It’s now day 30 of the Red Sea crisis—and month four of worries of a wider Middle East conflict, the possibility of which has concerned economists and politicians alike since the Oct. 7 outbreak of the Israel-Hamas war. Over the past month, Houthi militants based in Yemen have repeatedly attacked cargo ships in the area, forcing shipping giants to reroute their vessels around South Africa’s Cape of Good Hope. That’s a big deal, because roughly 15% of the world's shipping traffic, and 30% of its container traffic, transits the Red Sea each year, including oil tankers and container ships transporting every type of product you can imagine.

The conflict has intensified in recent days. On Thursday, a U.S.-led coalition ordered airstrikes on Houthi targets in Yemen, a week after Iran, which has backed Houthi militants for years, deployed the warship Alborz to the region. Even oil tankers, which for a time had continued their transit through the Red Sea even as cargo vessels headed for safer passages, abandoned the trade route this week. On Friday, four major oil tankers changed their course to avoid the Red Sea after the most recent strikes by the U.S. and its allies.

Ominously, for the global economy, which was rattled by Russia’s 2022 invasion of Ukraine, geopolitics could be returning to center stage before the Federal Reserve’s inflation battle has been completely won.

Economic consequences of the Israel-Hamas war are already being felt, bringing back memories of the supply chain chaos and surging oil prices that exacerbated inflation after the Ukraine war. Oil prices are rising; shipping costs have more than doubled since October; and there are increasingly lengthy transit delays for goods. Some experts are concerned that this bottleneck will fuel another surge of global inflation, forcing the Fed to hold off on its widely expected interest rate cuts.

But when it comes to forecasting the economic impact of the Red Sea crisis, particularly for the U.S., Bob Elliott, co-founder and chief investment officer of the investment firm Unlimited, advocates humility.

He noted that while it’s helpful to understand and prepare for the potential consequences of the Red Sea crisis—which include rising inflation and slowing global growth—no one really knows how long it will last or how bad it will get. When it comes to the conflict’s impacts on the U.S.: “The most honest answer you should be getting is ‘I have no idea,’” Elliott told Fortune. That may not be the most satisfying answer, but it’s the “right answer,” according to the former Bridegewater exec.

Experts agree that in theory, the Red Sea crisis could certainly cause shipping costs and oil prices to soar, leading to a resurgence in global inflation that would force the Federal Reserve to keep interest rates higher for longer, weighing on the U.S. economy. But tensions in the key trade route could also cool, leading oil prices and inflation to drop and paving the way for a soft landing—where inflation fades without a recession.

Betting on rising tensions or an expanded war in the Middle East wouldn’t be much of a stretch given the region's history. But the “default assumption” shouldn’t be that the Red Sea crisis will spread and impact the global economy just yet, Elliott argued.

A shipping and supply chain crisis

Forecasting the economic impact of the Red Sea crisis isn’t easy. But the regional conflict is already leading to some identifiable problems for businesses and consumers.

First, freight rates are rising—fast—and that will have an immediate impact on some American companies. Drewery’s World Container Index, which tracks container freight rates on 11 major trade routes, has soared 121% from $1,390 per 40 foot container just before the outbreak of the Israel-Hamas war to $3,090 this week.

Second, supply chains are being rerouted, which is leading to longer transit times for goods worldwide. Retailers have begun to warn their customers of potential issues. The Swedish furniture giant Ikea told the BBC in late December that consumers should expect “delays” and “some availability constraints” at their stores due to the Red Sea crisis. And Tesla was forced to halt production at its Berlin plant because “considerably longer transportation times” are “creating a gap in supply chains,” Reuters reported Friday.

