Smith & Wesson Brands (SWBI) reported its fiscal third-quarter results on Friday, easily topping Wall Street expectations and igniting a powerful rally in its shares. The stock surged 18% in a single session, propelling it to a fresh 52-week high as investors cheered signs of renewed strength in the firearms giant’s core handgun business. Even as broader industry demand softened, SWBI’s handgun sales surged, suggesting the company is steadily stealing market share from smaller rivals.

For a stock that has languished in recent years amid declining background checks and shifting consumer sentiment, the breakout performance raises an intriguing question: Is it finally time to buy America’s largest publicly traded firearms manufacturer?

Earnings Surpass Expectations

The numbers told a clear story of outperformance. SWBI posted net sales of $135.7 million, a 17.1% jump from the prior-year quarter and well ahead of consensus estimates around $125 million to $128 million. Adjusted earnings per share came in at $0.08, beating forecasts of $0.04 to $0.05 and more than doubling last year’s $0.03 result. Gross margin expanded to 26.2% from 24.1%, helped by higher average selling prices, better fixed-cost absorption, and a favorable product mix tilted toward higher-margin handguns. Adjusted EBITDA rose nearly 21% to $16.8 million.

Management followed the strong print with upbeat guidance, projecting 10% to 12% sales growth for Q4 compared with the same period a year ago. The tone was confident: after a year of disciplined inventory management, the company now sees enough sustained demand to ramp up production. Distributor inventories remained flat at targeted levels, allowing SWBI to capture incremental share without flooding the channel.

Inventory Discipline Gives Way to Production Ramp

For the past 12 months, SWBI deliberately throttled output and worked down excess stock built during the pandemic-era boom. That restraint paid off in healthier margins and stronger cash flow—the company turned free cash-flow positive and reduced debt. Now executives are flipping the switch, signaling plans to increase manufacturing to meet resurgent orders. The shift underscores improving visibility and a belief that current order strength is more than a temporary blip.

Yet the macro backdrop is less rosy. According to the FBI National Instant Criminal Background Check System (NICS) data—the best proxy for consumer gun purchases—fell 2% in the quarter and has declined every month for the past year. NICS checks have now dropped for four consecutive years, reflecting a broad cooling in firearm purchases after the surge that began in 2020.

Still, long-term ownership trends remain robust. According to the Pew Research Center, 42% of U.S. households own at least one firearm, with personal protection cited as the primary reason for purchase. That enduring cultural attachment provides a floor beneath industry volumes even when short-term demand ebbs.

Another supportive factor emerged in 2025: violent crime plummeted as law-enforcement priorities shifted. Murders fell 19%, robberies dropped 20%, and aggravated assaults declined nearly 10%. Fewer high-profile incidents reduce the fear-driven spikes that often lift sales.

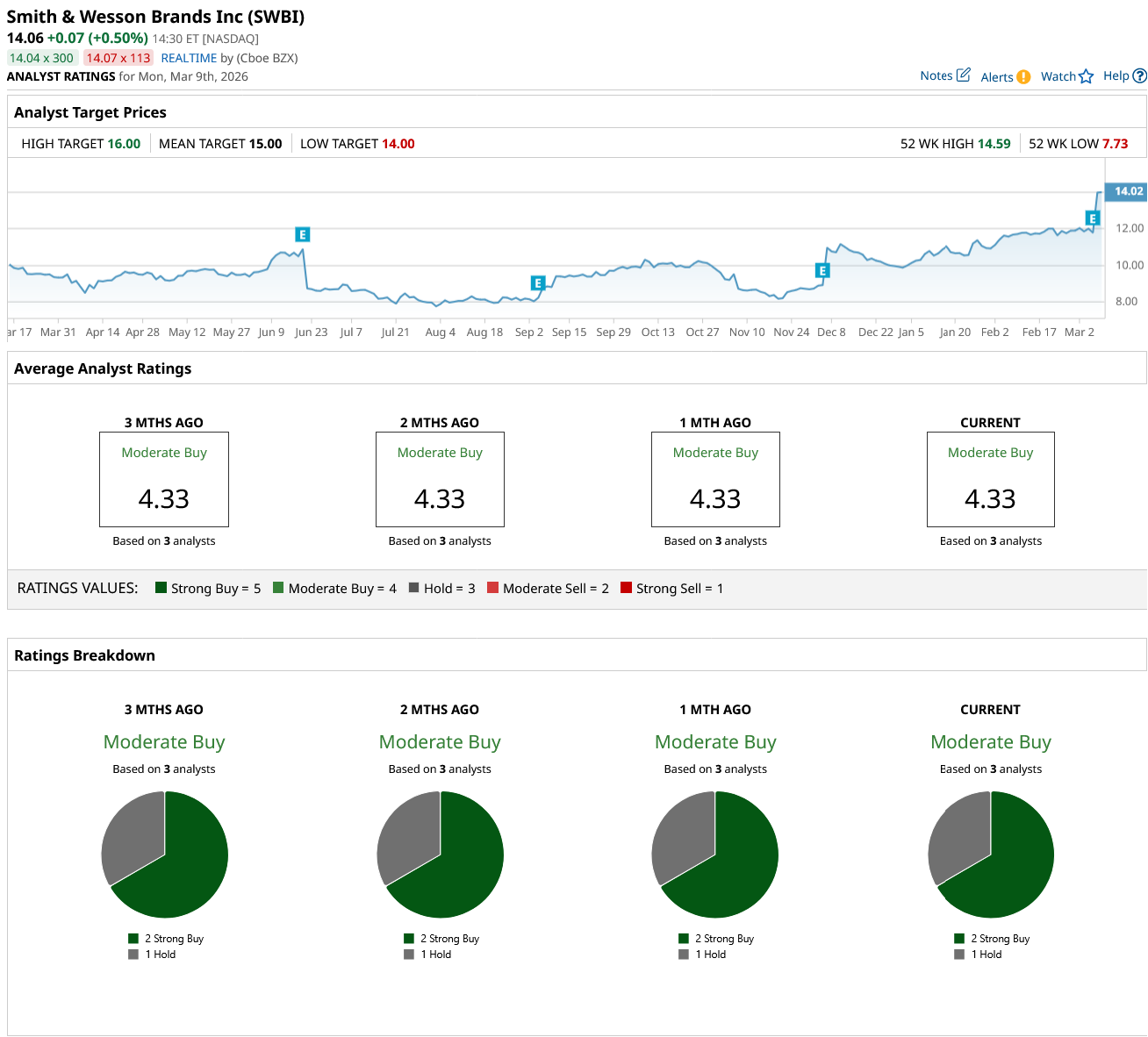

What Wall Street Thinks About SWBI Stock

Wall Street attention is surprisingly thin for a company of SWBI’s size. Barchart data shows just three analysts covering the stock, all maintaining a “Moderate Buy” consensus, with a mean price target of $15, implying 7% upside potential.

Valuation tells a more cautious tale. At current levels the shares trade at a trailing P/E multiple of 58.95—well above its historical averages and industry peers. While the dividend yield of 3.7% offers income appeal, the stock’s premium pricing leaves little margin of safety if demand weakens further.

Bottom Line

SWBI’s financials are solid, its balance sheet is strengthening, and its dominant position in the handgun market makes it a high-quality operator in a notoriously tough industry. Yet this remains a deeply cyclical business whose fortunes swing with crime rates, politics, and consumer sentiment. With the stock performing at or near its peak and valuations stretched, existing shareholders can comfortably hold. Prospective buyers, however, would be better off waiting for a pullback before pulling the trigger.