/Micron%20Technology%20Inc_billboard-by%20Poetra_RH%20via%20Shutterstock.jpg)

Artificial intelligence (AI) is no longer just driving demand for chips — it’s exposing every weak link in the semiconductor supply chain. GPUs from Nvidia (NVDA) tend to grab the headlines, but memory has quietly become the choke point. Massive AI models need enormous amounts of data moved at blistering speeds in real time, and traditional memory simply cannot keep up. That has created a shortage unlike anything the memory industry has seen in decades.

The question for investors is simple: Which company is best positioned for this moment? Wall Street seems to increasingly believe the answer is Micron Technology (MU).

The AI Memory Bottleneck Is Getting Worse

Training large AI models requires huge pools of high-bandwidth memory (HBM) alongside advanced DRAM chips capable of feeding GPUs continuously. Without enough memory bandwidth, even the fastest AI accelerators sit idle.

That imbalance has become severe. According to Micron, its entire 2026 supply of HBM4 is already sold out. Even more telling, the company said it can currently satisfy only 50% to 66% of key customers’ medium-term bit demand because of limited clean room capacity.

Simply put, customers want far more memory than Micron can physically produce. That matters because HBM pricing runs several times higher per bit than traditional DRAM.

With that in mind, let’s compare the major memory players:

| Company | Global DRAM Market Share | Global HBM Market Share | Key Advantage |

| Samsung Electronics | 38% | 22% | Scale and manufacturing |

| SK Hynix | 29% | 57% | Early AI partnerships |

| Micron Technology | 22% | 21% | Premium HBM margins, fastest growth |

Surprisingly, being third may have actually helped Micron. The company has moved aggressively into higher-margin HBM production instead of chasing lower-margin commodity DRAM volume. Management has openly acknowledged it is prioritizing HBM output because profitability is materially higher.

That strategy is now reshaping the company.

Wall Street Finally Catches Up

For most of the past decade, memory stocks have been treated like cyclical commodities — boom, bust, repeat. But AI is changing that framework.

