/A%20Palantir%20sign%20displayed%20on%20an%20office%20building%20by%20Poetra_RH%20via%20Shutterstock.jpg)

Palantir Technologies (PLTR) is a premier U.S. data analytics and software company that assists governments with defense-focused solutions and has successfully expanded its core mission into the global corporate sector. Today, Palantir operates three primary platforms: Gotham, Foundry, and its cutting-edge Artificial Intelligence Platform (AIP). These platforms serve as the firm's central operating infrastructure for massive institutional data integration.

Amid a highly volatile, multi-month stretch for global equity markets, mega-cap tech stocks have seen aggressive profit-taking, with Palantir emerging as one of the primary laggards. Let's take a closer look.

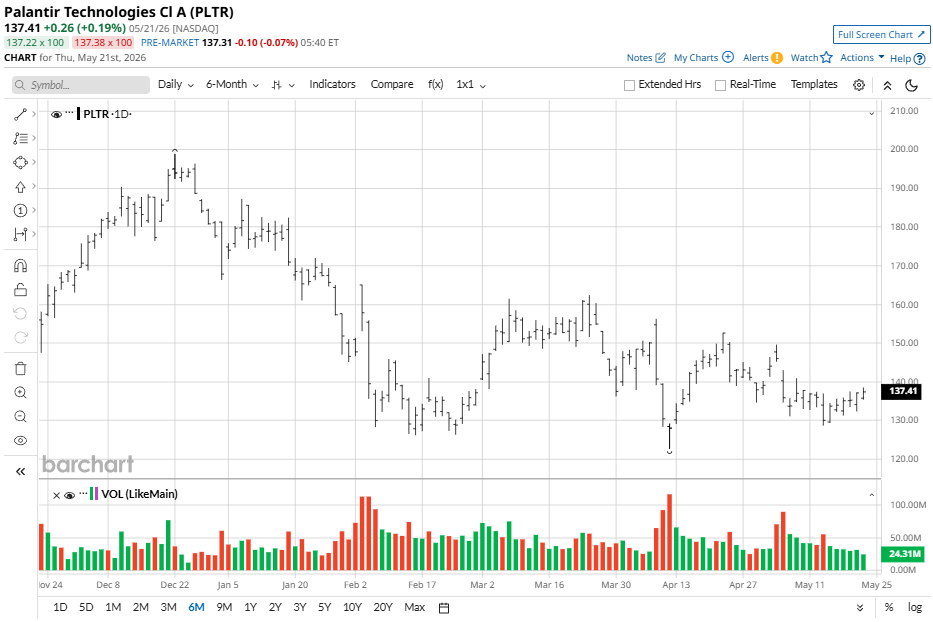

Palantir's Year-to-Date Reality Check

In a newly compiled list tracking the 10 worst year-to-date (YTD) underperformers among companies with a market capitalization of $200 billion or more, Palantir sits near the top. Carrying a steep decline of 25% YTD when the list was compiled, Palantir was outpaced in losses only by IBM (IBM), which was down more than 26%. However, as of this writing, PLTR stock is down by 23% YTD while IBM's loss has softened to roughly 14% so far in 2026.

This massive valuation pullback across the mega-cap space has triggered a broader cautious shift in market sentiment. Reflecting this cooling momentum, Palantir carries a neutral Seeking Alpha Quant Rating of “Hold,” a score it shares with fellow underperformers on the list, including Microsoft (MSFT), Visa (V), and Mastercard (MA).

Palantir Posts Strong Results

Palantir delivered a spectacular financial performance for the first quarter of 2026, marking its strongest three-month stretch as a publicly traded enterprise. Total quarterly revenue skyrocketed 85% year-over-year (YOY) to $1.63 billion, soundly beating Wall Street consensus estimates.

