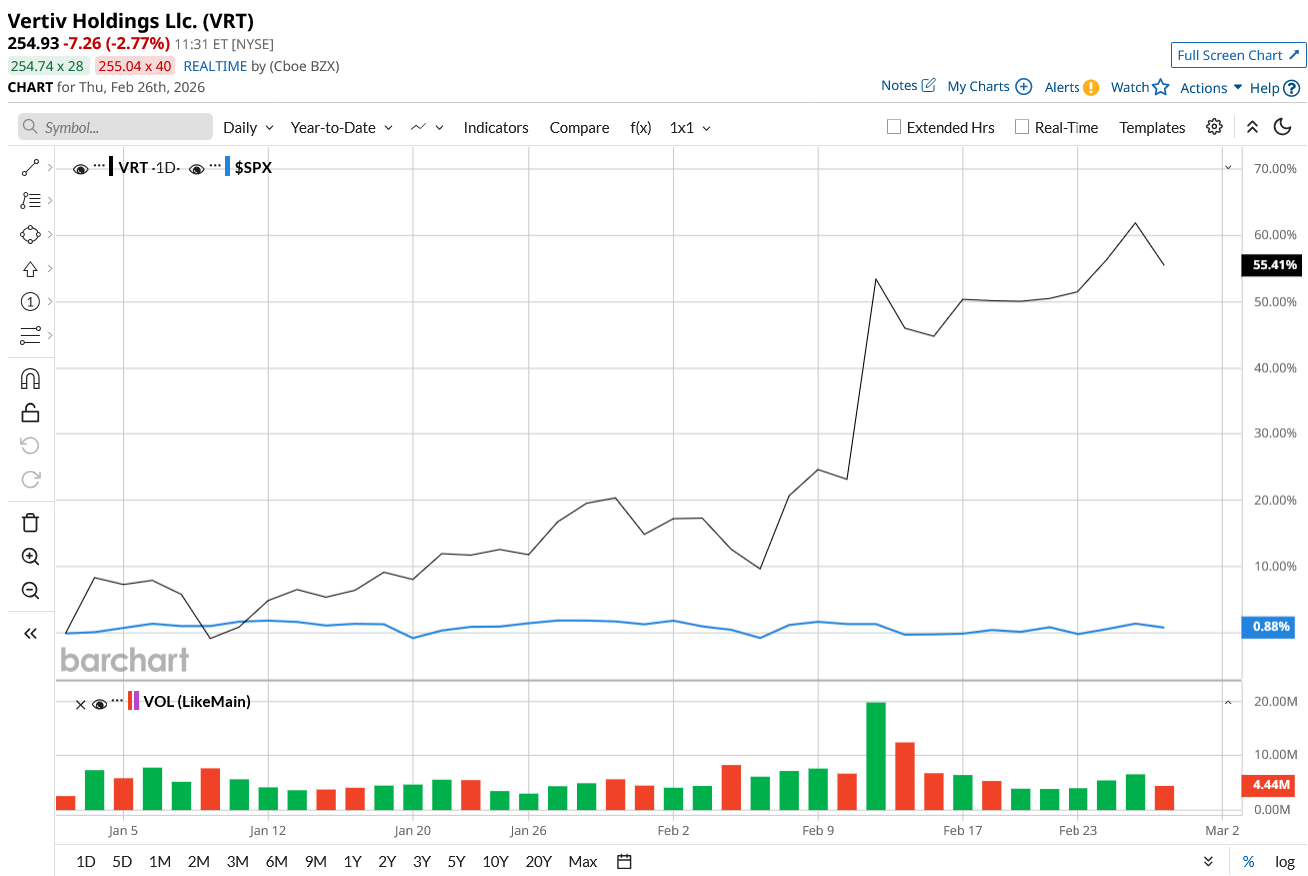

The AI investment cycle has now entered a more selective phase. Investors are no longer chasing the bigger AI names with lofty valuations, especially when earnings growth is struggling to justify these premium valuations. The focus is now shifting to high-quality infrastructure players like Vertiv Holdings (VRT), which are powering the AI revolution behind the scenes. VRT stock has returned 1,502% over the last three years and is up 52% so far this year, while the Magnificent Seven have slumped.

