Interest rates are rising for the fourth time in six months, meaning higher monthly payments for around 2 million homeowners.

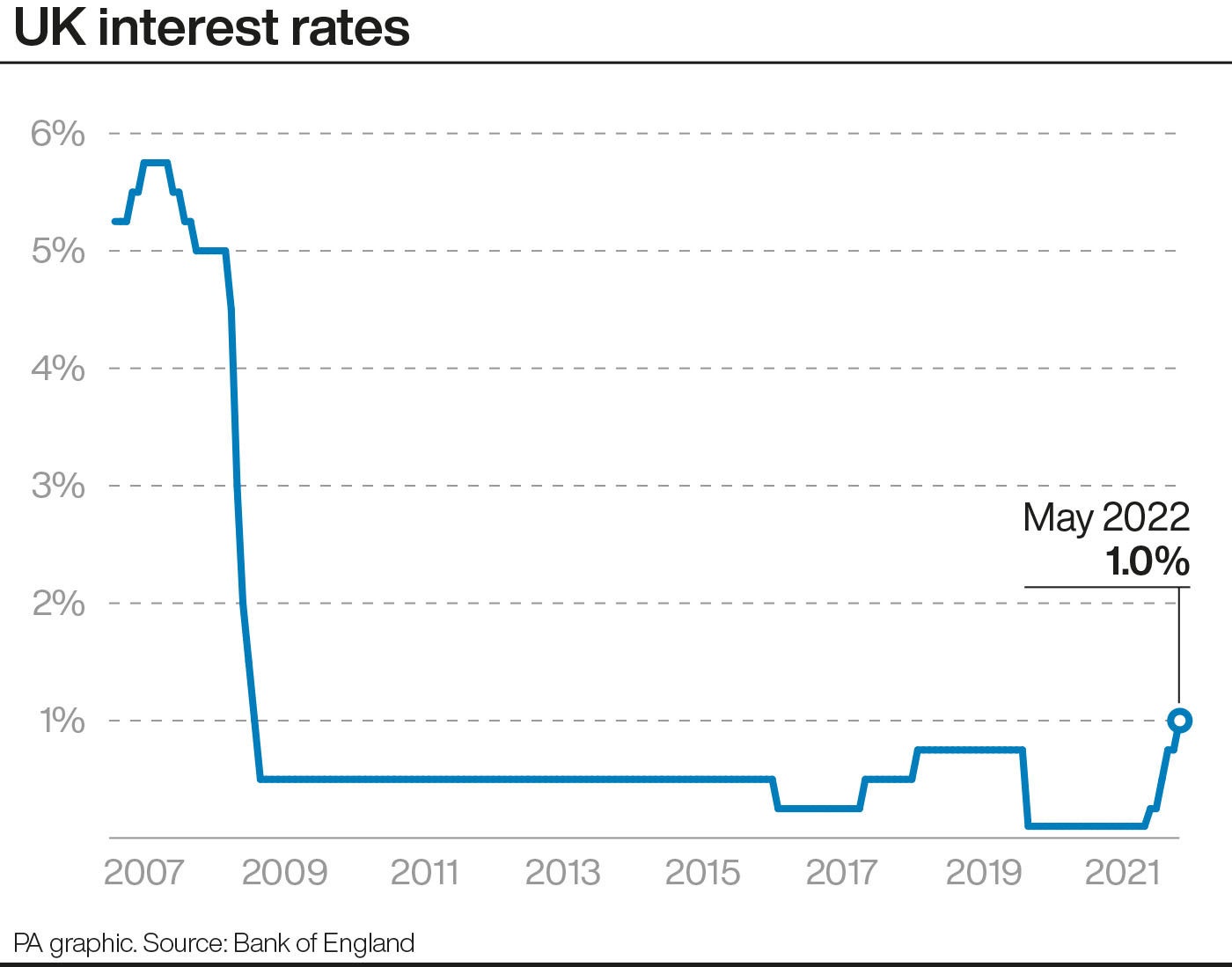

The Bank of England has raised its base rate from 0.75 per cent to 1 per cent – a level not seen since 2009.

