/Netflix%20on%20tv%20with%20remote%20by%20freestocks%20via%20Unsplash.jpg)

Netflix (NFLX) stock declined sharply, falling about 10% in pre-market trading, following its first-quarter earnings release. The selloff occurred despite the top-line result exceeding consensus expectations.

For the quarter, Netflix reported revenue of $12.25 billion, a 16.2% year-over-year (YoY) increase that surpassed analyst forecasts. Earnings per share reached $1.23, nearly doubling from $0.66 in the prior-year period. This upside was driven by stronger-than-expected operating income, alongside a one-time $2.8 billion termination fee tied to its transaction with Warner Bros. Discovery (WBD).

While these numbers show solid operational execution and continued platform scale, a portion of the earnings strength was non-recurring.

However, the market’s negative reaction was more about forward guidance. Management maintained its 2026 revenue outlook despite the first quarter benefiting from stronger-than-anticipated subscriber growth. This suggests a more cautious internal view on the sustainability of recent momentum, raising concerns about a potential deceleration in top-line expansion. For a company priced on growth durability, even a subtle indication of a slowing trajectory can trigger a stock selloff.

The margin outlook further compounded investor concerns. Netflix guided to a second-quarter operating margin of 32.6%, down from 34.1% in the comparable prior-year period. The expected compression is largely attributed to higher content amortization, reflecting the ongoing need to invest aggressively in programming to remain competitive.

Adding to the uncertainty is a forthcoming leadership transition. Co-founder and chairman Reed Hastings is set to step down from the board when his term expires in June. Founder departures often prompt reassessment of strategic continuity, governance oversight, and long-term vision. In Netflix’s case, this transition carries additional weight given the company’s position in a highly competitive global streaming landscape, where execution discipline and content strategy are critical to maintaining market leadership.

Taken together, the post-earnings decline reflects a recalibration of expectations. Netflix continues to demonstrate operational strength, but questions around growth sustainability, margin trajectory, and leadership continuity are now central to the investment narrative.

Here's NFLX Stock’s Bull Case

The recent selloff in NFLX stock suggests the market may be disproportionately pricing in near-term risks while overlooking the company’s longer-term structural advantages. Despite short-term volatility, Netflix continues to show strong platform engagement, reflected through a steady pipeline of high-quality content. Its solid content slate remains a key driver of subscriber retention and new user acquisition, strengthening the platform’s competitive positioning.

Netflix is broadening its content to include formats such as video podcasts and gaming. This diversification reflects a strategic effort to increase user engagement on the platform and drive its market share.

Equally important is Netflix’s pricing power. The company has successfully implemented price increases recently while growing its subscriber base in Q1. This shows Netflix's strong brand and high perceived value among its user base. This ability to raise prices without materially impacting demand is one of the key drivers of Netflix’s long-term revenue growth and margin expansion.

Another growth catalyst is Netflix’s advertising-supported tier. The company’s ad business is scaling rapidly, with revenue projected to double in 2026 and reach approximately $3 billion. As this segment matures, it introduces a complementary revenue stream that could carry higher incremental margins than the core subscription model. Moreover, the ad-supported offering expands Netflix’s addressable market by appealing to more price-sensitive consumers while creating additional monetization avenues.

From a profitability standpoint, near-term margin pressure remains a consideration, particularly in the second quarter. However, management has guided toward YoY operating margin expansion in the second half of the year and reaffirmed its full-year operating margin target of 31.5%.

Valuation has always played a key role in the investment debate around NFLX stock. Historically, NFLX stock has traded at a premium, and that premium is warranted given its solid content and pricing power. Moreover, the recent correction will likely reset expectations. With the stock trading at approximately 33.4 times forward earnings, a level that could compress further, the pullback creates a more attractive entry point for long-term investors.

Overall, Netflix’s sustained engagement metrics, pricing leverage, and the rapid development of its advertising business form the foundation of a credible bull case. While short-term uncertainties persist, the underlying business dynamics suggest the post-earnings decline may present an opportunity to buy.

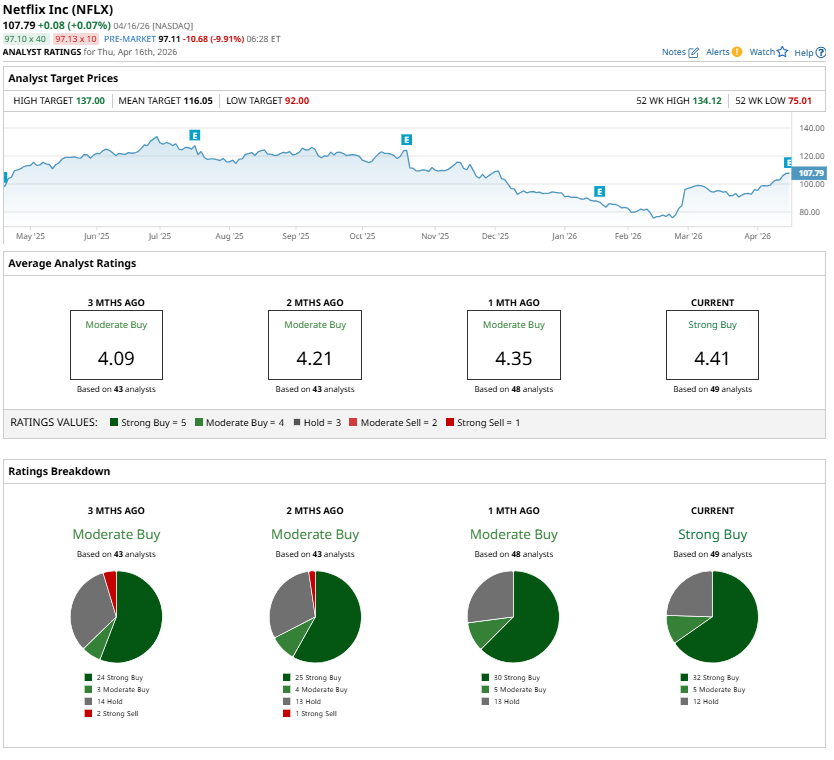

Analysts are bullish and maintain a “Strong Buy” consensus rating on NFLX stock.