SpaceX (SPCX) isn’t just chasing Mars anymore. It’s racing up the stock market’s leaderboard in real time. Less than a week after its June 12 IPO, SpaceX jumped about 62%, pushing the company’s value to $2.04 trillion and briefly as high as $2.85 trillion on June 16. That move was enough to surpass Amazon (AMZN) and even edge past Microsoft (MSFT) for a moment, putting SpaceX firmly among the five most valuable public companies.

This shift in value is being driven by more than rockets and Starlink. They are betting that its new neocloud business can turn into a steady, long‑running stream of revenue. Big suppliers like Nvidia (NVDA) and Intel (INTC) see that shift as a lasting driver of demand for their chips and gear rather than a short‑term boost.

Right now, SPCX is still settling after its huge debut, as one clear question hangs over the stock. Can SpaceX’s neocloud push grow quickly enough to support today’s market value and keep lifting the story for Nvidia and Intel, or has SpaceX already baked in too much future success?

SPCX’s Financial Reality

SpaceX designs and runs rockets, spacecraft, and the Starlink satellite internet service from its base in Hawthorne, California. Now, it's adding a Neocloud compute‑leasing business on top of its hardware and network footprint.

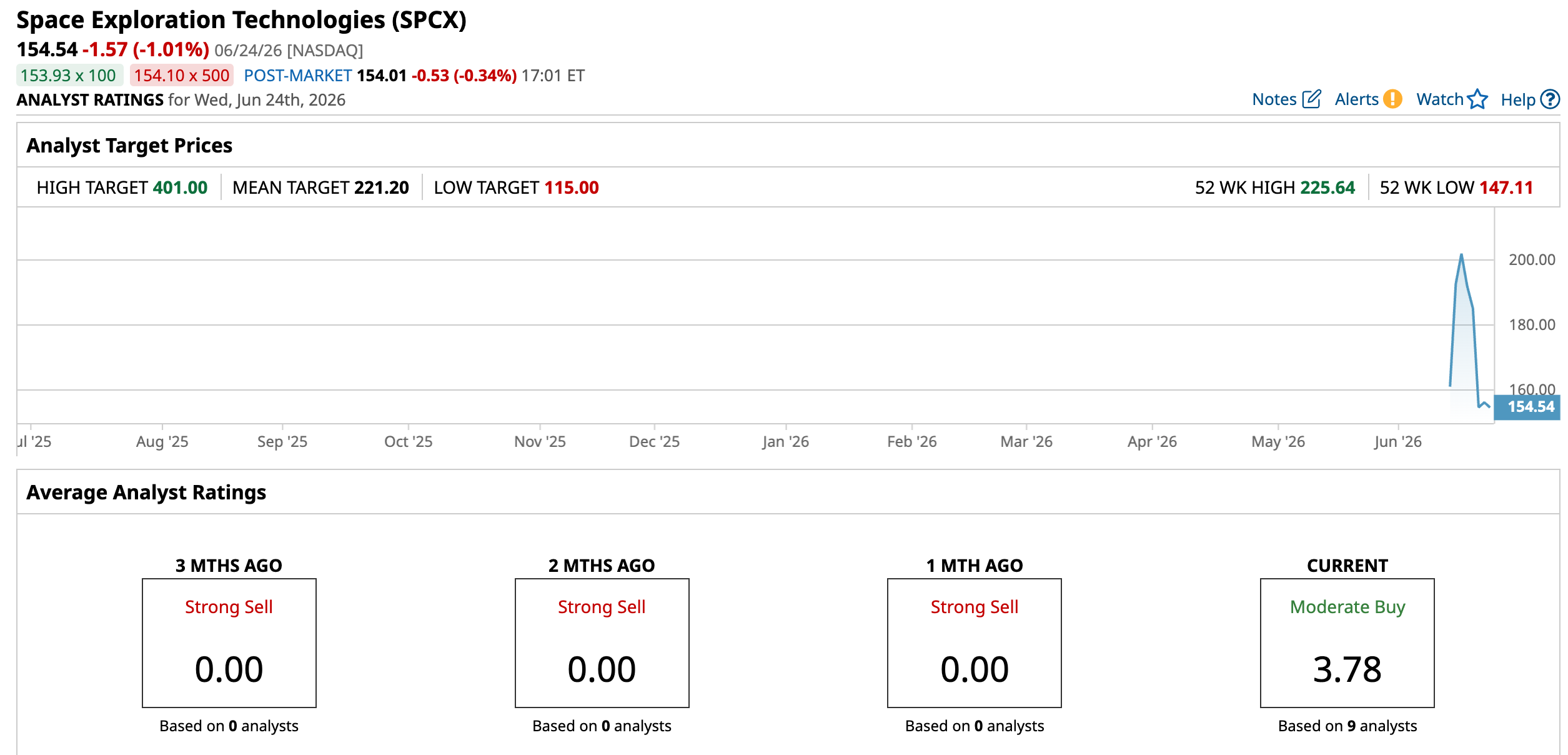

On June 24, SPCX closed at $154.54, down 23.42% over the past five days since listing.

The company sits at a market value of $2.02 trillion, backed by a rich price-to-sales multiple of 55.81 times compared with a sector median of 1.19 times.

Their latest quarter for March 2026 showed sales of $4.694 billion and sales growth of 15.42%, which points to launch, Starlink, and early compute‑leasing deals gaining traction. This same period saw a net loss of $4.276 billion, with net income growth of -709.85%, highlighting that heavy spending continues to weigh on the bottom line.