It is hoped that the move will help to contain an alarming rise in inflation, but it means that high street lenders will increase the rates they charge on variable-rate mortgages and loans.

Borrowers will therefore face higher costs at a time when energy bills and food prices are going up rapidly. Meanwhile, savers can expect slightly better returns on their money.

So, how will the Bank’s interest-rate hike affect people’s mortgages, savings and investments?

How will homeowners be affected?

Of the almost 9 million residential mortgages outstanding in the UK, fewer than a quarter will be affected immediately by the latest rise in interest rates.

A little less than one in 10 mortgages are trackers, meaning the rate that borrowers pay is directly linked to the Bank of England’s base rate. Around 850,000 homeowners will see the interest rate they pay increase by 0.25 per cent straight away.

A further 1.1 million people are on a standard variable rate (SVR), often because this is the default deal that their lender has put them onto once a fixed-rate deal has expired.

These rates are set by individual lenders and tend to follow closely the Bank of England’s base rate.

Three-quarters of outstanding mortgages are on fixed rates, meaning these homeowners will not feel the immediate impact of a base-rate rise, according to figures from trade association UK Finance.

However, if rates remain higher, these borrowers will find that they have to pay more each month when they renew their mortgage deal.

What will the impact on mortgages look like in cash terms?

The average borrower on a tracker mortgage will pay about £25 extra in interest per month, according to UK Finance. That’s based on an outstanding balance of £121,034.

Someone with a typical SVR balance of £76,499 would pay around £16 more per month, assuming the lender passes on the 0.25 percentage point base-rate rise in full.

What can mortgage holders do about the rises?

Borrowers on variable rates can protect themselves from rising interest rates by locking in a fixed-rate deal. The average two-year fixed rate has increased in recent months to more than 3 per cent, according to moneyfacts.co.uk.

The Bank of England indicated on Thursday that it may increase its base rate further this year, and markets are predicting that further rises are in the pipeline.

Will the rate rise mean better news for cash savers?

Rachel Springall, of moneyfacts.co.uk, said the average easy-access savings account interest rate has crept up by just 0.20 percentage points since November, from 0.19 per cent to 0.39 per cent.

She added: “There is still room for improvement across the sector, but as rates rise, comparing deals and switching is wise. As we have seen before, it can take a few months for customers to see any benefit from a base-rate rise, but there is no guarantee that savings providers will increase their rates.”

Ms Springall said a 0.25 percentage point increase passed on in full would equate to savers receiving £50 more a year in interest, based on a £20,000 investment.

Pensioners could also see their incomes increase. In April 2021, a £100,000 pension pot would get you a single-life level annuity income of £4,882 a year. Now, that figure has increased to almost £5,600.

Is there anything else savers can consider?

Paul Titterton, head of digital at Abrdn, suggests some people may want to consider investing in stocks and shares.

Mr Titterton said: “Anyone in a position to put money aside for their future should consider where they save and their attitude to risk. While cash savings are safe, they are impacted by low interest rates and growing inflation. Stocks and shares and investment Isas carry more risk, but could potentially provide greater returns in the long term.”

What could the implications of rising rates be for investments?

Jason Hollands, managing director of Bestinvest, said: “Rising borrowing costs have implications for the way investors assess businesses, and in this respect, ‘growth’ companies in sectors like technology and communication services are particularly vulnerable.

“That’s because investors assess these companies primarily on the basis of projections of future earnings, rather than their profits today, so when rising borrowing costs and inflation create greater uncertainty about the future value of money, investors revise their view of what such companies should be valued at.

“On the flip side, some businesses are a lot more resilient to the current environment. Banks can actually benefit from rising interest rates, energy prices are a major component of inflation, and some businesses offer hard-to-replicate products and services that customers cannot do without, so are able to pass on cost increases without sacrificing profit margins.

“The UK market has more than its fair share of such businesses, and so the UK stock market has held up relatively well so far this year. In the environment we are in, solid companies with conservatively financed balance sheets that are able to churn out attractive dividends should be on investors’ radars.

“In recent years, these have often been overlooked by investors as boring, but it is time to take another look.”