Vertiv may be a tempting growth opportunity for investors looking for smarter AI bets under $300.

Explosive Order Growth Signals Strong Visibility

Valued at $100.3 billion, Vertiv provides critical infrastructure such as power systems, thermal management solutions, integrated prefabricated infrastructure, and lifecycle services to enable data centers to operate securely and efficiently. Vertiv is experiencing explosive order growth, allowing its customers, including Amazon (AMZN), Microsoft (MSFT), and Google (GOOGL), as well as telecom carriers such as AT&T (T) and Verizon Communications (VZ), to build AI-ready capacity more quickly. Organic orders increased 152% year-on-year (YoY) in the fourth quarter. Over the trailing twelve months, organic orders grew 81%, and the company reported a book-to-bill ratio of 2.9 times. Vertiv's backlog now stands at $15 billion, indicating that the company has already received confirmed orders and will fulfill them over the following 12 to 18 months. This implies unrealized revenue in the upcoming quarters. For growth investors, this enormous backlog indicates that demand is not just spiking briefly. In fact, Vertiv's customers have committed to long-term infrastructure investments that will result in predictable earnings.

The company’s geographic diversity reduces reliance on a single market, allowing Vertiv to exploit global AI infrastructure demand. According to the management, while growth in China remains restrained, it is rising in other parts of Asia, particularly India and other emerging markets. For the full year, Vertiv reported net sales of $10.2 billion, an increase of 26%. It’s not just the top line that is strengthening, but pricing power and operating leverage have also boosted adjusted diluted EPS to climb 47% YoY to $4.20.

Beyond hardware, Vertiv’s service portfolio acts as a source of recurring revenue. As AI data centers grow more complex, fluid management, thermal balancing, and reliability optimization become increasingly critical. The company generated $1.9 billion in adjusted free cash flow (FCF) for 2025, leaving plenty of room for reinvestment, acquisitions, and shareholder returns.

Vertiv has a debt-to-equity ratio of 0.74, indicating that the firm does not rely heavily on debt to fund its operations. With a strong free cash flow balance and expanding margins, this debt looks manageable rather than risky. Furthermore, Vertiv aims to generate $2.2 billion in adjusted FCF in 2026, despite raising capital expenditures to 3% to 4% of sales to expand capacity and support future growth. This should help manage the debt.

In 2026, management expects 28% organic growth in sales to $13.5 billion. Adjusted EPS is expected to increase by 43% to $6.20 at the midpoint. Analysts expect rapid expansion over the next two years, with earnings increasing by 46% in 2026, followed by another 28.8% in 2027. The AI-driven infrastructure buildout is accelerating, and the industry is still in the early stages of its growth cycle. There could be sustained demand for Vertiv’s power and cooling systems in those facilities.

Currently, Vertiv is trading at a forward price-to-earnings (P/E) multiple of 33x. The premium valuation implies the market already expects strong growth. Long-term investors who believe AI infrastructure spending will remain robust for years may find the current valuation justified by sustained earnings expansion. However, risk-averse investors might want to accumulate shares during market pullbacks.

