/NVIDIA%20Corp%20logo%20outside%20building-by%20BING-JHEN_HONG%20via%20iStock.jpg)

Timothy Arcuri, an analyst at UBS, has called trading conditions for Nvidia (NVDA) stock “favorable” for investors as the company heads into its fiscal Q4 earnings report on Feb. 25. The analyst believes numerous factors are looking positive for the stock, including supply chain issues and a not-so-impressive stock performance.

Arcuri expects $76 billion in revenue from the chipmaker in the recently concluded quarter. While analysts have questioned the company’s expected 75% gross margins, Arcuri suggests there is nothing to worry about on that front. To find out whether Nvidia is a “Buy” before the earnings come out, let’s look at the company’s current valuation and earnings expectations.

About Nvidia Stock

Nvidia is currently the most important company in the world when it comes to building artificial intelligence (AI) infrastructure. Its graphics processing units (GPUs) are a must-have for anyone training large language models (LLMs) or building data centers, both of which are vital in AI development. The company is led by Jensen Huang and headquartered in Santa Clara, California.

Anyone who’s bought NVDA stock over the last two years is sitting on pretty gains. However, this year so far has been nearly flat, with the stock returning 2% so far. This happened despite upward analyst revisions and a positive general sentiment for the stock. The iShares Semiconductor ETF (SOXX) has returned 20% so far this year, showcasing how semiconductors continue to be a great bet for outperformance.

This lack of performance provides the very opportunity that UBS analysts are pointing out. Nvidia’s forward price-to-earnings (P/E) ratio of 27.03x is by no means outrageous, and a PEG ratio of 0.58x suggests the stock is still undervalued considering future growth potential. The current Wall Street consensus calls for an earnings growth of 64.52% in the next year, something easily achievable considering the company’s central role in AI infrastructure.

Nvidia also looks undervalued on various other metrics. Its forward EV/EBITDA of 33.48x is much cheaper than the five-year average of 38.35x. It is similarly trading at a 6.7% discount on a forward price per cash flow basis. It is incredible that a stock that has returned 44% over the last 12 months is still trading at a discount to its historical valuation.

An Earnings Report To Look Forward To

One aspect that makes Nvidia’s upcoming earnings on Feb. 25 so interesting is the fact that when the company announced its Q3 earnings on Nov. 19, it was trading at exactly the same level. Despite posting a beat and guiding higher, the stock has not moved up, making it an interesting bet for the upcoming earnings report.

On the earnings call for Q3, management guided for a Q4 revenue of $65 billion, which Arcuri now expects to be $76 billion. This is another example of how the stock has not appreciated despite improving fundamentals. The management also acknowledged that input costs were rising. However, it reiterated that it could still manage to hold gross margins in the mid-70s. The company is likely to exclude all China revenue from guidance, which could become a tailwind if relations with China improve going forward.

What Are Analysts Saying About NVDA Stock?

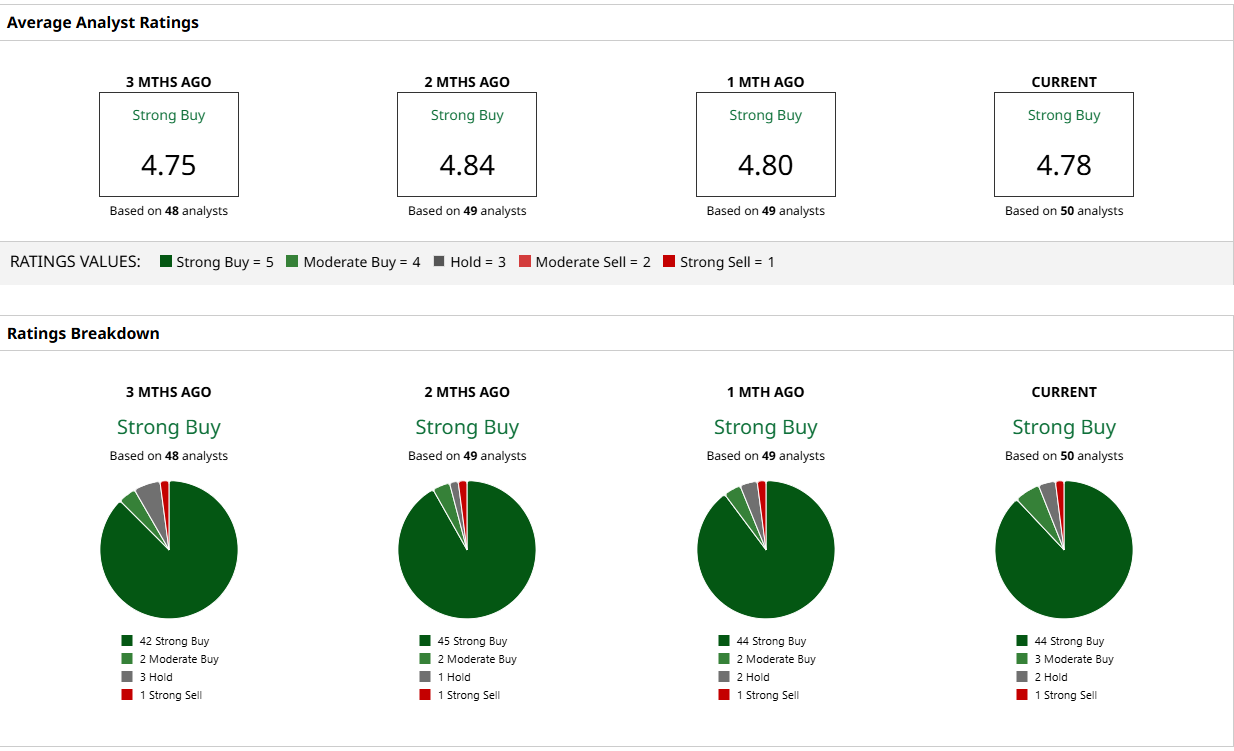

UBS raised NVDA stock’s price target from $235 to $245. As we get nearer to the earnings date, more analysts are likely to come forward with a higher price target. Currently, the mean price target is $255.34, according to analyst ratings from 50 analysts. This suggests a further 36% upside from here on, a decent return for a company that is perhaps the safest bet as AI continues to change how we work and live our lives.