/Facebook-you've%20been%20Zucked%20by%20Annie%20Spratt%20via%20Unsplash.jpg)

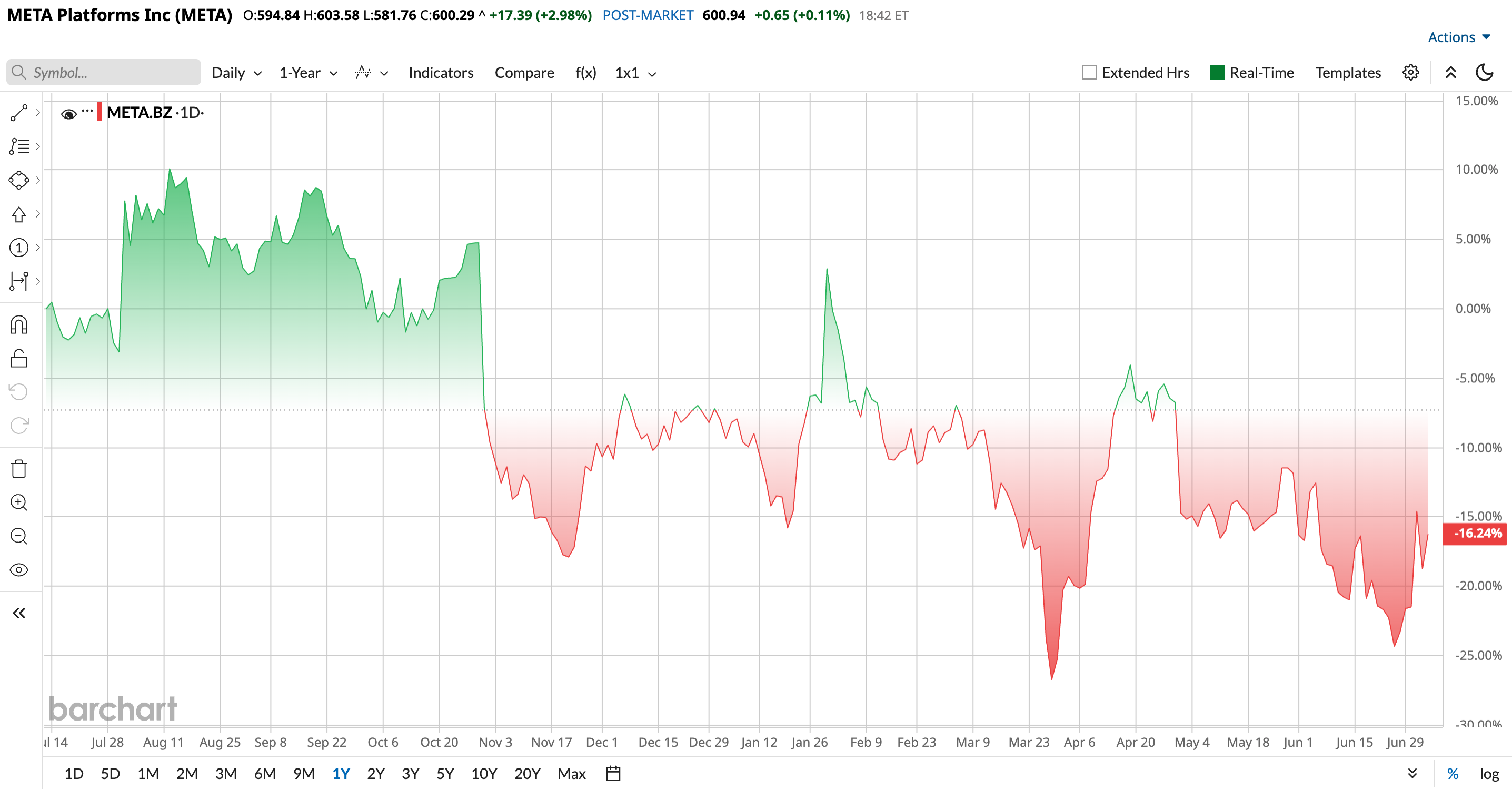

Meta Platforms (META) stock has hit a rough patch recently. Meta reached a high near $796 during 2025. Strong advertising demand and AI enthusiasm helped drive that rally.

But changed happened in 2026. Shares pulled back 9.1% year-to-date (YTD) and at one point fell more than 25% from peak levels. The weakness was not driven by slowing business trends. Instead, investors worried about rising costs.

But Goldman Sachs thinks investors may be looking at an opportunity instead of a problem.

Meta raised its AI infrastructure spending outlook to between $125 billion and $145 billion. Those numbers are massive. Some investors worry that heavy spending today could pressure profits tomorrow. Yet, investors have still become cautious ahead of the next earnings release. That disconnect is exactly why Goldman believes the recent weakness may create an attractive entry point.

