If all goes according to OpenAI’s financial plans, Microsoft will close a $10 billion investment deal into the artificial intelligence startup before the end of this month, as Jeremy Kahn and I reported yesterday and according to documents seen by Fortune.

That would be an enormous investment in a market environment where founders are struggling to get prospective investors to even pick up the phone—and for a company that isn’t profitable and likely won’t be for some time.

Microsoft’s bet on OpenAI appears to be even bigger than was previously known. The documents suggest that, prior to this deal, Microsoft had already poured $3 billion into the company—$2 billion more than has been publicly reported. If the current deal is completed at the figures being discussed, the cap table in the documents states that Microsoft will have contributed a total of $13 billion in capital to OpenAI, underscoring how important it believes the technology behind ChatGPT and DALL-E 2 is to its future.

Documents related to the looming investment paint a highly unusual deal structure that appears to be tilted in Microsoft’s favor. But, owing to OpenAI’s hybrid structure—with a non-profit lab and a capped-profit business arm—and its extensive commercial partnerships with Microsoft, there are countless variables that could affect how things ultimately play out and pay out. Here are a few key takeaways based on our analysis of the documents.

Venture capitalists are investing in OpenAI through a tender offer of employee shares, happening in parallel to Microsoft’s potential investment, as we previously reported. All investors—including Microsoft—have caps on their potential returns. That isn’t to say the potential returns are small: Documents show that should OpenAI’s technology become extraordinarily successful and profitable, Microsoft would be able to make as much as $92 billion from its collective investment, and venture capitalists that participate in the tender offer would be able to garner up to $150 billion. (An OpenAI spokeswoman declined to comment for this story, and a Microsoft spokesman didn’t respond to a request for comment.)

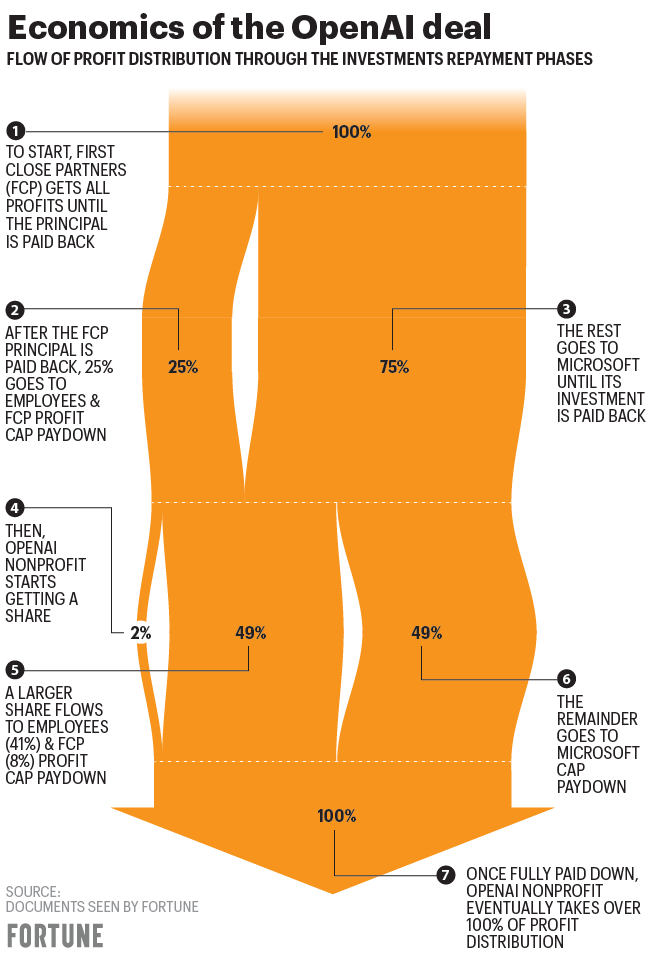

Microsoft will receive preferential treatment when it comes to OpenAI profits. The documents lay out how investors will be reimbursed once OpenAI starts posting a profit. “First close partners” will be reimbursed their principal first (it’s unclear whether “first close partners” refers to OpenAI’s early investors, Khosla Ventures and Reid Hoffman’s foundation, or other subsequent investors in the company). Once that has happened, 75% of OpenAI’s profits will flow directly to Microsoft until the sum that Microsoft invested in OpenAI is reached. Here is a graphical representation of how the economics are structured:

While the terms look like a win-win for Microsoft, it could end up being quite a while before Microsoft, or any of the other investors, see a meaningful return on that investment. Documents show that, as of the end of last year, OpenAI was projecting a loss of more than $508 million for 2022. The company has projected $1 billion in revenue in 2024, as was first reported by Reuters, but it’s unclear what it expects its costs to be in the years ahead. According to the documents, OpenAI expected that its costs in 2022 would total somewhere around $544.5 million.

Will OpenAI need to increase its spending in order to achieve its revenue target in 2024? Or maybe the deal with Microsoft will allow it to stabilize its spending by taking advantage of Microsoft resources, such as cloud computing infrastructure and salespeople? The answers to those questions will help determine when OpenAI might swing to a profit, and consequently when Microsoft would begin to recoup its investment. As for venture investors, an active secondary market for OpenAI shares could help offer liquidity and returns more quickly than OpenAI’s planned profit structure allows.

Of course, an investment in OpenAI is not really a play for short-term profits. A bet on OpenAI is a bet that its generative A.I. technology could override the way everyday people access the internet (Google’s management team is reportedly worried about this possibility); it’s a bet that the OpenAI technology—more so than any generative A.I. technology that may come out of Google, Amazon, or Oracle—could power a universe of high-performing digital assistants that are more effective than humans; and it’s a bet that, just maybe, OpenAI becomes the first company to create computers that can think and learn, which could “be the most important technological development in human history,” according to OpenAI CEO Sam Altman.

David Beisel, co-founder and partner at VC firm NextView Ventures (which is not involved in the OpenAI tender offer), says that OpenAI is a way for venture firms to get in early to “the next potential platform shift.”

“There’s a desire to not just be a part of this company specifically, but the beginning of this broader platform shift,” Beisel says. “When you’re part of it early, and when you’re part of the early successes, the success compounds.”

See you tomorrow,

Jessica Mathews

Twitter: @jessicakmathews

Email: jessica.mathews@fortune.com

Submit a deal for the Term Sheet newsletter here.

Jeremy Kahn contributed to the reporting of this essay, Nicolas Rapp designed the chart, and Jackson Fordyce curated the deals section of today’s newsletter.