/Nasdaq%20Inc%20NY%20building-by%20hapabapa%20via%20iStock.jpg)

The worst of the war-related market turmoil may be over. Setting a buy-in target for Nasdaq, Inc. (NDAQ) stock may be worthwhile. One play is to short out-of-the-money (OTM) NDAQ puts for one-month expiry. Another is to buy in-the-money NDAQ calls for longer periods.

Today it's trading at $88.17, up from a Feb. 12 trough of $79.01, well before the recent drop from the Iran war. But it could have much more to go. I discussed this in a Feb. 10 Barchart article.

The article discussed price targets for NDAQ stock and a short-put play (“Nasdaq, Inc. Stock Is Off Its Highs, Despite Strong Results - Short Put Plays Work Here”).

So, how has this worked out? And, what NDAQ play is best now?

Higher Price Targets (PTs)

I wrote that NDAQ was worth $95.95 per share, based on its strong free cash flow (FCF) and FCF margins. That is 8.8% higher than today's price.

Moreover, other analysts had higher price targets (PTs). For example, Yahoo! Finance reports 17 analysts have an average PT of $108.53. In fact, Barchart's mean analyst survey has a $111.88 PT.

These PTs are +23% and 27% higher than today's price. Even AnaChart's survey, which covers recent analyst write-ups, shows higher prices. It shows a $98.97 average PT from 13 analysts, or +12% upside potential.

That shows it makes sense to take advantage of this low NDAQ price. One way to do this is to sell short out-of-the-money (OTM) puts to set a lower potential buy-in point. That way, an investor can get paid while waiting for this lower buy-in.

Shorting OTM NDAQ Puts

A month ago, I discussed shorting the $80.00 strike price put option that expires on March 20. At the time, the premium received was $1.60, for a 2.0% yield (i.e., $1.60/$80.00) over the next 38 days.

Today, that $80 put strike price premium is down to just 43 cents at the midpoint. That means much of the short-put play income has already been earned. It will expire worthless if NDAQ stays over $80 by March 20.

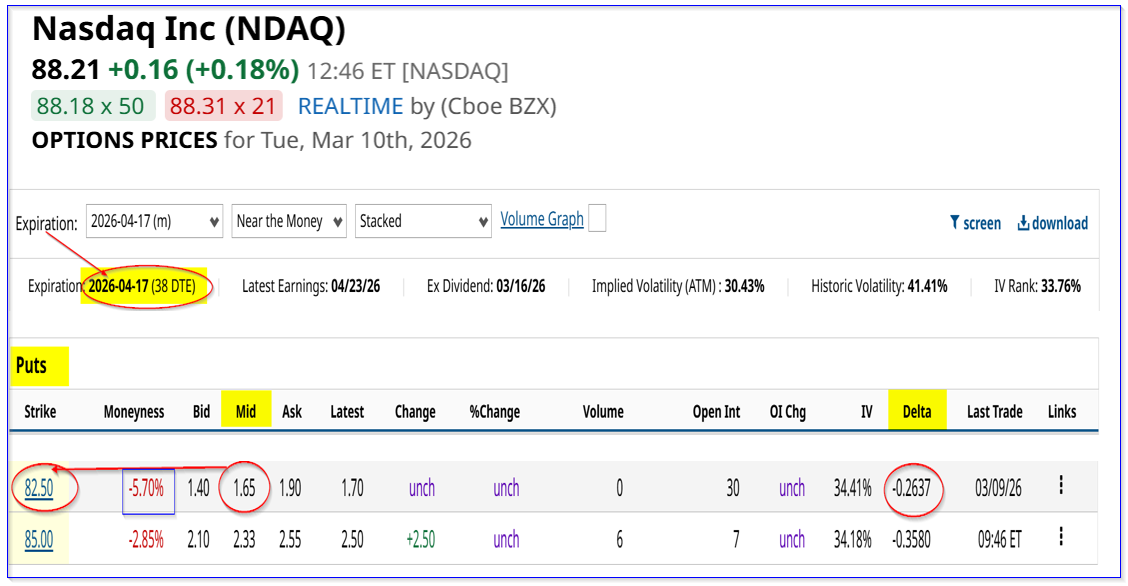

It makes sense to roll this play over (i.e., “Buy to Close”) and do a new short-put play. For example, the April 17, 2026, expiry period shows that the $82.50 strike price put contract has a midpoint premium of $1.65.