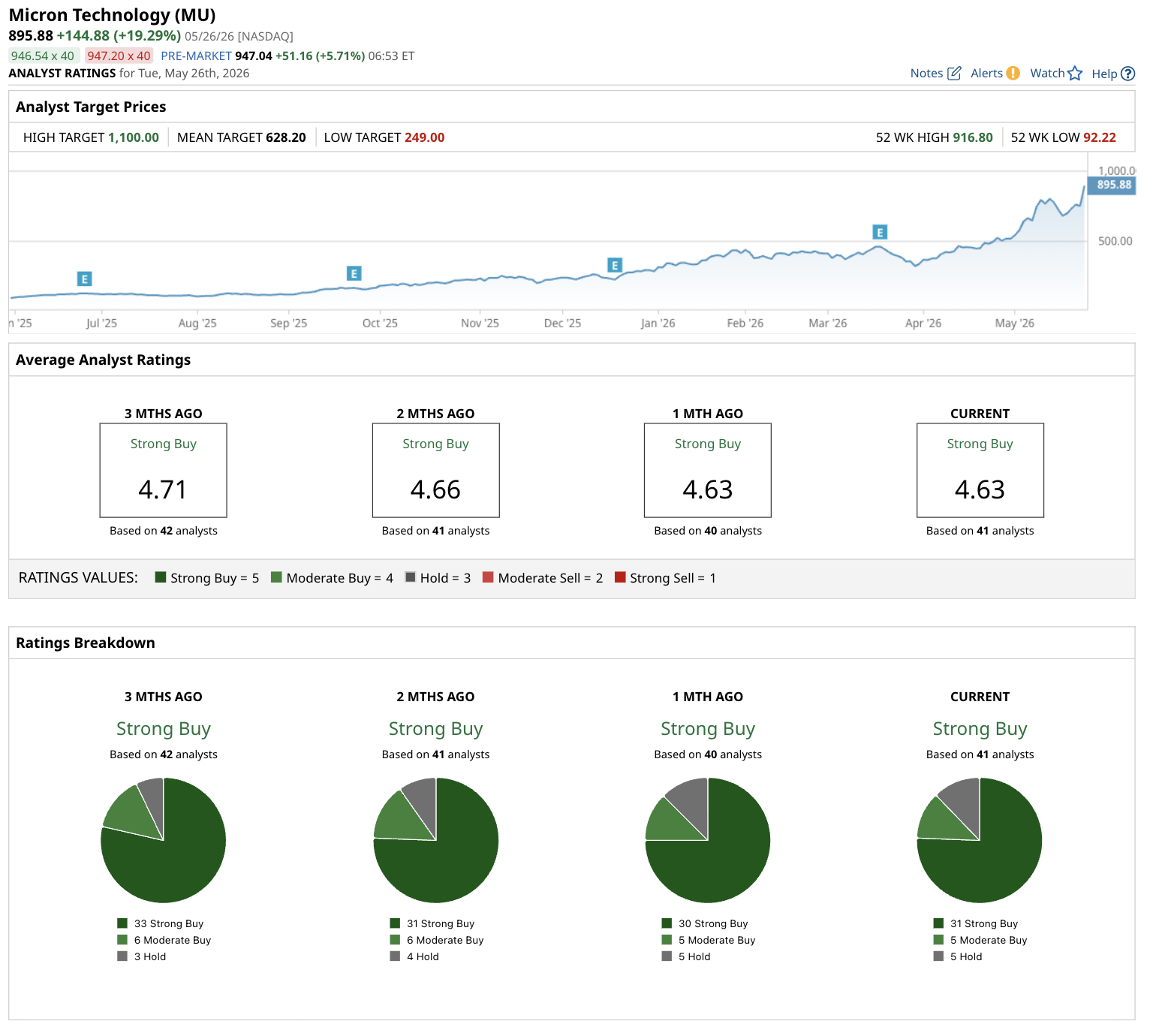

UBS analyst Timothy Arcuri recently raised his price target on MU stock from $535 to $1,625, arguing that the market still underestimates the structural shift taking place in AI memory demand.

The stock responded immediately. Micron jumped $144 in one session, rising more than 19% to $895.88 on May 26. The next day, shares closed at $928.41, up another 4%. That means Micron added more than $220 billion in market value in about 24 hours. But what reframes the story for investors is that, just over a year ago, Micron’s entire market capitalization sat near $77 billion. In other words, the company added about three times last year’s total valuation in a single trading day.

Micron is now worth $1.01 trillion, making it the 11th-largest company by market cap.

Granted, some of this move reflects momentum trading. A stock rising 860% in one year naturally attracts speculation. That said, there is also fundamental math behind the rally.

Why Micron May Still Have Room to Run

The AI infrastructure buildout is still in its early innings. Cloud providers, sovereign AI projects, hyperscalers, and enterprise customers continue to pour hundreds of billions of dollars into AI systems that require enormous memory capacity. And unlike GPUs, memory cannot simply be replaced with software optimization.

Micron’s constraints actually reinforce pricing power. If demand exceeds supply through 2026 — and management’s sold-out HBM4 production suggests it will — margins could remain elevated far longer than investors previously modeled.

Regardless of how you look at it, the memory market has changed. AI has transformed DRAM and HBM from cyclical components into strategic infrastructure.

Key Takeaway

In short, Micron is no longer being valued like a traditional memory company. Investors are increasingly pricing it like a critical AI infrastructure provider.

Could MU stock pull back after such a rapid rise? Of course. Stocks rarely move from a $77 billion valuation to over $1 trillion without periods of volatility. But the underlying drivers — constrained HBM supply, premium pricing, and relentless AI demand — remain firmly intact.

For sharp investors, the key question is no longer whether AI needs more memory; the data already answers that. The real question is whether the world can build enough of it fast enough. Right now, Micron appears to hold one of the most valuable seats at that table.