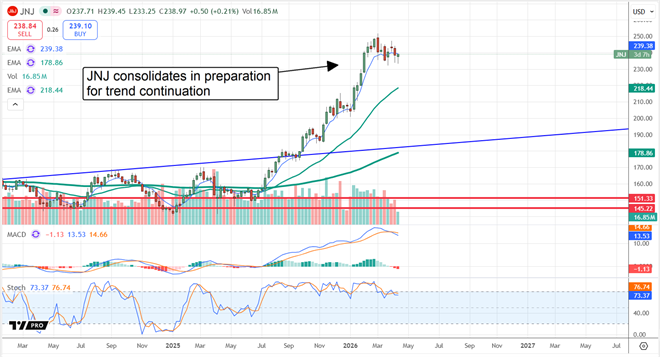

Johnson & Johnson’s (NYSE: JNJ) price action entered consolidation in early March. While it may continue moving sideways or even pull back further, those moves are unlikely, given a convergence of factors.

Price action and accelerating growth suggest the March pullback is a continuation signal and a buying opportunity likely to lead to much higher prices down the road. Among the highlights from the recent Q1 earnings release were numerous approvals and pipeline updates, which led management to increase guidance and affirm a double-digit revenue growth pace by the decade’s end.

Technically speaking, JNJ’s stock price consolidation bears the hallmarks of a Bull Flag or Pennant formation. These formations mark stopping points within a rally, and bring easily identifiable targets into play when confirmed.

Confirmation is primarily through price action; it includes the setting of new highs and subsequent testing of support following the breakout.

The critical resistance point for this market is $250 as of mid-April. If broken and confirmed as support, the initial target for upside advance is about $35, or the magnitude of the rally preceding the pattern. Assuming the company continues executing its strategy and building its revenue base, the bull-case targets equalling the percentage gain of the move preceding the pattern, worth about 17% from the breakout point, come into play. That could put this market in the $290 range within a few months of setting the new high.

Johnson & Johnson Pulls Back Following Hot Quarter and Raised Guidance

Johnson & Johnson had a solid quarter, with revenue growing 9.9% driven by organic gains, acquisitions, and foreign exchange tailwinds. The revenue outpaced MarketBeat’s consensus by more than 190 basis points, with strength in both core segments. Innovative Medicine grew by 11.2%, underpinned by strength in the oncology segment, while Med Tech grew at a slower 7.7% rate. Regionally, sales in the United States were solid at up 8.3%, led by a stronger 11.9% gain internationally.

Margin and guidance were also bullish, albeit insufficient to spark a rally on their own. The company’s margin compressed significantly due to patent expiration and increased competition for Stellara. The good news is that the impact was only slightly worse than expected and offset by revenue strength. The bad news is that earnings contracted. The bottom line is that $2.70 in adjusted earnings per share is down 2.5% compared to last year, but outpaced the consensus by 2 cents (75 bps), trailing the top-line strength by more than 100 bps.

Guidance was tepid, despite the increase, compared to analyst trends. The company raised its fiscal year 2026 forecast to align with the consensus estimate, expecting earnings growth of 7% at the midpoint. The opportunity for investors is that accelerating growth could lead to outperformance in upcoming quarters, and that new approvals could lead to improving margins as the company’s pipeline is monetized.

Institutions and Analysts Underpin JNJ’s 2026 Stock Price Increase

Institutional activity is noteworthy, as it spiked in Q1, aligning with the stock price increase that pushed it to new highs. With them owning nearly 70% of the stock and the outlook for accelerating business, it is unlikely they will revert to distribution soon, instead sticking to accumulation as the story plays out.

Analyst trends have also been bullish, with them lifting price targets and sentiment ratings ahead of the report. As it stands, the group rates JNJ as a Moderate Buy with 67% Buy-side bias, no Sell ratings are logged, and the consensus price target is trending higher.

Offering only a slim upside in April, the high-end analyst price target suggests 20% upside is available, aligning with the technical $290 target. Short interest is not a factor in this market, as it remains below 1% and is unlikely to increase.

Dividends are among the reasons sell-side interest is so strong. The company’s 2% yield is reliable, grows annually, and is backed up by a healthy balance sheet. The company uses debt to fund cash and capital needs, but maintains a healthy profile and sufficient free cash flow to sustain distributions and growth. As it stands, JNJ has increased its payment for more than 60 years and has the capacity to continue the trend for the foreseeable future.

The biggest risks for JNJ are ongoing patent expirations and their impact on revenue and margin. However, the company’s pipeline is robust, with leading candidates expected to drive 5% to 7% in annualized revenue growth over the next four to five years. The company is also focusing on Med Tech, with the Cardiovascular unit specifically driving growth through several platforms. Surgical Robotics is another focus, with the OTTAVA system expected to receive approval by late this year. Surgical Robotics is a fast-growing industry, expected to quadruple in size over the coming decade.

Where Should You Invest $1,000 Right Now?

Before you make your next trade, you'll want to hear this.

MarketBeat keeps track of Wall Street's top-rated and best performing research analysts and the stocks they recommend to their clients on a daily basis.

Our team has identified the five stocks that top analysts are quietly whispering to their clients to buy now before the broader market catches on... and none of the big name stocks were on the list.

They believe these five stocks are the five best companies for investors to buy now...

The article "Johnson & Johnson: A 20% Gain Looks Easy After Q1 Earnings Results" first appeared on MarketBeat.