/AI%20(artificial%20intelligence)/Ai%20chip%20by%20Quality%20Stock%20Arts%20via%20Shutterstock.jpg)

The artificial intelligence (AI) boom has created clear winners across the semiconductor industry, but not all of them build GPUs. Some supply the technologies that make AI infrastructure usable at scale, and few markets have tightened faster than memory and storage. As hyperscale cloud providers race to deploy larger AI clusters, demand for high-performance flash storage has outpaced supply, pushing pricing higher across the industry.

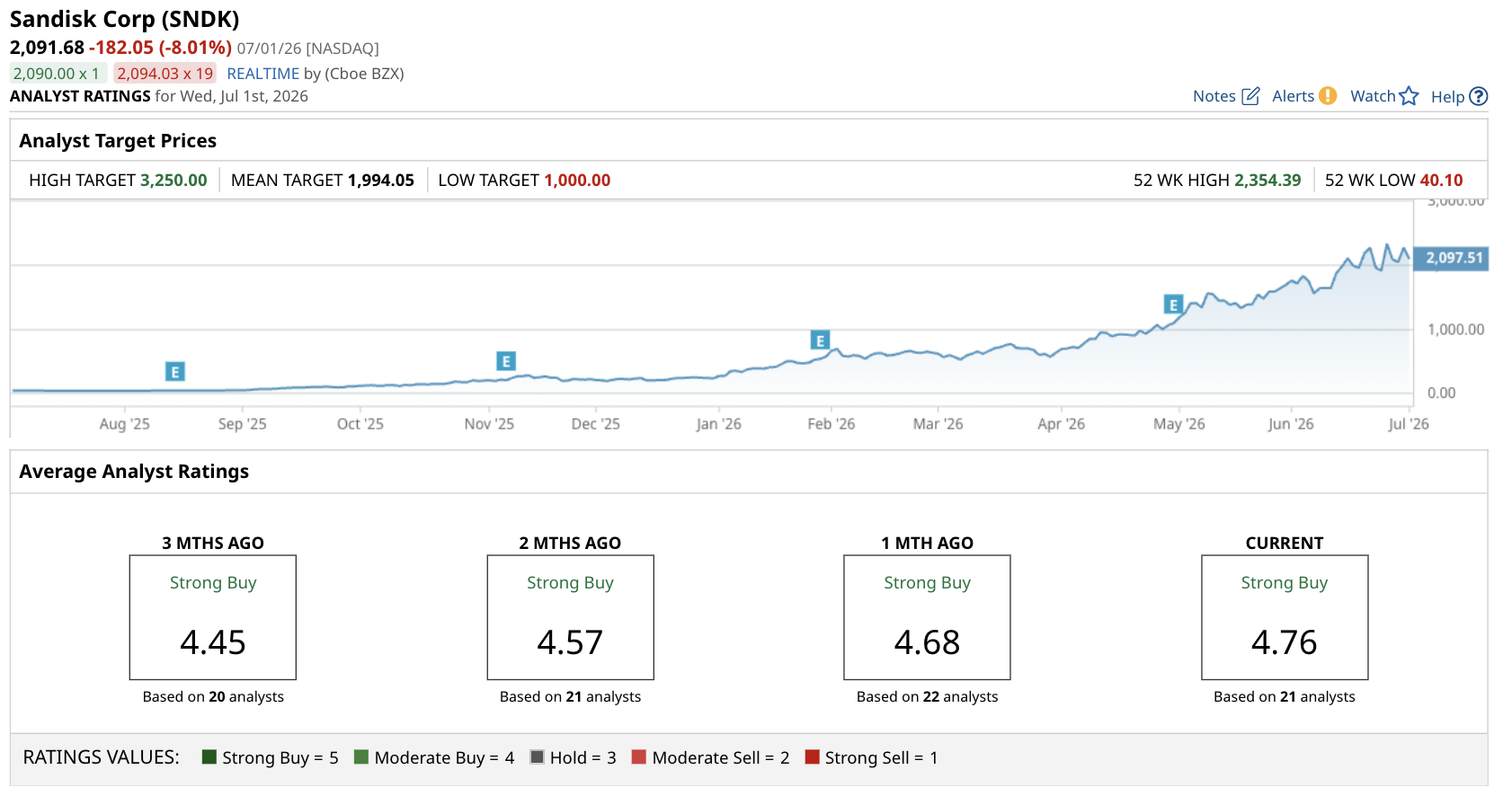

That backdrop has helped one stock separate itself from the rest of the market. Through the first half of 2026, Sandisk (SNDK) ranked as the S&P 500's ($SPX) best-performing stock. SNDK stock is up more than 645% year-to-date (YTD), extending a rally that has surprised even longtime semiconductor investors.

AI Demand Is Rewriting the Storage Market

GPUs may capture most of the headlines, but every AI server also requires massive amounts of high-speed storage. Training models and serving AI applications generates enormous volumes of data, making NAND flash memory an increasingly valuable part of the infrastructure stack.

Sandisk is benefiting from two powerful tailwinds at the same time:

| Company | Primary Business | AI Exposure | Recent Trend |

| Sandisk | NAND flash storage | Enterprise SSDs, AI servers | NAND pricing rising |

| Micron (MU) | DRAM and NAND | HBM and NAND | HBM demand outpacing supply |

| Samsung Electronics | Memory and storage | HBM, DRAM, NAND | Expanding AI capacity |

| SK Hynix | Memory | HBM leader | AI memory shortages continue |

Unlike DRAM, which has been dominated by demand for high-bandwidth memory (HBM), NAND flash has quietly entered one of its strongest pricing environments in years. Industry data continues to point toward constrained supply and improving contract pricing throughout 2026. Analysts see the shortage lasting into 2028.

Supply Discipline Has Changed the Story

Previous NAND upcycles often collapsed because manufacturers flooded the market with new capacity. This cycle looks different.

The industry reduced wafer production after memory prices fell below profitable levels. As AI demand accelerated, though, supply found itself in a far healthier position.

