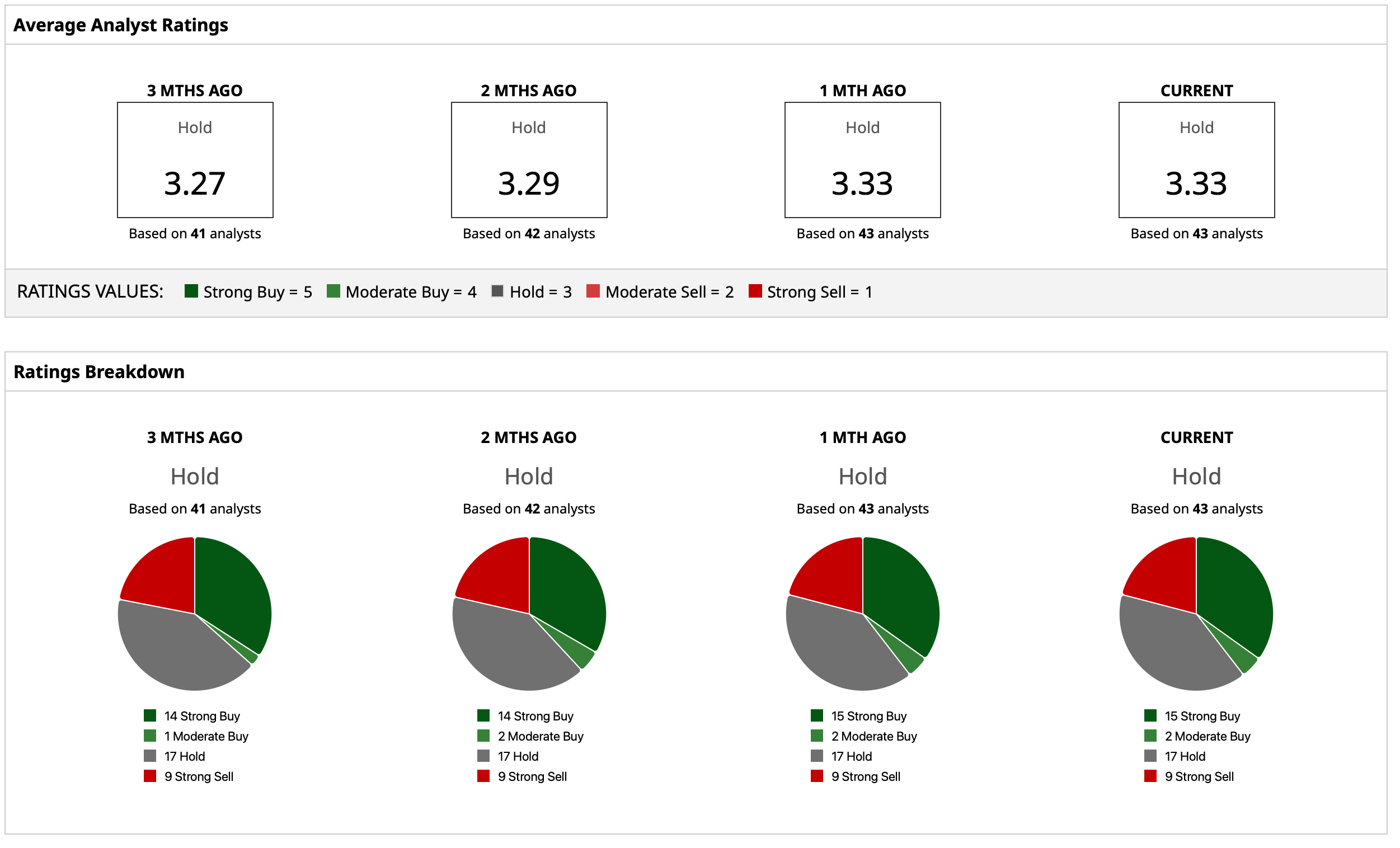

Analyst Opinion on TSLA Stock

Taking all of this into account, analysts have attributed to TSLA stock an overall rating of “Hold,” with a mean target price of $400.58. This denotes an upside potential of about 2% from current levels. Out of 43 analysts covering the stock, 15 have a “Strong Buy” rating, two have a “Moderate Buy” rating, 17 have a “Hold” rating, and nine have a “Strong Sell” rating.