It was a balance sheet showing total assets of $102.094 billion, up 10.88%, and total liabilities of $67.561 billion, down 24.52%. That hints at big investments in rockets, satellites, and compute clusters funded with a cleaner mix of obligations.

This quarter’s operating cash flow came in at $1.047B, down 84.57%, while net cash flow was -$8.516 billion, a drop of 162.51%, telling investors SPCX remains firmly in a cash‑hungry build‑out phase.

SpaceX’s Neocloud Story

SpaceX recently agreed to buy AI coding startup Cursor, the parent company Anysphere, in an all‑stock deal valued at $60 billion. This move is aimed at beefing up its coding and automation tools and narrowing the gap with rivals like Anthropic and OpenAI in self‑writing software. The deal is expected to close in the third quarter of 2026 and shows a clear push into AI software that sits neatly beside its growing neocloud compute business.

Space Exploration Technologies is also stepping up its funding game. The company has launched its first investment‑grade bond sale soon after its record IPO, targeting at least $20 billion in senior unsecured notes, and early indications point to strong demand from credit investors. Proceeds are set to refinance bridge loans tied to the IPO and cover broad corporate needs, including more spending on rockets, satellites, and AI‑ready infrastructure.

Taken together, the Cursor deal and the new bond issue show SpaceX funding both sides of its story at once, software and infrastructure.

What the Analysts Are Really Saying

Next up for SpaceX is a quarter that will show the amounts investors are willing to pay for the neocloud story. For the June 2026 period, the average earnings estimate is -$0.18 per share, with year‑over‑year (YOY) earnings expected at -100.02%. That is a sharp drop and reflects spending that still runs ahead of profits.

On June 22, ARK Invest’s funds bought another 210,121 SPCX shares, based on daily trading disclosures. The biggest purchase came from the ARK Innovation ETF (ARKK), which added 131,837 shares. This followed earlier buying after the June 12 IPO, when the firm accumulated about 3.29 million SPCX shares across its ETFs.

On the research side, Arete Research started coverage on SpaceX on June 18 with a “Buy” rating and a $401 price target, the highest target since the stock listed. Their analyst Andrew Beale linked much of that view to Starlink V3 satellites, expected to fly on Starship and boost data capacity.

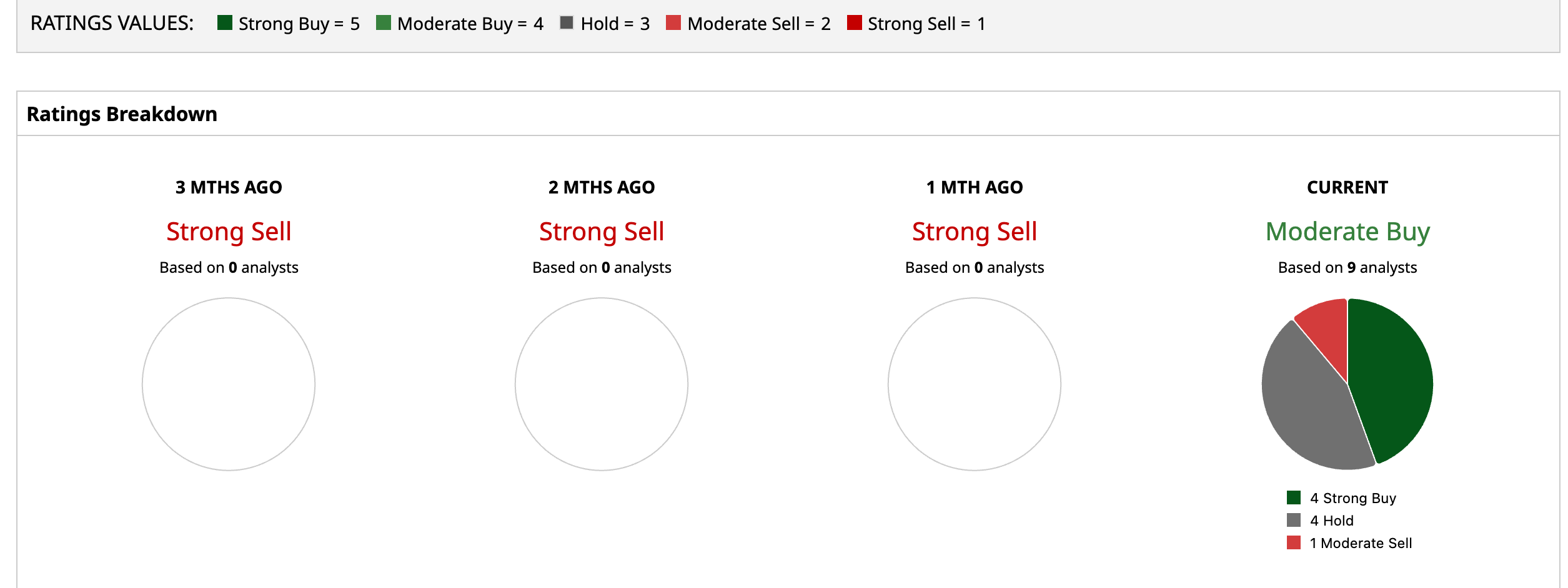

SPCX’s broader analyst consensus tells the same story in numbers. Across nine tracked analysts, the stock carries a “Moderate Buy” consensus rating. The average price target is $221.20, which implies a 43.14% upside from the June 24 closing price.

Conclusion

SpaceX’s move into neocloud operations has made SPCX a straightforward way to bet on the future of computing power and satellite internet. Big contracts, heavy spending on infrastructure, and upbeat analyst targets are all pointing in the same direction. Together, those factors suggest the shares are more likely to drift higher over the long run, even if the path includes some sharp swings.