With a market cap of $33.5 billion, Roper Technologies, Inc. (ROP) is a diversified technology company that designs and develops vertical software solutions and technology-enabled products for customers worldwide. The company operates through three segments—Application Software; Network Software; and Technology Enabled Products, offering solutions across industries such as education, healthcare, insurance, transportation, financial services, and foodservice.

Companies valued at $10 billion or more are generally classified as “large-cap” stocks, and Roper Technologies fits this criterion perfectly. Its portfolio includes cloud-based software, AI-enabled analytics, payment processing platforms, precision measurement systems, medical devices, and wireless sensor technologies.

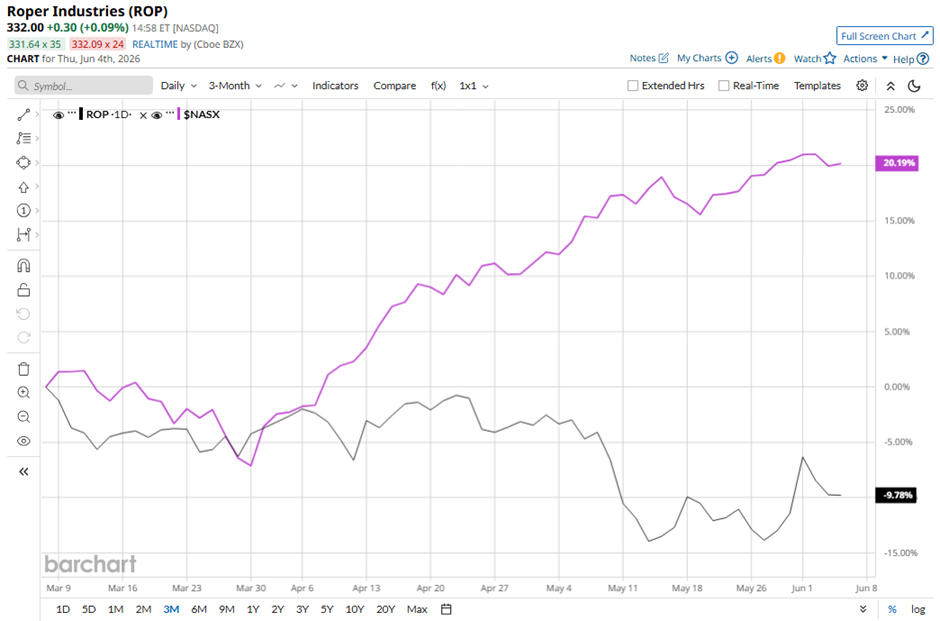

Shares of the Sarasota, Florida-based company have slipped 42.5% from its 52-week high of $576.49. The stock has declined 8.3% over the past three months, lagging behind the Nasdaq Composite’s ($NASX) 18% gain over the same time frame.

Longer term, ROP stock is down 25.6% on a YTD basis, underperforming NASX’s 15.8% increase. Moreover, shares of the company have decreased 41.7% over the past 52 weeks, compared to NASX’s 38.3% return over the same time frame.

The stock has been trading below its 50-day and 200-day moving averages since last year.

Roper Technologies reported strong Q1 2026 results on April 23, including 11% revenue growth to $2.10 billion, 6% organic revenue growth, and 11% free cash flow growth to $562 million. The company also delivered adjusted DEPS of $5.16, up 8%, and net earnings of $509 million, up 54% year-over-year. In addition, Roper raised its full-year 2026 adjusted DEPS guidance to $21.80 - $22.05 from $21.30 - $21.55. However, the stock fell marginally on that day.

In contrast, rival Shopify Inc. (SHOP) has lagged behind ROP stock on a YTD basis, with Shopify shares dipping 27.4%. However, SHOP stock has gained 12.9% over the past 52 weeks, outpacing ROP stock.

Despite Roper Technologies’ weak performance, analysts remain moderately optimistic about its prospects. The stock has a consensus rating of “Moderate Buy” from 18 analysts in coverage, and the mean price target of $450.77 is a premium of nearly 36% to current levels