This gives a short-seller of this put contract a one-month yield of 2.0% (i.e., $1.65/$82.50 = 0.02), just like last month's $80.00 short-put play.

And this strike price is still -6.47% lowqr than today's price. Moreover, it offers a lower potential breakeven point, if NDAQ falls to $82.50 by April 10:

$82.50 - $1.65 = $80.85 B/E

That's -8.3% lower than today's price. So, it provides a great potential buy-in point for value investors.

However, what if NDAQ rises to our lower PT? Shorting puts doesn't provide any upside. One way around this is to use short-put play income over the next 6 months to buy in-the-money (ITM) calls.

Buying ITM NDAQ Calls

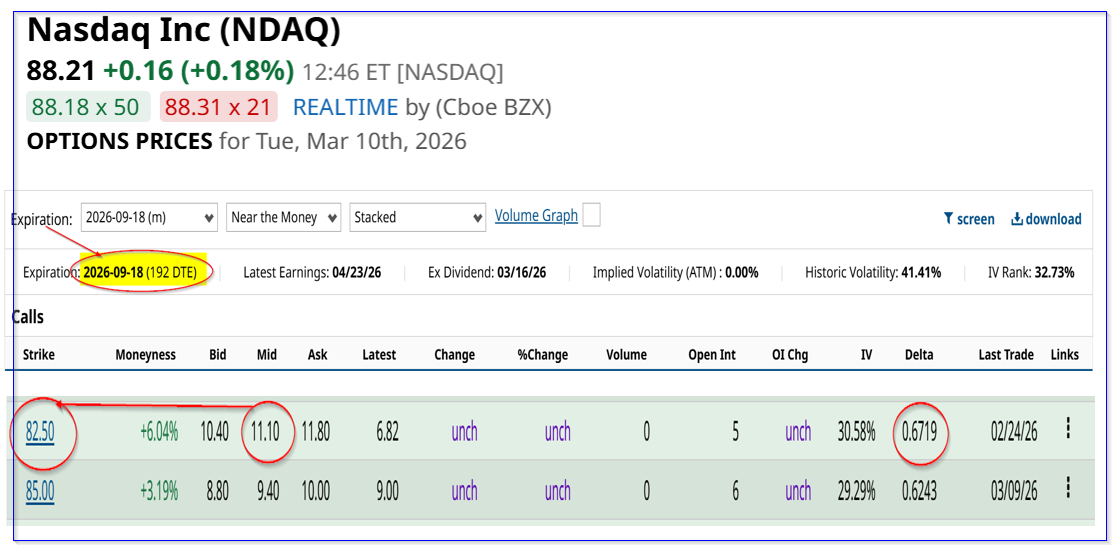

For example, look at the Sept. 18, 2026, expiry period, over 6 months or 192 days to expiry (DTE). It shows that the $82.50 call option has an attractive midpoint premium cost of $11.10.

That means that an investor who continues to short OTM puts each month for six months could potentially pay for most of this call option:

$1.65 x 6 = $9.90 put income

$11.10 - $9.90 = $1.20 net cost

That implies that an investor's cost to buy 100 NDAQ shares (assuming the call option is exercised) would be just $83.70 (i.e., $82.50 +$1.20).

Potential Returns

Here is what that could help an investor. Let's compare a 100 share purchase today vs. this mixed 6-month OTM short-put/ITM call purchase play.

If NDAQ rises to $100 by Sept. 18, the long-share buyer would make the following return:

Cost: 100 shs x $88.21 = $8,821

Return: $100 x 100 shs = $10,000

$10,000 - $8,821 = $1,179

ROI: $1,179 /$8,821 = +13.37%

However, consider the alternative:

Cost: $8,370 (mixed cost of short-put play and call option buy-in - $83.70 x 100)

Return: $10,000 - $8,370 = $1,629

ROI: $1,629 / $8,250 = +19.75%

The ROI is significantly higher over the six month period.

This is due to the lower cost of shorting $82.50 put contracts each month and eventually buying in at this lower in-the-money (ITM) cost of $82.50.

Moreover, the investor collects income each month, which helps pay for the longer-dated ITM call option. At any point, due to extrinsic value, the investor may be able to sell the call option for a much higher ROI.

The bottom line is that shorting OTM NDAQ puts and buying ITM calls makes sense here.