Valued at a market cap of $10.1 billion, Camden Property Trust (CPT) is a real estate company that owns, manages, develops, redevelops, acquires, and constructs multifamily apartment communities. The Houston, Texas-based company has a geographically diverse portfolio concentrated in high-growth markets within the Sunbelt and coastal regions.

Companies worth $10 billion or more are typically classified as “large-cap stocks,” and CPT fits the label perfectly, with its market cap exceeding this threshold, underscoring its size, influence, and dominance within the REIT - residential industry. CPT’s business model focuses on providing a range of living options to diverse tenant bases while leveraging an integrated operating platform to drive property-level performance.

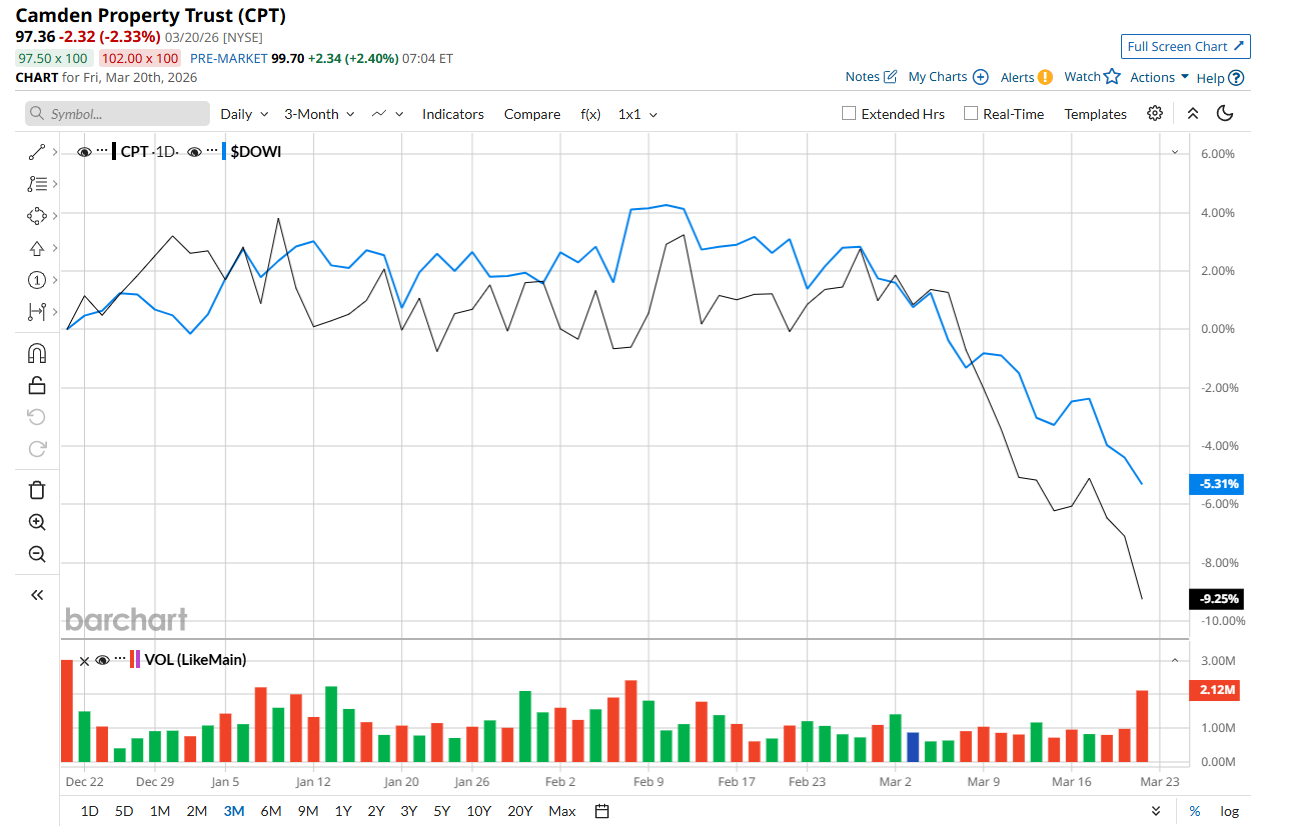

This residential REIT has dipped 21.7% from its 52-week high of $124.32, reached on Mar. 31, 2025. Shares of CPT have declined 9.3% over the past three months, underperforming the Dow Jones Industrial Average’s ($DOWI) 5.3% drop during the same time frame.

Moreover, on a YTD basis, shares of CPT are down 11.6%, compared to DOWI’s 5.2% loss. In the longer term, CPT has fallen 18.9% over the past 52 weeks, considerably lagging DOWI’s 8.6% uptick over the same time frame.

To confirm its bearish trend, CPT has been trading below its 200-day moving average since mid-May 2025, with slight fluctuations, and has remained below its 50-day moving average since early March.

On Feb. 5, shares of CPT plunged 2% after reporting mixed Q4 results. The company’s FFO of $1.76 per share topped Wall Street expectations of $1.73 per share. However, its revenue of $390.8 million missed Wall Street forecasts of $394.6 million. CPT expects full-year FFO in the range of $6.60 to $6.90 per share.

CPT has trailed its rival, Equity Residential (EQR), which dropped 16.5% over the past 52 weeks and 7.6% on a YTD basis.

Despite CPT’s recent underperformance, analysts remain moderately optimistic about its prospects. The stock has a consensus rating of "Moderate Buy” from the 25 analysts covering it, and the mean price target of $115.20 suggests a 17.2% premium to its current price levels.