/Space/Planet%20earth%20with%20flying%20rocket%20by%20Sergey%20Mironov%20via%20Shutterstock.jpg)

Space Exploration Technologies (SPCX), better known as SpaceX, is a vertically integrated aerospace, satellite connectivity, and artificial intelligence heavyweight. Founded by Elon Musk in 2002, the company operates across three main units – Starlink (connectivity), xAI (artificial intelligence), and Space. The company has redefined the economics related to space exploration using reusable rockets, minimizing launch costs by up to 90% versus competitors.

Its connectivity program, Starlink, now handles approximately 9,600 low-earth orbiting satellites in over 164 countries, delivering high-speed internet, low-latency internet connectivity. Meanwhile the xAI platform, now integrated into SpaceX, spans its frontier, Grok LLM, the X platform (formerly known as Twitter), and orbital AI compute satellites slated for deployment in 2028.

SpaceX Spikes Post IPO

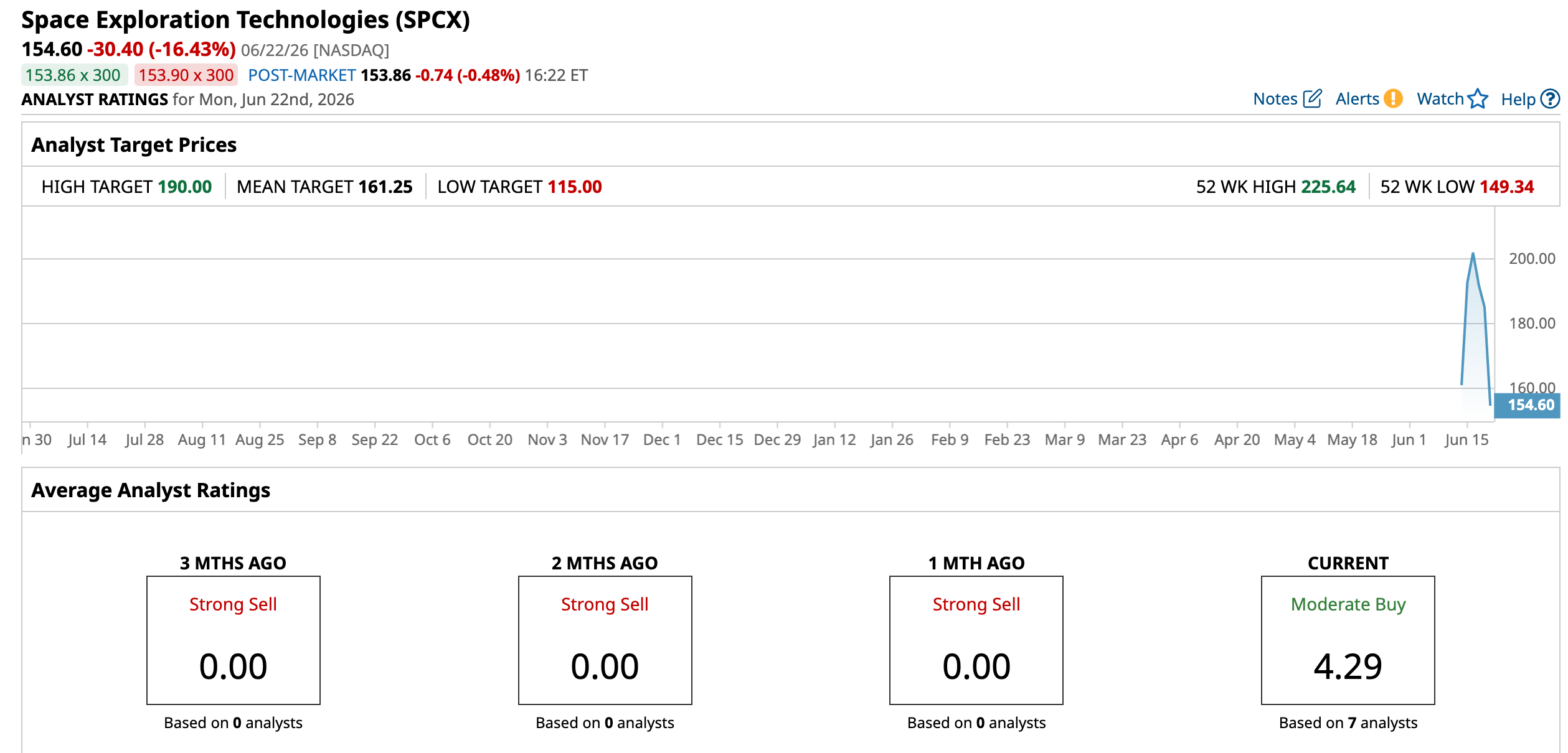

SpaceX completed its IPO on 12 June, raising approximately $87 billion at $135 per share, making it the largest IPO in history. The company shares hit an all-time high of $225.64 on June 16, before pulling back to the $185 level, still representing a 37% rise in just 10 days.

Against the Nasdaq Composite’s ($NASX) 12.54% year-to-date (YTD) gain, SPCX’s explosive start has already captured the imagination of both institutional and retail investors globally. The stock has become the most sought-after retail stock, outperforming Nvidia (NVDA) by 3.5 times in retail volume.

SpaceX Financial Metrics

SpaceX posted its first-quarter results with a revenue of $4.69 billion, while reporting an operating loss of $1.94 billion and adjusted EBITDA at $1.13 billion, reflecting its heavy investment in xAI infrastructure and Starship development. Starlink generated $3.26 billion in revenue in Q1, constituting 69% of total revenue, making it an indispensable financial engine for the company.