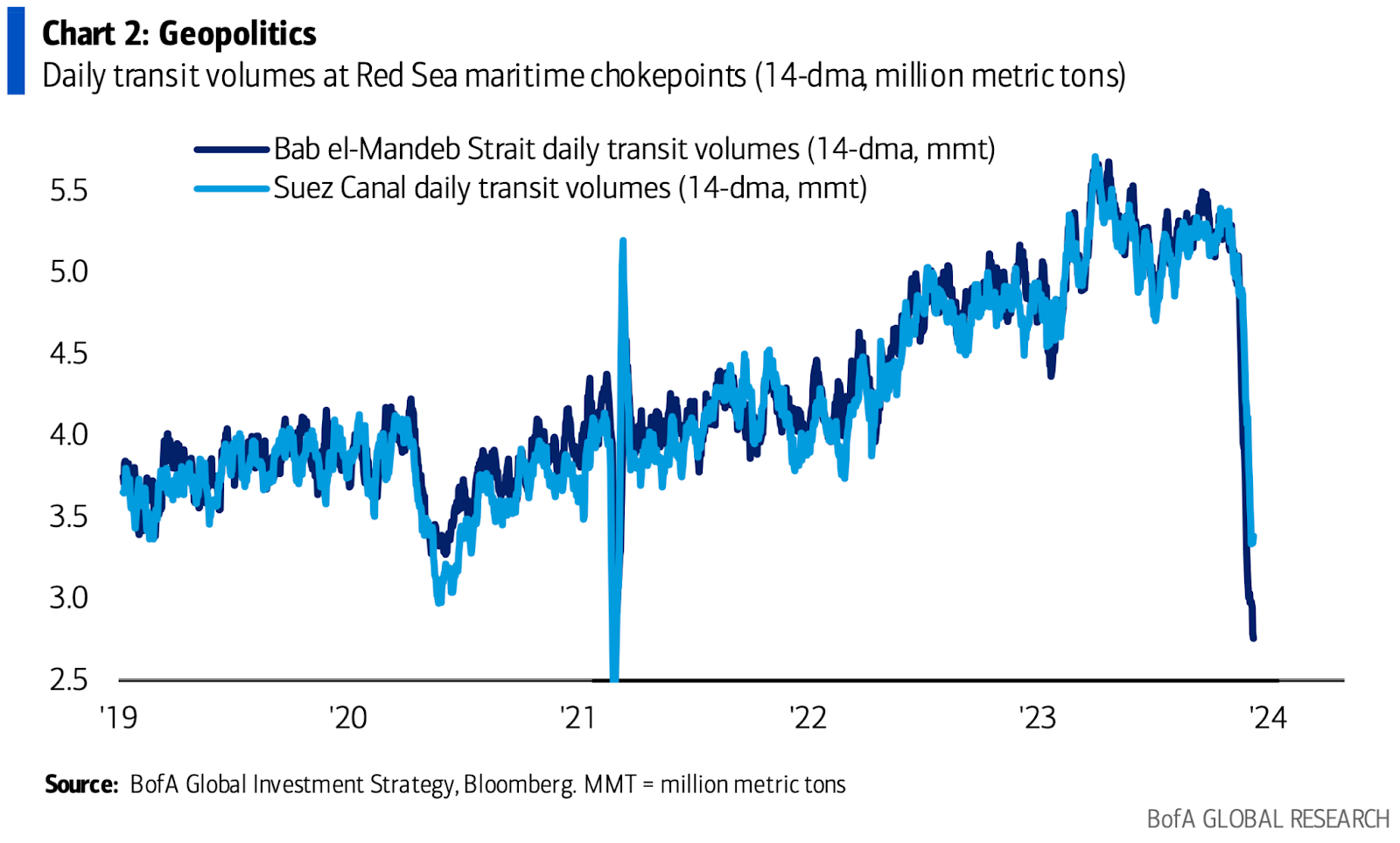

Bank of America analysts put out a chart on Thursday detailing some of the impact on transit volumes for key trade routes around the Red Sea, and it shows just how dramatic the supply chain chaos is. The daily goods transit volume in the critical Suez Canal, for example, has been cut in half since December.

Thomas Goldsby, a supply chain management professor and the Haslam Chair in Logistics at The University of Tennessee, explained that if this situation isn’t resolved by Lunar New Year (Feb. 10), a period when shipping traffic rises sharply, U.S. businesses will face serious cost increases amid crippled supply chains.

“By then I'm getting very concerned, particularly if it becomes escalation, rather than de-escalation,” he told Fortune. “Because then we're going to start talking about altering supply chain configurations, maybe looking to source in different locations, not just seeking the short-term fixes.”

That’s bad news considering Maersk’s CEO prediction that the shipping crisis isn’t likely to end soon. “It’s unclear to us if we are talking about re-establishing safe passage into the Red Sea in a matter of days, weeks or months,” Vincent Clerc told the Financial Times Thursday, adding that the shipping crisis “could potentially have quite significant consequences on global growth.”

