With a market cap of $263.7 billion, Philip Morris International Inc. (PM) produces cigarettes and a range of smoke-free products, including heat-not-burn, e-vapor, and oral nicotine offerings under brands like IQOS, VEEV, and ZYN. It also sells consumer accessories and has expanded into wellness products.

Shares of the Stamford, Connecticut-based company have underperformed the broader market over the past 52 weeks. PM stock has decreased 2.8% over this time frame, while the broader S&P 500 Index ($SPX) has gained 28.5%. Moreover, shares of the company are up nearly 5% on a YTD basis, compared to SPX’s 6% increase.

Narrowing the focus, the tobacco giant stock has lagged behind the State Street Consumer Staples Select Sector SPDR ETF’s (XLP) 3% rise over the past 52 weeks.

Shares of Philip Morris soared 7% after it reported stronger-than-expected Q1 2026 results on Apr. 22, with revenue of $10.15 billion and adjusted EPS of $1.96. Investors were encouraged by solid growth in its international smoke-free segment, where shipments increased 11.9%, offsetting a 23.5% drop in the U.S. Zyn shipments. Despite a slight cut in full-year adjusted EPS guidance to $8.36 - $8.51, the midpoint still came in above analysts’ expectations.

For the fiscal year ending in December 2026, analysts expect PM’s EPS to grow 12.1% year-over-year to $8.45. The company’s earnings surprise history is promising. It beat the consensus estimates in the last four quarters.

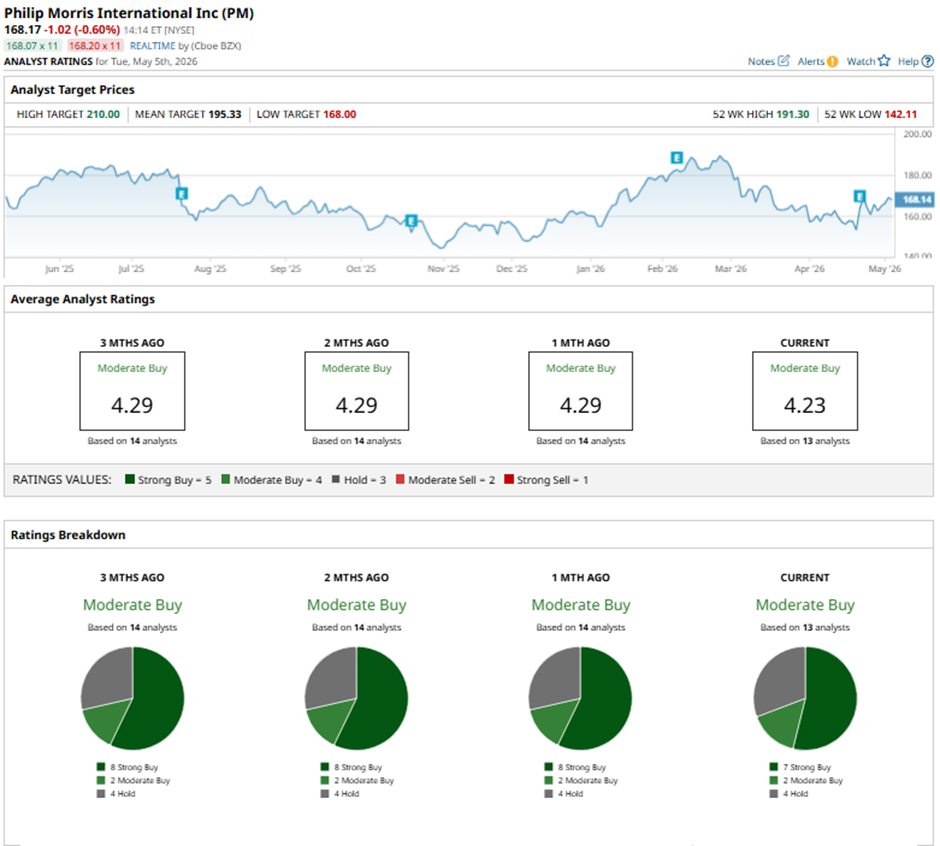

Among the 13 analysts covering the stock, the consensus rating is a “Moderate Buy.” That’s based on seven “Strong Buy” ratings, two “Moderate Buys,” and four “Holds.”

On Apr. 29, Citic lowered its price target for Philip Morris to $180 while maintaining an “Add rating” on the stock.

The mean price target of $195.33 represents a 16.2% premium to Philip Morris’ current price levels. The Street-high price target of $210 suggests a 24.9% potential upside.