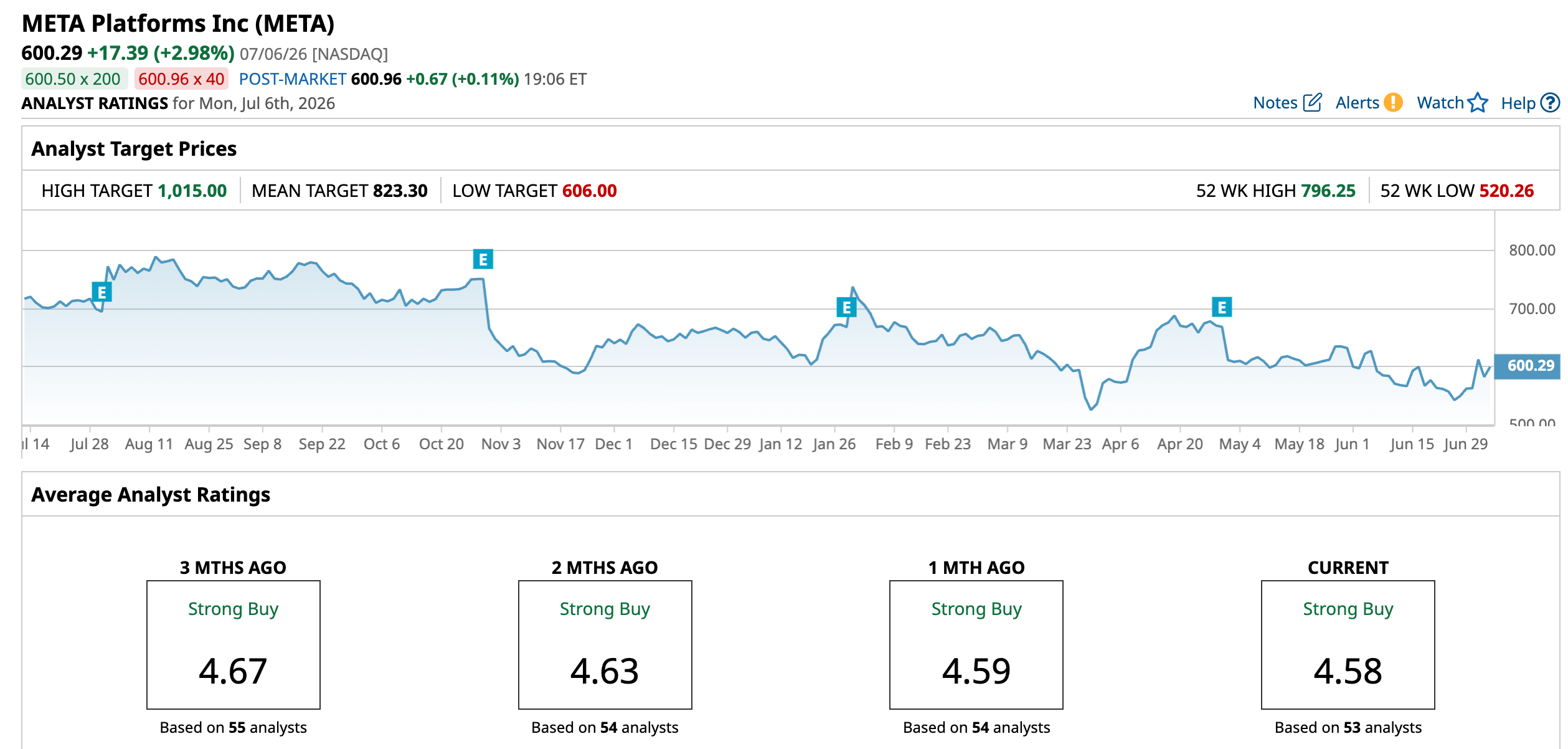

Also, legal concerns created pressure. But Goldman Sachs appears to believe the market reaction has gone too far. The firm recently maintained its “Buy” rating and kept a target price of $830.

Meta Delivered Another Strong Quarter

Meta Q1 results gave investors several reasons to stay positive. Revenue reached $56.31 billion, rising 33% year-over-year (YOY). The company also topped analyst expectations. Adjusted earnings per share came in at $7.31, above consensus estimates near $6.67. The biggest growth engine remained advertising. Family of Apps revenue generated roughly $55.9 billion during the quarter. Reality Labs contributed about $400 million.

Profit growth looked even stronger. Net income jumped 61% YOY to $26.77 billion.