Connectivity stood out as the only profitable sector for SpaceX, recording $1.19 billion in operating profit, while the space business posted a loss of $619 million, with the AI unit posting $2.5 billion in operating loss, citing heightened R&D investment costs. AI segment and R&D costs spiked over 300% to $5.06 billion for full-year 2025, driven by $1.67 billion in higher GPU depreciation and $1.44 billion in infrastructure and cloud expenses.

Management has defined an ambitious roadmap for SpaceX: completing a 12,000-satellite Starlink constellation, achieving operational Starship capability for lunar and Mars missions, and beginning deployment of orbital AI compute satellites by 2028. The company carries $25.45 billion in contractual commitments, with 95% due in 2026 and 2027.

Oppenheimer Raises SpaceX Target

Oppenheimer analyst Timothy Horan has raised his price target on SpaceX to $250 from its initial $190 target, hinting at a potential 35% upside from the market rate. The analyst cited the company’s acquisition of Cursor and its uniquely advantaged position on the AI stack as the key reason behind the hike.

Horan described SpaceX as owning "every layer of the AI stack," giving it structural cost and quality advantages that no competitor can replicate. The upgrade was driven by a sharp revision to AI revenue estimates, with Q4 2026 AI revenue now forecast at $8.75 billion, up from $4.75 billion previously, reflecting Cursor's explosive growth trajectory, which Horan estimates is currently running at a $4 billion annual revenue rate and targeting $6 billion by year-end 2026.

With Starship described as both a launch moat and a NASA-funded lunar supply base, and orbital compute identified as a longer-term revenue catalyst, Oppenheimer views SpaceX's commercial roadmap as one of the most compelling in technology today.

Should You Buy SPCX?

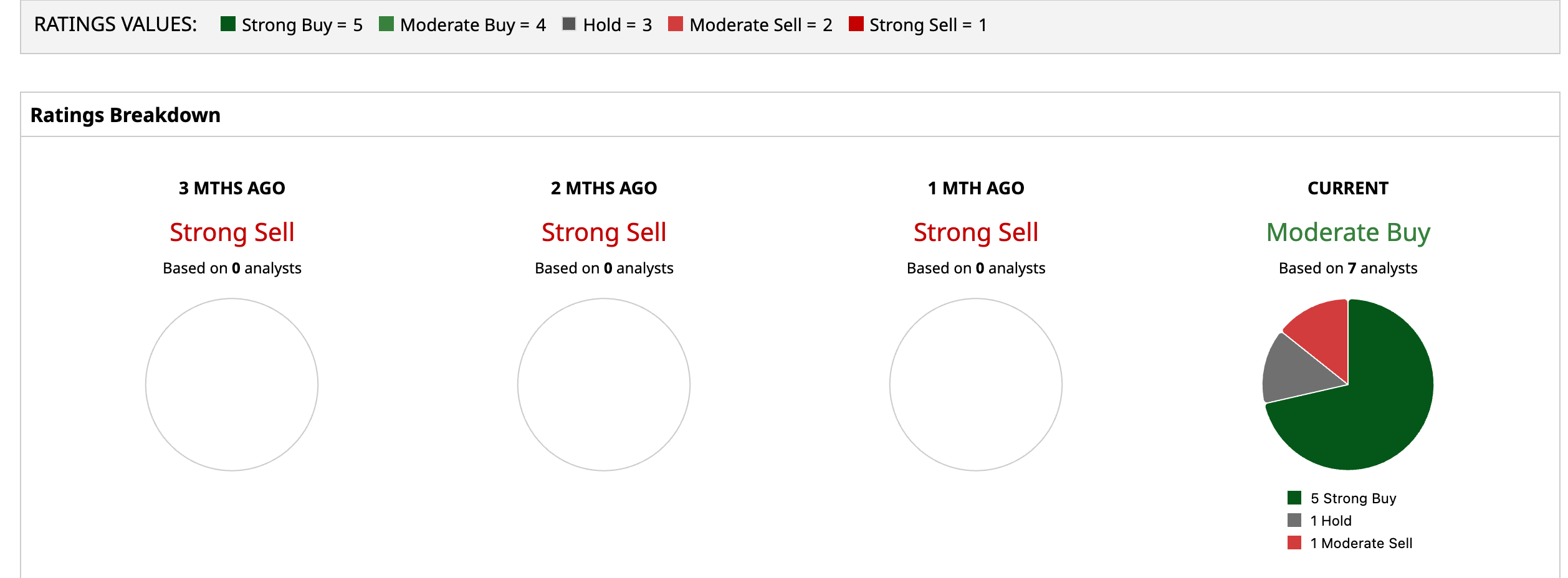

With Oppenheimer's $250 price target underscoring SpaceX's unrivaled position across the entire AI stack, from orbital compute to Cursor's $4 billion revenue run rate, the long-term bull case is as compelling as any stock in the market today. However, Wall Street's nascent consensus reflects a stock that has already raced ahead of near-term fair value. SPCX carries a "Moderate Buy" rating across seven analyst ratings, comprising five"Strong Buy," one analyst giving a "Hold," and one bearish with a "Moderate Sell." With a mean price target of $161.25, the market implies a 4.3% upside from current levels.

For investors, SPCX is the ultimate long-term conviction buy, but disciplined entry points matter enormously at a $2.4 trillion valuation.