That shift has translated directly into stronger financial performance. Gross margins have expanded as average selling prices have recovered, while enterprise SSD shipments have become a larger share of revenue than lower-margin consumer products.

Granted, memory has been one of the semiconductor industry's most cyclical businesses. Higher prices eventually encourage additional production. The question is whether supply can catch demand while Amazon (AMZN), Microsoft (MSFT), Alphabet (GOOGL), and Meta Platforms (META) continue spending hundreds of billions of dollars building AI infrastructure.

For now, the numbers suggest demand still holds the upper hand.

Valuation Is Rich, But Momentum Has Support

One reason Sandisk has led the S&P 500 since its spinoff from Western Digital (WDC) last year is that expectations were exceptionally low. Investors were pricing in another prolonged downturn just as the market began tightening.

That said, today's valuation showing a price-to-earnings (P/E) ratio of 75.8 times and a forward P/E of 35.5 times assumes current pricing remains favorable well into 2027. Any slowdown in enterprise spending or faster-than-expected capacity additions could pressure both margins and earnings.

Surprisingly, Sandisk's outlook depends less on consumer electronics than in previous cycles. AI data centers have become an increasingly important source of demand, helping smooth what has historically been a volatile business.

Regardless, investors should remember that memory companies rarely move in straight lines. They often overshoot both on the way down and on the way up.

Key Takeaway

In short, Sandisk's position as the S&P 500's best-performing stock during the first half of 2026 is backed by improving industry fundamentals, not simply market enthusiasm. Rising NAND pricing, disciplined supply, and AI-driven enterprise demand have combined to create one of the strongest storage markets in years.

Ultimately, the easy gains may already be behind new investors after such a powerful rally. Even so, if AI infrastructure spending remains on its current trajectory and NAND supply stays constrained, Sandisk could continue outperforming many semiconductor peers. Smart investors should watch memory pricing, enterprise SSD demand, and management's commentary in upcoming earnings reports. Those three indicators will likely determine whether the market leader can remain on top through the second half of 2026.