/Edwards%20Lifesciences%20Corp%20logo%20on%20phone-%20by%20IgorGolovniov%20via%20Shutterstock.jpg)

Valued at a market cap of $47.4 billion, Edwards Lifesciences Corporation (EW) is an Irvine, California-based company that provides products and technologies to treat advanced cardiovascular diseases.

Companies valued at $10 billion or more are typically classified as “large-cap stocks,” and EW fits the label perfectly, with its market cap exceeding this threshold, underscoring its size, influence, and dominance within the medical devices industry. The company recently divested its critical care unit, allowing it to sharpen its focus on high-growth areas like asymptomatic aortic stenosis and structural heart failure.

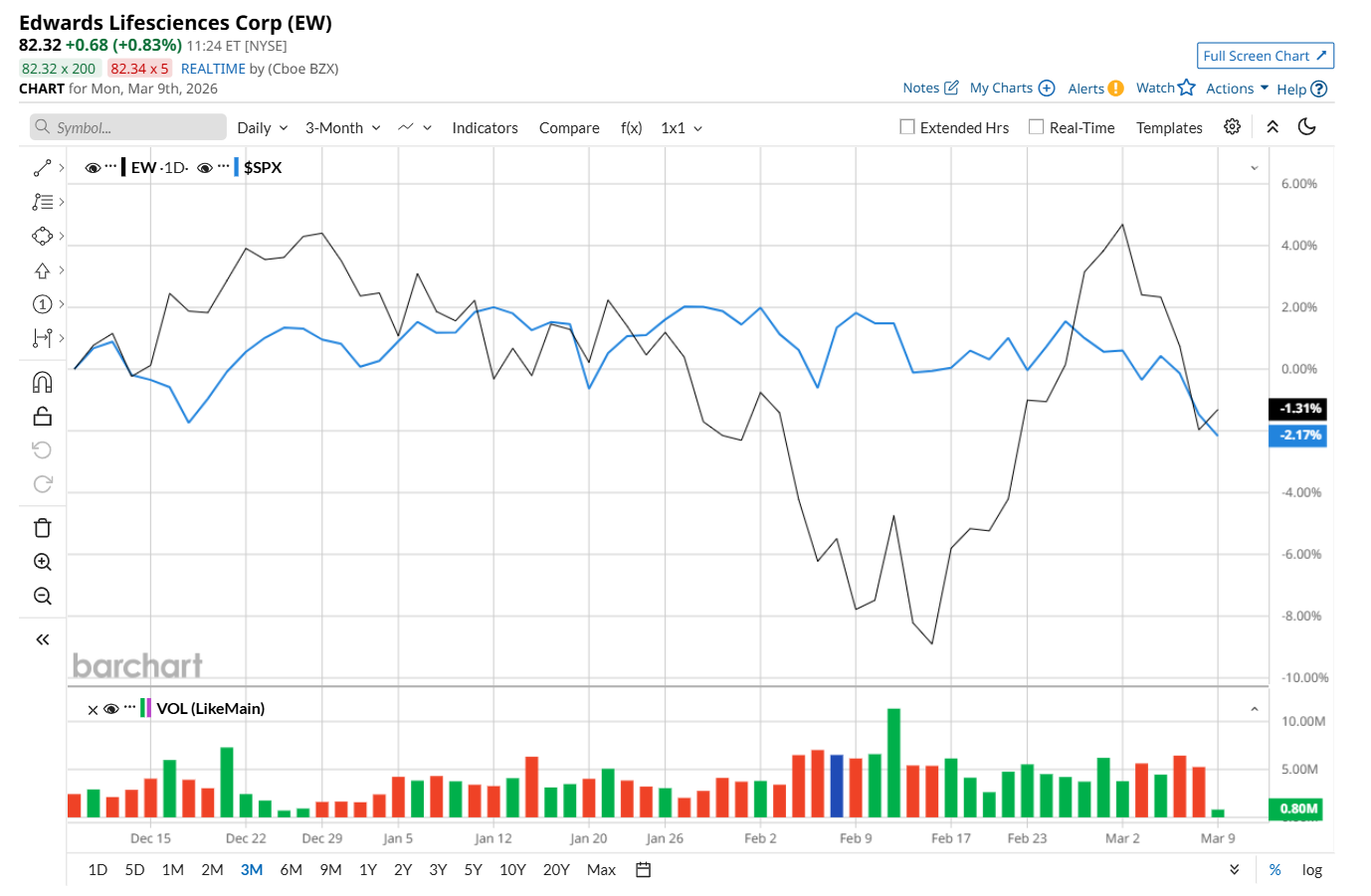

This healthcare company has dipped 6.6% from its 52-week high of $87.89, reached on Dec. 5, 2025. Shares of EW have declined 1.8% over the past three months, outperforming the S&P 500 Index’s ($SPX) 2.4% drop during the same time frame.

Moreover, in the longer term, EW has soared 16.3% over the past 52 weeks, outpacing SPX’s 15.7% uptick over the same time frame. However, on a YTD basis, shares of EW are down 4.1%, lagging SPX’s 2.5% loss.

To confirm its recent bearish trend, EW has been trading below its 50-day moving average since early March. However, it has remained above its 200-day moving average since mid-February.

On Feb. 10, EW delivered its Q4 results, and its shares surged 3% in the following trading session. The company’s net sales increased 13.3% year-over-year to $1.6 billion, while its adjusted EPS declined 1.7% from the year-ago quarter to $0.58. The company is advancing next-generation technologies such as the SAPIEN M3, the first transseptal mitral replacement option, while targeting $2 billion in Transcatheter Mitral and Tricuspid Therapies (TMTT) sales by 2030.

EW has outperformed its rival, Medtronic plc (MDT), which declined 4.2% over the past 52 weeks and 5.7% on a YTD basis.

Given EW’s recent outperformance, analysts remain moderately optimistic about its prospects. The stock has a consensus rating of "Moderate Buy” from the 31 analysts covering it, and the mean price target of $96.07 suggests a 15.9% premium to its current price levels.