Still, Goldsby said that, for now, the shipping and supply chain issues caused by the Red Sea crisis are far milder than those seen during the pandemic. “The pandemic was so ubiquitous, right? It hit the entire world all at once. The Red Sea issue that we're facing right now is a little more localized,” barring a wider conflict in the Middle East, he said.

Oil prices have yet to face serious consequences—but that could change quickly

When it comes to oil prices, the Red Sea crisis has had a smaller impact than what was seen during the pandemic or the outbreak of the Ukraine war. Although oil prices have steadily risen in recent weeks, they haven’t soared like they did after Russia’s 2022 invasion. WTI crude oil prices are up nearly 8% over the past month to just under $73 per barrel, but that’s still below the $86 per barrel price seen after the Israel-Hamas war began in early October. Compare that to the surge from roughly 60% surge to over $120 per barrel in the first three months of 2022, and this year’s crisis looks manageable.

View this interactive chart on Fortune.com

Jay Hatfield, founder and CEO of Infrastructure Capital Management, told Fortune that oil prices are still likely to rise over the next few weeks if the Red Sea crisis continues, but ultimately, rising U.S. crude supply, a nimble oil market, and favorable weather conditions will prevent a repeat of the Ukraine war’s crude disaster.

He noted the flexible nature of the crude market means that many suppliers will be able to shift their crude sales to avoid affected regions. And unlike two years ago, major oil-producing nations have yet to see their crude production affected by either the Israel-Hamas conflict or the Red Sea crisis. Plus, “even if every barrel of oil that was going to go to Europe had to be shipped around the horn [of Africa], it's about four bucks,” Hatfield added, referring to the minor potential increase in crude oil prices per barrel due to the current shipping issues.

Overall, Hatfield believes that the supply and demand dynamics in the oil market can’t support surging prices, especially after what has been an unseasonably warm winter. “Our whole thesis is that weather matters more than wars,” he said, arguing that oil prices could rise to $85 per barrel in the near term, but will stick in a range between $75 per barrel and $95 in 2024.

In a worst-case scenario where Iran gets involved and the global market loses 3 million barrels of oil per day produced there, oil prices could rise as high as $115 per barrel, Hatfield warned. But while that’s a significant jump, it’s an unlikely outcome.

Matt Stephani, president at Cavanal Hill Investment Management, echoed Hatfield’s outlook, noting that the Houthi attacks have caused a slight rise in oil prices in recent weeks, adding a “war premium,” as he calls it, but the impact of the Israel-Hamas war overall has been “minimal.”

“If the conflict were to spread to the other side of the Arabian peninsula, i.e. the Persian Gulf or Strait of Hormuz, oil markets may react much more significantly,” he said. “As of now…no supply has actually been halted and that war premium may decline if physical supplies are not disrupted.”

The Fed should stay the course—for now

How will all of this impact the Federal Reserve, which forecast three interest rate cuts for 2024 in its December Summary of Economic projections amid fading inflation? Like many of her peers, Lisa Pollina, an investment advisor at Ares and the former vice chairman for RBC Capital Markets, explained that it’s just not that easy to forecast.

“We just don't know what we don't know in terms of these exogenous shocks,” she told Fortune. “There could be more, whether it’s a widening war in the Middle East, U.S. involvement in the Middle East, or material war opening on a third front that impacts not only the U.S. involvement, U.S. military, but also NATO. And all of those things could have a significant effect on the US economy.”

While a widening conflict could certainly exacerbate inflation stateside and slow growth globally, Pollina said that she doesn’t believe the Red Sea crisis has changed the Fed’s thinking yet and they’re still likely to begin cutting interest rates in March.

“The Fed has no incentive to push us into a recession,” she said. “So they're going to watch things very closely. They could pause. Absolutely, there's a possibility of a pause. But I think it's less likely.”

Unlimited’s Elliott added that although the Red Sea crisis could exacerbate inflation or slow global growth, particularly if it worsens over the coming months, only paying attention to potential risks is likely a mistake. After all, he said, the U.S. economy has proved its resilience in the face of the Fed’s rapid interest rate hikes and foreign wars—which means maybe we should all worry a bit less.

“It's fashionable to go around talking about all the challenges in the economy, but, you know, the S&P 500 is at 4,800—all time highs. Growth is above potential. Unemployment is at secular lows…bond yields have declined,” he said. “When you look at things on an aggregate basis...when you synthesize the data across all the information that's available, what you see is you see things are going pretty well.”