The Bank of England raised its main interest rate for the eleventh time in a row to 4.25% at its March meeting. At its previous meeting in February the Bank was optimistic about the prospects for inflation in the coming year, saying: “We expect inflation to fall quickly this year.”

But in-between times, inflation hit 10.4%, with price increases for food and other essentials rising well above that rate. This is close to the highest levels for 40 years. The Bank’s main tool for tackling this rising cost of living is to raise interest rates, but this is starting to become harder to do.

One of the main reasons controlling inflation has become more difficult recently could be due to the return of monetarism. This is a theory promoted by the economist Milton Friedman in the 1970s. He believed there was a stable relationship between the supply of money and inflation. He explained this in the following terms:

Inflation is always and everywhere a monetary phenomenon in the sense that it is and can be produced only by a more rapid increase in the quantity of money than in output.

Monetarism was in vogue after Margaret Thatcher became UK prime minister in 1979. But it subsequently went out of fashion, largely because the predictable relationship between money and inflation disappeared. An increase in the money supply no longer appeared to increase inflation.

In the UK, the Monetary Policy Committee of the Bank of England is responsible for determining the Bank’s base rate of interest. This is the most important mechanism for changing the money supply because it is the basis for so many other interest rates – savings, mortgages and other loans – that affect how much money people have access to. For example, if the committee reduces the bank rate, this lowers the cost of credit which has the effect of boosting the money supply.

The recent return of the relationship between money supply and inflation is explained in a report from economist Claudio Borio and his colleagues at the Bank of International Settlements, a global organisation for central banks that aims to promote financial stability. They found, for example, that the money supply in the UK started to increase quite rapidly from the beginning of 2020 and by the middle of 2021 inflation took off. They also found a similar relationship exists in the US and in the Eurozone. Broadly speaking, this increase in money supply happened when central banks tried to counter the slowdown in spending caused by the pandemic.

The research also showed that the link between money and inflation only appears to work when inflation is high. This explains why it disappeared after Thatcher’s time in government and after the financial crash of 2008 – the rate of inflation was low at these times.

In the current environment, the Borio report shows that the Bank of England will have to continue raising interest rates if it is to effectively fight inflation. But the relatively long lag over a year before the policy begins to work will take us into 2024, which is an election year.

Until then, rising inflation and interest rates could cause more bankruptcies among financial institutions – such as we have seen with Silicon Valley Bank and Credit Suisse recently. This is also likely to harm the many businesses that rely on banks, not to mention increasing mortgage costs for millions of homeowners.

À lire aussi : Silicon Valley Bank: how interest rates helped trigger its collapse and what central bankers should do next

Inflation and government popularity

This is bad news for the government because history shows that the party in power loses votes when inflation is high. Low inflation appears to have no effect on government support, as opposed to unemployment, which always seems to have an effect.

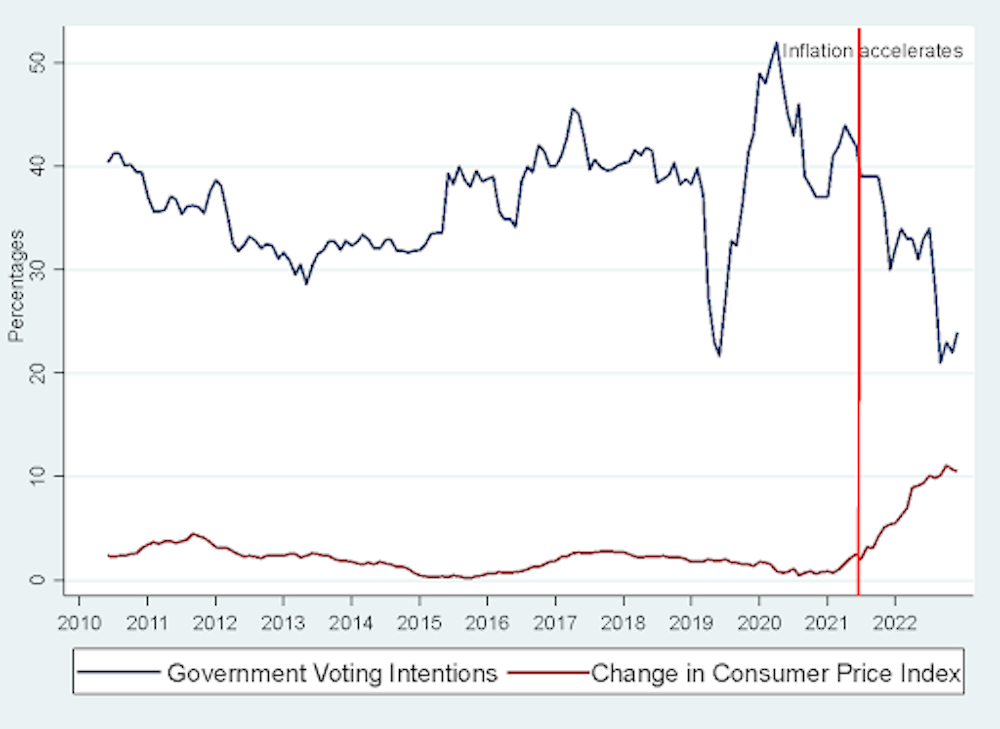

The effect of inflation can be seen in the graph below. It shows monthly voting intentions for the government and the inflation rate from the time of the 2010 election up to the end of 2022.

Inflation and voting intentions

The chart also shows that inflation only took off from the middle of 2021. In July of that year, it was running at 2% per year, but by July 2022 it was over 10%. The link between voting intentions and inflation up to July 2021 – before this increase started – was nonexistent. After that, it became a problem for the government (this point is marked on the graph above with a vertical red line).

Just as the money supply only affects inflation when the latter is high, it is also true that inflation only affects support for the government when it is high. Of course, following Liz Truss’s disastrous tenure in 10 Downing Street, Conservative voting intentions crashed, as the chart shows. This period contributed to the fall in Conservative voting intentions, along with rising inflation.

À lire aussi : Only a U-turn by the government or the Bank of England will calm UK financial markets

This also puts the Bank of England in a tricky position. If it overdoes interest rate rises, it could create a recession. On the other hand, if it does nothing, we could be facing a politically toxic combination of high inflation and high unemployment, known as “stagflation”. While the Bank of England makes interest rate decisions independently of the government, whatever it does is likely to influence the next election.

Paul Whiteley has received funding from the British Academy and the ESRC

This article was originally published on The Conversation. Read the original article.