The hyper-growth engine was overwhelmingly supercharged by U.S. revenue, which jumped 104% YOY to $1.28 billion, accounting for about 79% of total sales. Crucially, U.S. commercial revenue surged an astronomical 133% YOY to $595 million, driven by relentless, boot camp-led enterprise conversions for its foundational AIP infrastructure. Meanwhile, U.S. government revenue advanced 84% YOY to $687 million.

Corporate profitability reached unprecedented heights alongside the top-line expansion. GAAP net income soared to $871 million, translating into a highly lucrative 53% margin and delivering GAAP diluted EPS of $0.34, which topped forecasts. Operationally, the company recorded an adjusted operating margin of 60% and achieved a monumental Rule of 40 score of 145%, backed by a pristine balance sheet holding $8 billion in cash and short-term Treasurys.

Management aggressively raised its full-year 2026 revenue guidance to a range of $7.65 billion to $7.66 billion, reflecting compounding confidence in U.S. commercial enterprise demand.

What Should You Do With PLTR Stock?

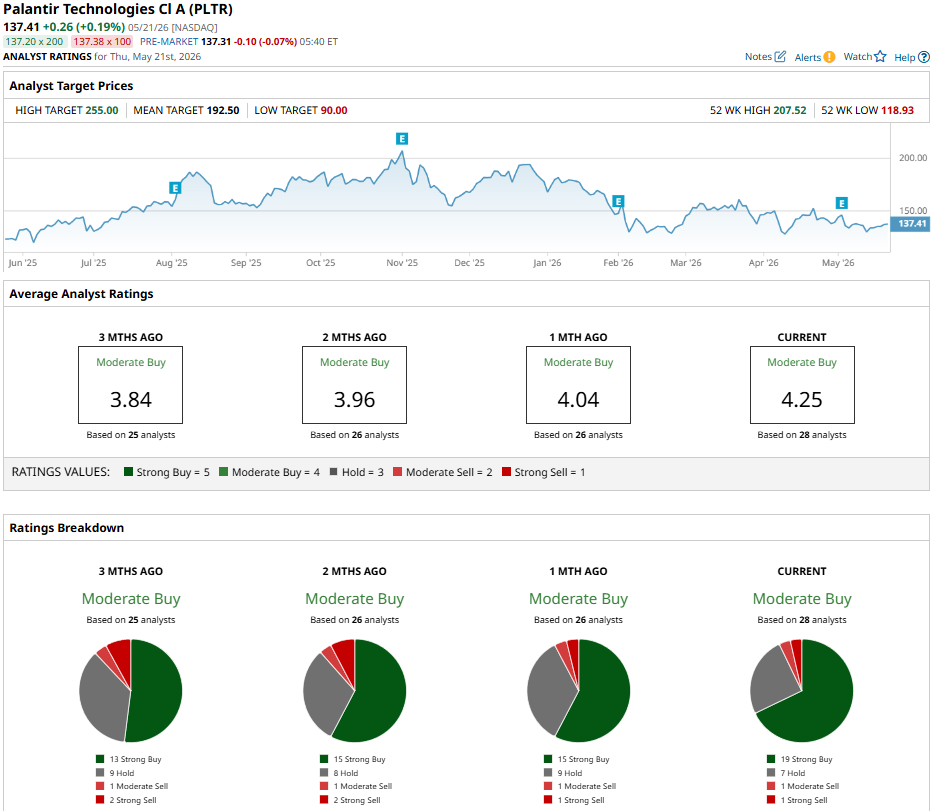

Palantir’s sharp YTD decline reflects widespread valuation compression among mega-cap tech giants rather than operational decay. Under the surface, its commercial blueprint remains intact, sustaining a Wall Street consensus "Moderate Buy" rating. Out of 28 analysts with coverage, 19 have a "Strong Buy" rating, seven analysts have a "Hold," one has a "Moderate Sell," and one has a “Strong Sell” rating.

The mean price target of $194.81 suggest impressive 42% potential upside from current levels. That presents an ideal entry window for long-term growth investors.