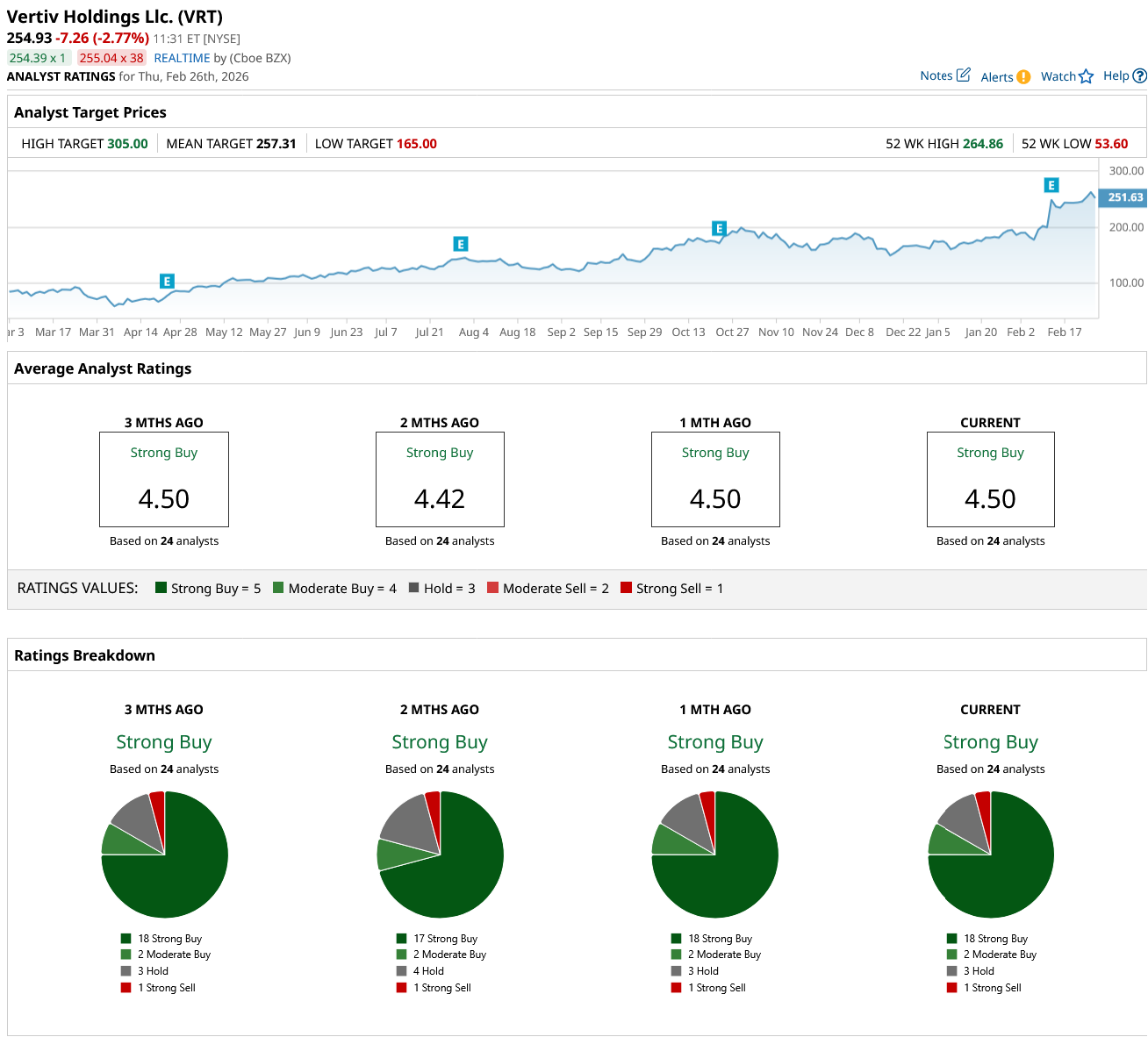

Is VRT Stock a Buy, Hold, or Sell on Wall Street?

On Wall Street, VRT stock holds an overall rating of “Strong Buy.” Of the 24 analysts covering the stock, 18 rate it as a "Strong Buy," two call it a "Moderate Buy," three recommend a “Hold,” and one has a “Strong Sell” rating. VRT stock is trading just below its average target price of $257.31. However, its high price estimate of $305 indicates a possible 20% rally over the next 12 months.