Also, Meta provided a solid outlook for the current quarter. Management guided second-quarter 2026 revenue to a range of $58 billion to $61 billion, with the midpoint at $59.5 billion. The guidance assumes foreign exchange provides roughly a 2% tailwind to YOY growth.

Wall Street expectations currently sit near the midpoint of that range, suggesting analysts continue to expect healthy advertising demand and strong momentum across Meta's AI-driven products and platforms.

Why Goldman Sachs Sees Meta as a Buy Ahead of Earnings

Goldman Sachs is bullish on Meta because it expects the market to place too much emphasis on near-term spending on AI and not enough on its growing earnings potential. Meta's latest sell-off may have driven down valuation amid robust demand for ads and solid profit performance. These steady earnings and advertising demand have been curtailed by a recent sell-off by Meta that has reduced valuation.

Goldman said that there's also been a mismatch between growth in earnings forecasts and share performance. As long as future results indicate that a continued investment in AI is leading to increased revenue, engagement, and monetization, sentiment could turn around swiftly, and a turnaround may take effect.

What Analysts Think of META Stock

Analysts still appear largely positive on Meta. Other than Goldman Sachs, Morgan Stanley also maintained an “Overweight” rating and sees shares reaching $775.

Evercore became even more bullish and raised its target to $930 after highlighting Meta's AI progress. Stifel stayed positive but lowered its target to $780 because of spending concerns.

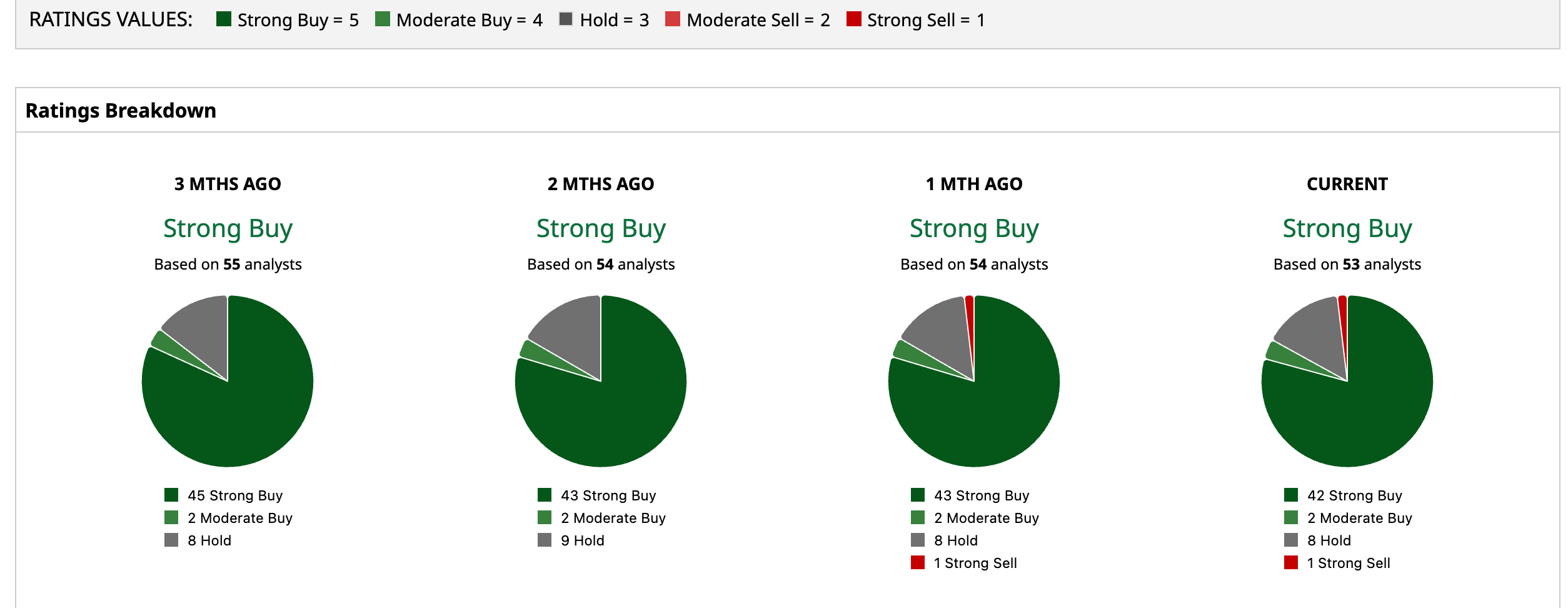

Data currently shows a “Strong Buy” consensus rating on Meta stock with an average target $823.30. That suggests a massive upside of 37.2% from the current price.

Wall Street clearly sees near-term risks. But analysts still appear to believe Meta's core advertising business, AI investments, and long-term growth opportunities make the recent dip worth buying.