Your work doesn’t end merely after filing your Income Tax Return (ITR). Taxpayers often delete or misplace important tax records, assuming they won't need them again after filing the ITR. However, documents such as Form 16, AIS, Form 26AS, bank statements and investment proofs may be required years later to respond to tax notices, verify claims or support future tax calculations.

Here's what every taxpayer should know about preserving income tax documents, whether digital copies are sufficient, and how long these records should be retained for.

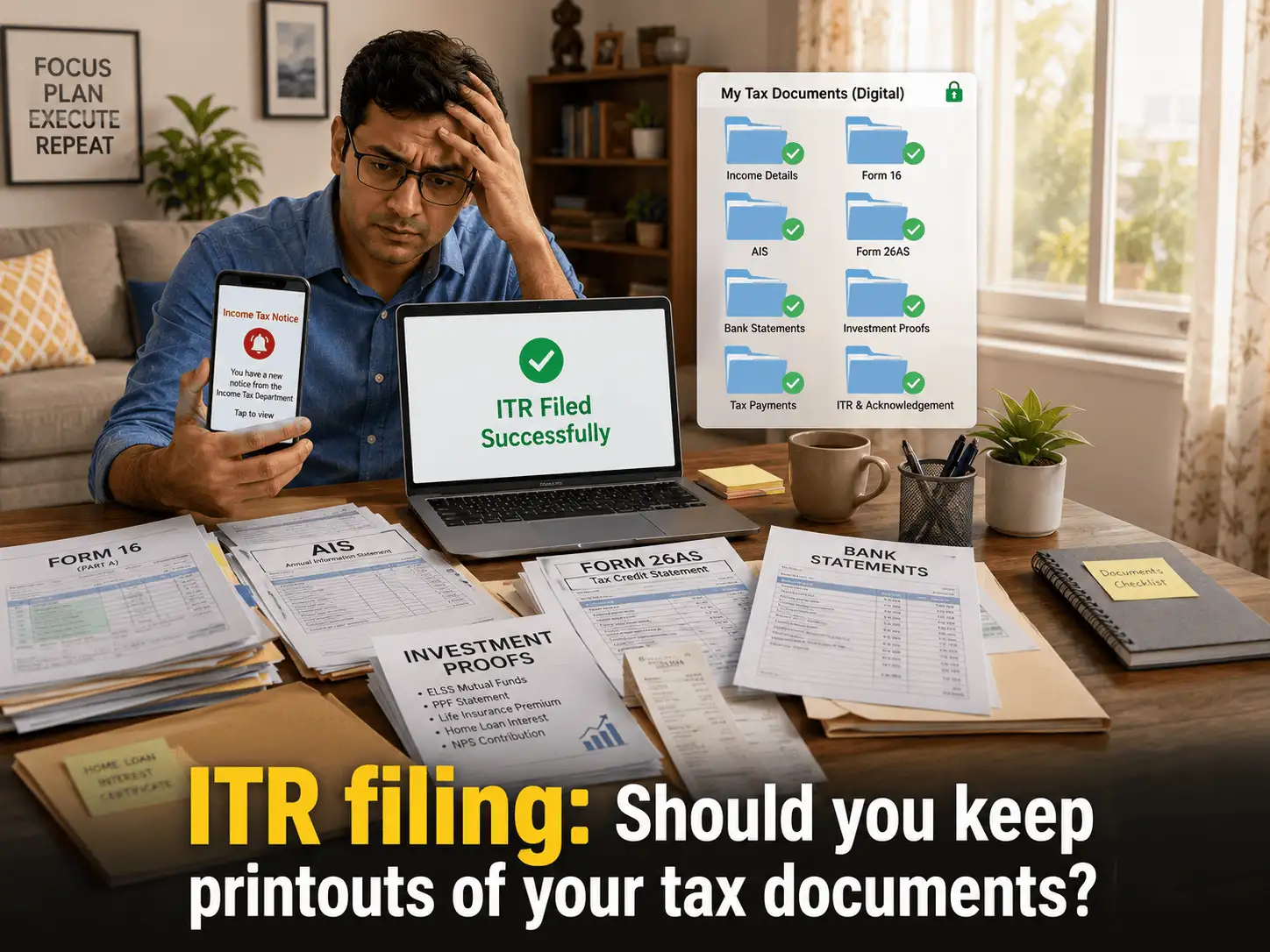

Are digital copies of ITR documents enough, or should you also keep physical copies?

For most taxpayers, maintaining digital copies of income tax documents is sufficient, provided they are clear, complete, readily retrievable and reconcilable.

“Since most tax-related documents, such as Form 16, AIS, Form 26AS, annual information statements, bank statements and investment proofs, are now generated electronically, retaining them in digital format is usually sufficient,” says Neeraj Agarwala, Senior Partner, Nangia & Co LLP.

However, certain documents are best preserved in their original physical form. Taxpayers should not completely discard physical records in cases where the original document itself establishes ownership, cost, or legal rights.

For certain documents such as property purchase deeds, gift deeds, loan agreements, or other records establishing ownership, cost of acquisition or cost of improvement, it is advisable to preserve the original physical copies in addition to scanned versions, Agarwala explains.

A practical approach is to maintain digital copies of all tax documents for easy access while safely storing the original physical copies of important legal and property-related documents. This ensures you are prepared both for tax-related verification and any future legal or ownership requirements.