Stocks ended mixed on Monday with the Dow closing at a record high while tech stocks slid into the red.

The Dow Jones Industrial Average gained 65.44 points, or 0.16%, to finish the day at 41,240.52, after setting a new intraday record earlier in the session.

The S&P 500 lost 0.32% to 5,616.84 and the tech-heavy Nasdaq dropped 0.85% to end at 17,725.76.

AI chip titan Nvidia, which is due to report quarterly results on Wednesday, fell 2.25% to $126.46 and the SPDR Technology ETF dropped 1.25%.

Oil prices were rising and Adam Turnquist, chief technical strategist for LPL Financial, cited escalating tensions in the Middle East with Israel launching an air strike on Hezbollah missile launchers stationed in southern Lebanon over the weekend.

"Falling inventory levels in the U.S. have also helped support oil," Turnquist said. "Stockpiles at the key storage hub in Cushing, Oklahoma have recently declined to six-month lows as refining activity ramps up and imports from Canada decline."

"Demand for near-term oil and tight conditions is evident on the oil futures curve, which has remained in backwardation for most of the year," he added, referring to a situation where the spot price is higher than the upcoming futures prices.

Updated 12:54 pm EST by Todd Campbell

Technology stocks aren't the only winners this month

The S&P 500’s gains this year had been driven by technology stock returns, leading many to worry that narrow breadth was a harbinger of a market peak.

Those worries remain, but it wasn’t just technology leading the charge in August.

While the SPDR Technology ETF (XLK) has gained a better-than-market 2.4% (so far), healthcare has done even better, with the Health Care Select Sector SPDR Fund (XLV) rising 3.9% and the SPDR Utilities ETF (XLU) gaining 3.6% month-to-date through August 25.

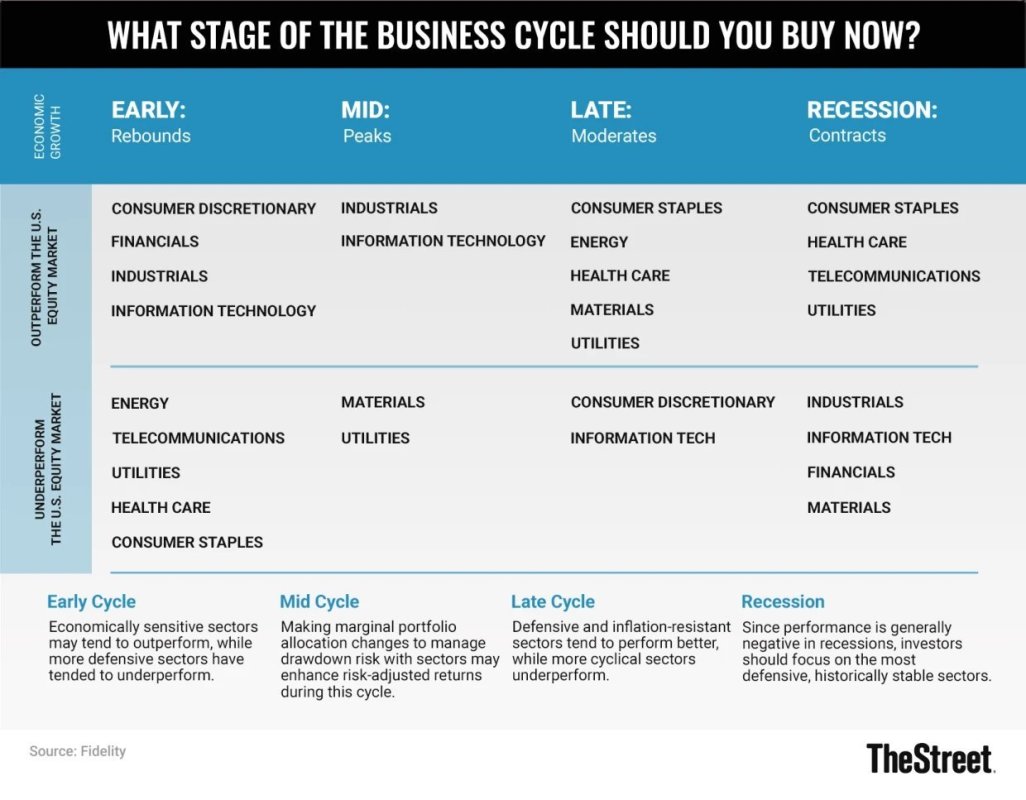

Interestingly (or frighteningly?), healthcare and utilities perform best in the late and recession stages of the business cycle, according to Fidelity.

Perhaps we saw some hedging bets with defensive stocks this month amid all the worry over job growth.

Updated 11:45 am EST by Todd Campbell

Past September S&P 500 returns raise eyebrows

Dog days of summer. Not really. It’s been a pretty busy August.

