With a market cap of $12.9 billion, McCormick & Company, Incorporated (MKC) is a global manufacturer and marketer of herbs, spices, seasonings, condiments, and flavor products serving both consumers and the food industry. The company operates through two segments: Consumer, which sells branded spices, sauces, and packaged foods through retail and e-commerce channels worldwide, and Flavor Solutions, which provides customized flavor systems to food manufacturers and foodservice clients.

Companies valued at $10 billion or more are generally considered “large-cap” stocks, and McCormick fits this criterion perfectly. McCormick has built a diverse portfolio of well-known brands across the Americas, Europe, and Asia-Pacific regions.

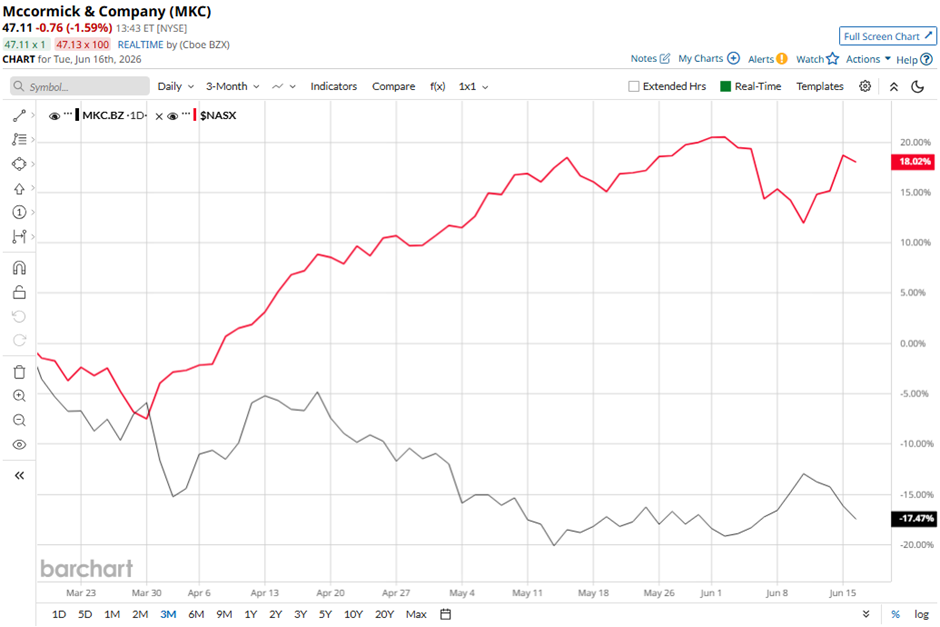

Shares of the Hunt Valley, Maryland-based company have fallen 39.6% from its 52-week high of $78.16. MKC stock has declined 18.2% over the past three months, underperforming the broader Nasdaq Composite’s ($NASX) 18.6% gain over the same time frame.

MKC stock is down 30.7% on a YTD basis, lagging behind NASX's 14.2% increase. Longer term, shares of Cholula sauce maker have decreased 36.1% over the past 52 weeks, compared to NASX’s 34.7% return over the same time frame.

Despite a few fluctuations, the stock has been trading below its 50-day and 200-day moving averages since last year.

McCormick delivered Q1 2026 results on Mar. 31, with adjusted EPS of $0.66 beating the consensus estimate and improving from $0.60 a year earlier. Revenue increased 16.7% year-over-year to $1.87 billion, supported by the acquisition of McCormick de Mexico and 1.2% organic sales growth, while consumer segment sales surged 30.4% in the Americas and 15.5% in the EMEA region. However, the stock tumbled 6.1% on that day.

In comparison, rival The Kraft Heinz Company (KHC) has shown a less pronounced decline than MKC stock. Shares of Kraft Heinz have dipped 8.3% over the past 52 weeks and 2.5% on a YTD basis.

Despite McCormick’s weak performance, analysts remain moderately optimistic about its prospects. Among the 13 analysts covering the stock, there is a consensus rating of “Moderate Buy,” and the mean price target of $63.36 suggests a premium of 34.4% to its current levels.