/Women%20sitting%20on%20roling%20chair%20in%20front%20of%20computer%20monitors%20by%20ThisisEngineering%20via%20Unsplash.jpg)

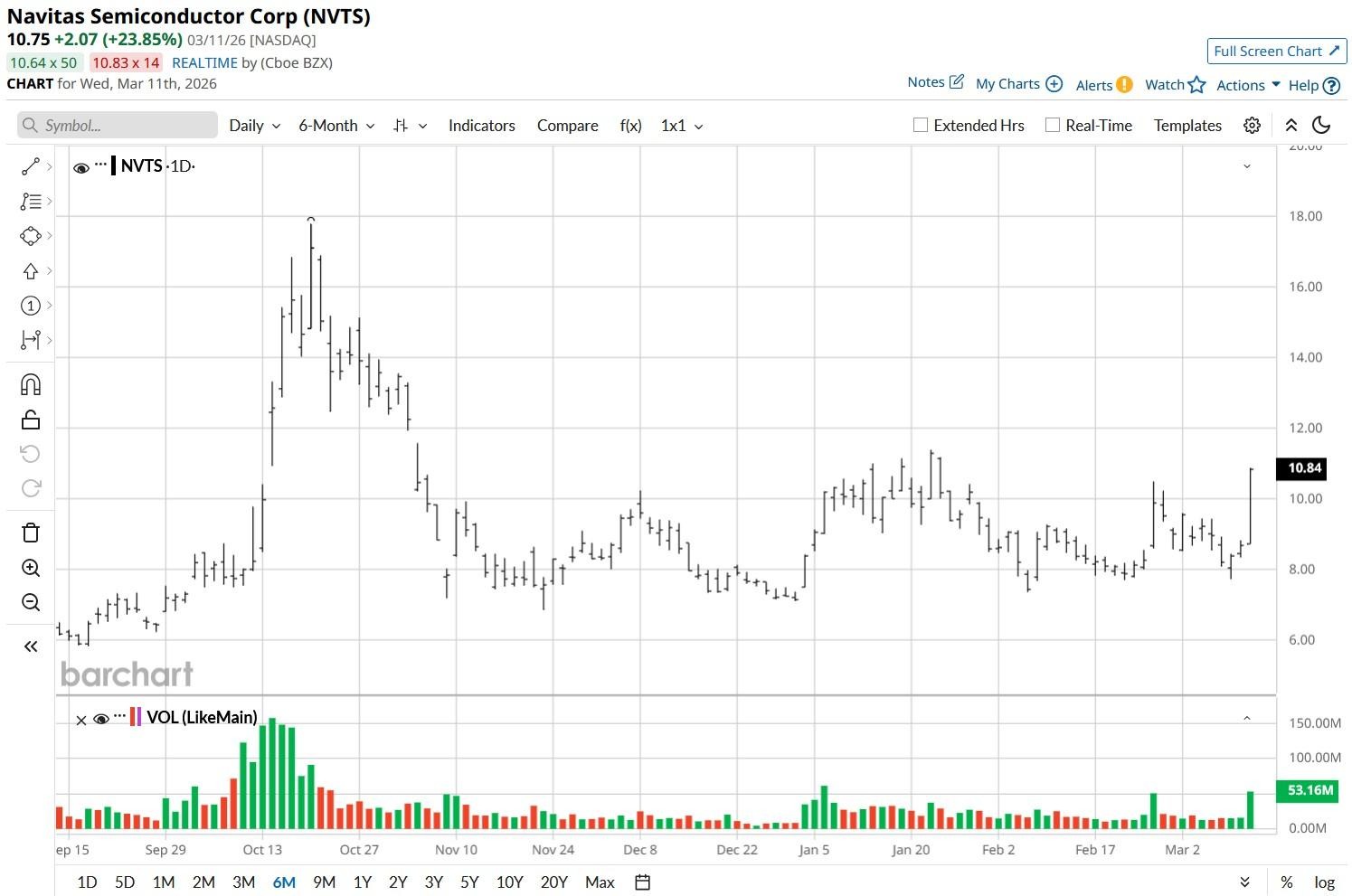

Navitas (NVTS) stock charged higher on Wednesday after the company launched its fifth-generation GeneSiC silicon carbide (SiC) power semiconductor platform.

Featuring advanced MOSFETs and “high-efficiency” packaging for artificial intelligence (AI) data centers, the announcement helps NVTS rally past its major moving averages (20-day, 50-day, 100-day), indicating bulls firmly taken control across multiple timeframes.

Despite their meteoric run on March 11, Navitas shares remain down about 4% versus their year-to-date high.

Does the Launch Warrant Buying Navitas Stock?

Navitas’s latest GeneSiC platform directly addresses the thermal and efficiency bottlenecks currently throttling AI scaling.

These 1200V Trench-Assisted Planar (TAP) MOSFETs deliver 35% improvement in performance figures, allowing AI data centers to handle much higher power densities with cooler operation.

By introducing top-side cooled (TSC) QDPAK packaging, Navitas is helping server-makers shrink power supply footprints while increasing output — a key requirement for next-gen GPU racks.

This product roadmap confirms that Navitas is no longer just a charger company but a critical component provider for the AI power path from the grid to the processor.

Investors cheered NVTS stock on Wednesday as it validates the firm’s transition from low-margin mobile markets to high-growth artificial intelligence infrastructure.

Why Else Are NVTS Shares Worth Owning?

The broader bull case for Navitas shares is anchored by its inclusion in Nvidia’s 800V "AI factory" ecosystem and a projected serviceable addressable market (SAM) of about $3.5 billion by 2030.

While currently unprofitable, Navitas maintains a strong $160 million cash cushion and has guided for Q1 revenue of up to $8.5 million, exceeding analyst consensus.

With mobile revenue now comprising less than 25% of the mix, the margin profile is set to expand as high-power AI and grid infrastructure sales take the lead.

According to experts, if Navitas delivers on its 32% annual revenue growth ambition — the current valuation would prove a ground-floor entry into a pure-play AI infrastructure winner.

Note that NVTS’s relative strength index (14-day) sits at about 62 currently, reinforcing that bullish momentum remains far from exhaustion in the near term.

How Wall Street Recommends Playing Navitas

Despite a sharp rally and premium valuation of about 42x sales, Wall Street firms remain somewhat bullish on NVTS shares.

While the consensus rating on Navitas Semiconductor sits at a “Hold” only, the price targets go as high as $13, signaling potential upside of another 20% from here.

This article was created with the support of automated content tools from our partners at Sigma.AI. Together, our financial data and AI solutions help us to deliver more informed market headline analysis to readers faster than ever.