With a few more days to go, the S&P 500 ETF (SPY) and Nasdaq 100 ETF (QQQ) are up about 2%. Not bad at all considering the Stock Trader’s Almanac pegs the average August return for the S&P 500 at 0.01% (flat) since 1950.

Historically, election year August’s have been better, but even still, we’ve still outpaced the 1.3% average gain notched in past Presidential Election years.

September? Well, that’s been a tougher month for stocks.

The average for all Septembers and Presidential election year Septembers is -0.7% and -0.4%, respectively. The last four Septembers don't add a lot of upside conviction. Although, markets do have a way of surprising the masses.

History says September is the S&P 500's worst month of the year.

— Phil Rosen (@philrosenn) August 26, 2024

Stocks in the last 4 Septembers:

🔴 -3.9%

🔴-4.8%

🔴-9.3%

🔴-4.9%

“Chasing momentum is tempting, but potentially treacherous at this time of year” says @SteveSosnick @ReadOpeningBell 👇https://t.co/mBzGXLN2SF pic.twitter.com/RrENlQBv0K

Regardless, September S&P 500 returns are something to think about over burgers and beverages this coming holiday weekend.

Updated: 10:30 am by Todd Campbell

Stocks mixed as markets digest Middle East tension

The S&P 500 returns to flat after ticking higher in early action. The tech-heavy Nasdaq is down 0.8%.

Investors seem to be digesting a tension-filled weekend in the Middle East. Hezbollah launched over 300 missiles at Israel, despite Israel launching hundreds of airplanes to strike an airfield in a bid to prevent the attack.

Unsurprisingly, oil has made the biggest move higher. Crude oil prices are up 3.4% to $77.35 per barrel, and the United States Oil Fund (USO) , which tracks West Texas Intermediate crude oil prices, is up 3.3%.

Big oil stocks also responded by trading higher. ExxonMobil (XOM) gained 2% while Warren Buffett favorite, Occidental Petroleum (OXY) , gained 1.1%,

Stocks rise premarket on August 26.

Stocks were higher in early Monday trading and pushing record levels, following Friday's surge stemming from the central bank's clear indication that it would cut interest rates.

The Dow Jones Industrial Average gained 123.04 points, or 0.30%, 41,298.12, while the S&P 500 rose 0.24% to 5,648.17 and the tech-heavy Nasdaq Composite advanced 11% to 17,898.11.

Investors cheered the central bank's signaling on interest rates but are wary of the Middle East situation, where Israel and the terrorist group Hezbollah traded attacks over the weekend. Bloomberg reported that oil prices were higher as a result.

Investors will focus this week on the approaching fiscal-second-quarter report from artificial-intelligence-chip maker Nvidia, scheduled for after the market close on Wednesday.

On Friday the S&P 500 finished 1.15% higher, putting it within 1% of its record. Investors reacted to Fed Chairman Jerome Powell's assertion that inflation is on a path toward the central bank's 2% target and that "the time has come" for interest rate policy to adjust accordingly.

Speaking at the Fed's annual convention in Jackson Hole, Wyo., Powell said that the labor market has cooled down considerably and that the balance of its two-sided mandate, full employment and low inflation, has shifted to the jobs side.

Related: Nvidia's Jensen Huang and new inflation data may rock the markets

"Powell’s Jackson Hole speech was largely priced into the bond market, which is why yields stayed in place following his dovish comments," said Richard Saperstein, chief investment officer, Treasury Partners.

"This next regime of lower interest rates provides fuel for equities to move higher. The relationship between stocks and bond yields is important, especially during this Federal Reserve policy transition," he added.

On Friday the Commerce Department's Bureau of Economic Analysis will report the Fed's favorite inflation measure, the Personal Consumption Expenditures Price Index. It measures the changes in prices of the goods and services that consumers buy and use. TheStreet's Charley Blaine reported that as of Sunday at midday the consensus estimate was for a 2.4% rise.

Nvidia (NVDA) is expected to report earnings more than doubled to 64 cents a share from 25 cents in the year-earlier quarter. Revenue is estimated to have doubled as well, to $28.6 billion.

"Nvidia is clearly an important market component and each earnings release will be a cliffhanger," Saperstein said. "The bar remains high for Nvidia to demonstrate that AI spending is continuing at a torrent pace."

Other companies to watch this week include CrowdStrike, (CRWD) which also is reporting for its Q2 on Wednesday. The company is managing the damage last month when it sent out an update that caused computer app outages worldwide.

And other critical companies reporting include department-store retailer Nordstrom (JWN) on Tuesday, customer-relations-management-software giant Salesforce (CRM) on Wednesday, and computer hardware giant Dell Technologies (DELL) and chip stalwart Marvell (MRVL) on Thursday.

"Investors should maintain exposure to large cap technology stocks, which benefit from significant and growing recurring revenues, AI tailwinds as well as a haven from macro volatility," Saperstein said. "The August selloff provided an opportunity to establish or increase exposure."