/Deckers%20Outdoor%20Corp_%20phone%20by-%20Piotr%20Swat%20via%20Shutterstock.jpg)

Valued at a market cap of $15.8 billion, Deckers Outdoor Corporation (DECK) is a Goleta, California-based company that designs, markets, and distributes footwear, apparel, and accessories for casual lifestyle use and high-performance activities.

This footwear & accessories company has underperformed the broader market over the past 52 weeks. Shares of DECK have gained 5% over this time frame, while the broader S&P 500 Index ($SPX) has soared 26.8%. However, on a YTD basis, the stock is up 10.3%, outpacing SPX’s 9.7% rise.

Narrowing the focus, DECK has also lagged the State Street Consumer Discretionary Select Sector SPDR ETF’s (XLY) 12.1% rise over the past 52 weeks. Nonetheless, it has exceeded XLY’s 1.8% YTD gain.

On May 21, shares of DECK rose 4.5% after posting better-than-expected Q4 results. The company’s net sales increased 9.6% year-over-year to $1.1 billion, topping analyst estimates by 3.7%. Meanwhile, its EPS of $0.96 declined 4% from the year-ago quarter but handily surpassed consensus expectations of $0.81.

For the current fiscal year, ending in March 2027, analysts expect DECK’s EPS to grow 5.6% year over year to $7.41. The company’s earnings surprise history is promising. It exceeded the consensus estimates in each of the last four quarters.

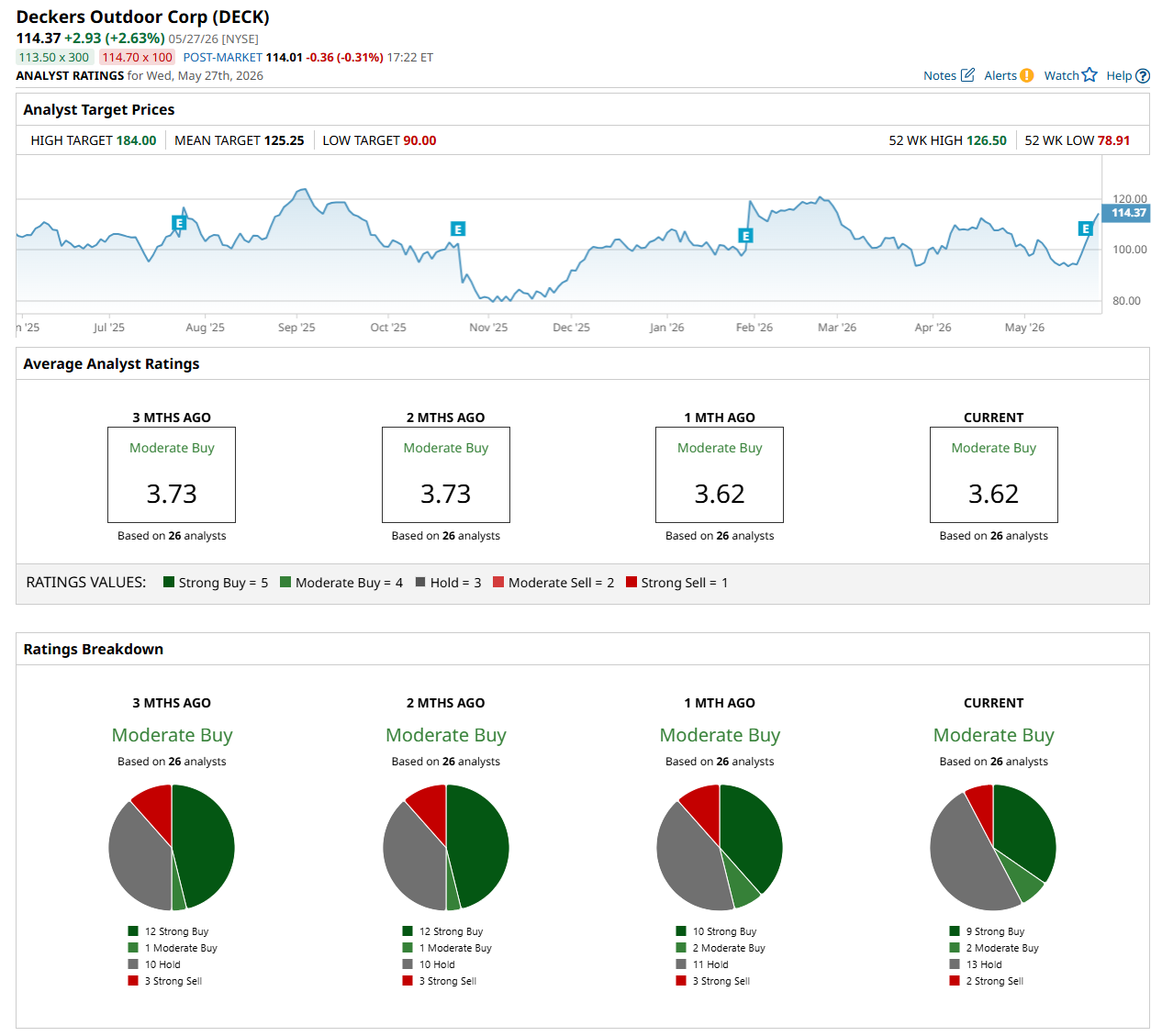

Among the 26 analysts covering the stock, the consensus rating is a "Moderate Buy," which is based on nine “Strong Buy,” two "Moderate Buy,” 13 “Hold,” and two "Strong Sell” ratings.

The configuration is slightly less bullish than a month ago, with 10 analysts suggesting a “Strong Buy” rating.

On May 26, Barclays analyst Adrienne Yih maintained an "Overweight" rating on DECK and lowered its price target to $141, indicating a 23.3% potential upside from the current levels.

The mean price target of $125.25 suggests a 9.5% premium to its current price levels, while its Street-high price target of $184 implies a 60.9% potential upside.