Mortgage rates are plummeting this week after two cooler-than-expected inflation reports gave Wall Street hope that the Federal Reserve’s interest rate hikes are working their magic. For more than 20 months, Fed officials have rapidly hiked rates in an attempt to quash inflation, contributing to an affordability crisis within the housing market as the cost of borrowing to buy a home surged.

But with inflation fading and the labor market cooling, many economists now believe the Fed is set to cut interest rates in the coming months. The new outlook helped push the average 30-year fixed mortgage rate down to just 7.37% on Friday. That’s a big drop from the over 8% rate just a month ago. And real estate experts say consumers should expect mortgage rates to continue falling in 2024.

“There is room for mortgage rates to fall further,” Bright MLS chief economist Lisa Sturtevant said Wednesday, pointing to the historic gap between the 10-year Treasury yield and 30-year fixed mortgage rate, which typically trade at similar levels.

For beleaguered homebuyers, this is potentially a very big deal, considering that skyrocketing mortgage rates coupled with home prices that rose substantially during the pandemic sent affordability to multi-decade lows in recent years, drawing comparisons from Wall Street banks and Fortune 500 economists to the 18% mortgage rates from the 1980s housing market. But mortgage rates falling now doesn’t mean home prices are set to fall, too.

Lower rates also mean higher demand

Lower rates will provide some relief for homebuyers, but Sturtevant warned that the rush to take advantage of the recent drop in mortgage rates at a time when the supply of homes is “limited” could cause problems. That means mortgage rates won’t come down quickly, “nor will they decline to the sub-5% level that we have had since the Great Recession,” she said.

Citi economist Veronica Clark warned in a Friday note that she even expects “upward pressure on home prices in the near term” due to the limited inventory of homes and rising mortgage demand. Morgan Stanley and Goldman Sachs have also forecasted higher home prices this year and next, respectively.

Rising home prices would definitely put a dent in the affordability benefit of the recent drop in mortgage rates for consumers given how high they’ve gotten. With that in mind, Sturtevant said: “For those homebuyers who can wait, the spring will bring more new listings and lower mortgage rates.”

If mortgage rates were to fall low enough, that could entice would-be sellers to put their homes on the market in the spring—lessening the lock-in effect that’s largely pushed existing home sales to their lowest level in more than a decade and exacerbated supply constraints.

It’s still a renters’ and sellers’ market—for now

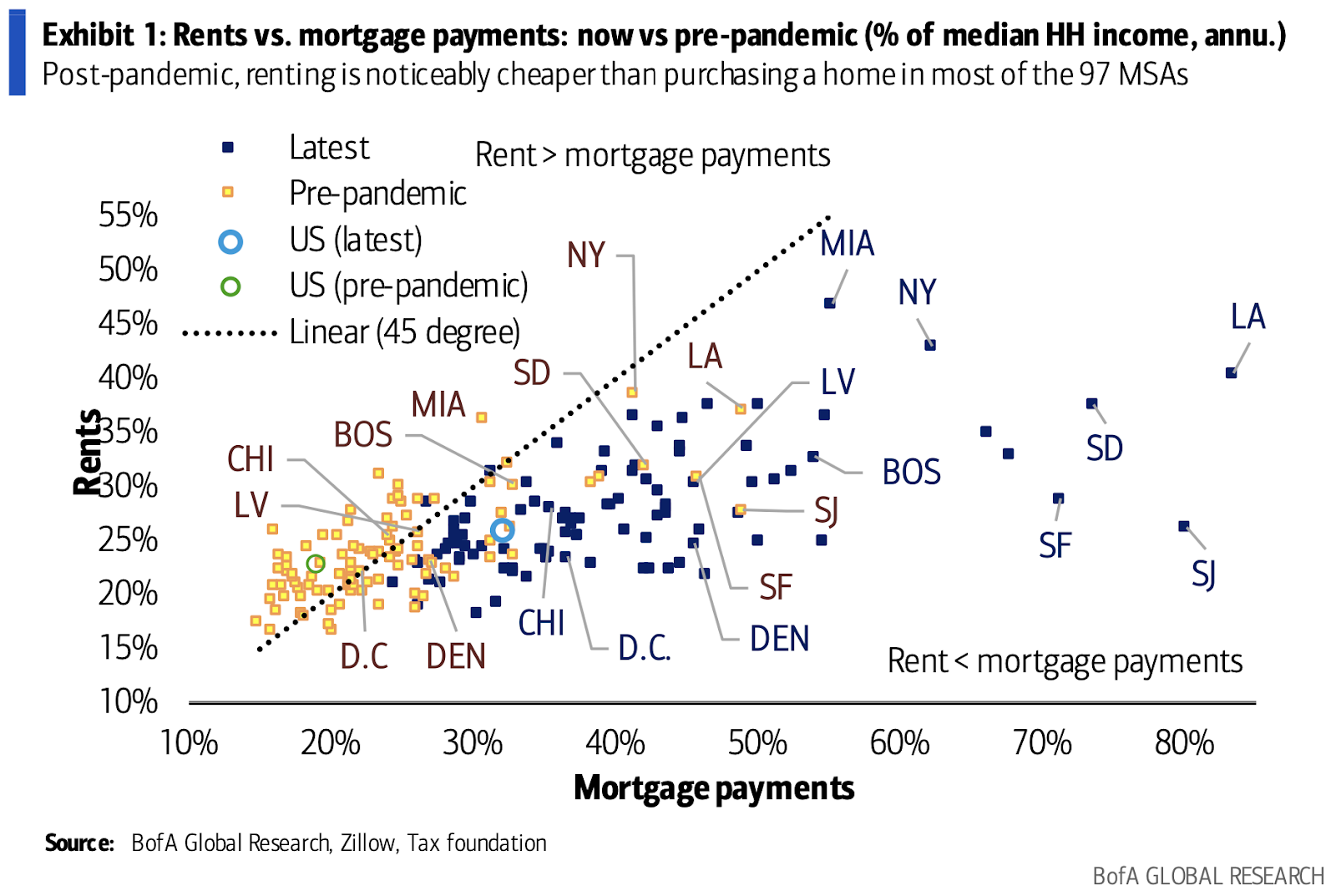

After living through a sellers’ market for years, the recent drop in mortgage rates is undoubtedly “good news” for buyers, according to Bank of America’s U.S. economist Jeseo Park. But Park warned in a Thursday note that, according to her analysis, renting is still cheaper than buying in 95 out of 97 major Metro Areas. Realtor.com’s recently released report also found that it’s cheaper to rent than buy in nearly every major market as the rental market continues to soften.

On top of that, Park still believes that homebuyers will have to reckon with a “higher-for-longer” interest rate environment for years to come, even if housing affordability will “likely improve” as the Fed cuts rates. The days of 3% mortgage rates may be over.

Homebuilders don’t seem to be worried about the demand for new homes amid the affordability crisis, however. That could be evidence that homebuilders expect mortgage rates to fall more than Wall Street. Total new home starts rose 1.9% in October, while building permits for the construction of single-family homes jumped 0.5%.

“Builders are ramping up construction as they expect mortgage rates to continue leveling off,” Quincy Krosby, chief global strategist at LPL Financial, said of the data. “Builders undoubtedly perceive there's a viable market for new housing and that they can sell the houses fairly quickly.”

Still, there could be other reasons for homebuilders’ bullishness. The new home sales market has outperformed the existing home sales market, and homebuilders can offer incentives like mortgage rate buydowns, to incentivize consumers to buy.