With the stock market soaring to new all-time highs on what seems like a daily basis, managing your portfolio's risk might not be the first thing on your mind.

If you wait for a downturn, though, it's already too late. You don't want your roof to catch fire before you buy homeowner's insurance.

The best way to manage your portfolio's risk is through proper diversification. And the basic idea is simple enough: Don't put all of your eggs in one basket.

But how much diversification is enough? And how do you know if your portfolio is functionally diversified vs apparently diversified?

Your 401(k) account might be spread across 10 different mutual funds. But if they all own substantially the same stocks, you're not diversified. You have the appearance of diversification without the benefits of diversification.

So, let's talk about the basics of diversification and how to ensure your portfolio actually reaps rewards from doing it the right way.

What is diversification?

The core principle of diversification is that prices of different assets move independently of one another and that holding a broad mix of assets reduces your risk.

For instance, when the stock market declines, bonds may increase in value, or real estate might remain stable.

Diversification also works within an asset class. Large-cap tech stocks such as Apple (AAPL) and Microsoft (MSFT) can both be affected by the general direction of the stock market.

But these are also distinct companies with risks and opportunities specific to their respective businesses. Apple might have a great quarter and see its stock soar at the same time Microsoft has a lousy quarter and sees its stock fall, or vice versa.

Perhaps the most important beneficial impact of diversification is a smoothing effect.

Over time, you get the weighted average return of the individual pieces of your portfolio. But, along the way, you suffer less of the up-and-down volatility.

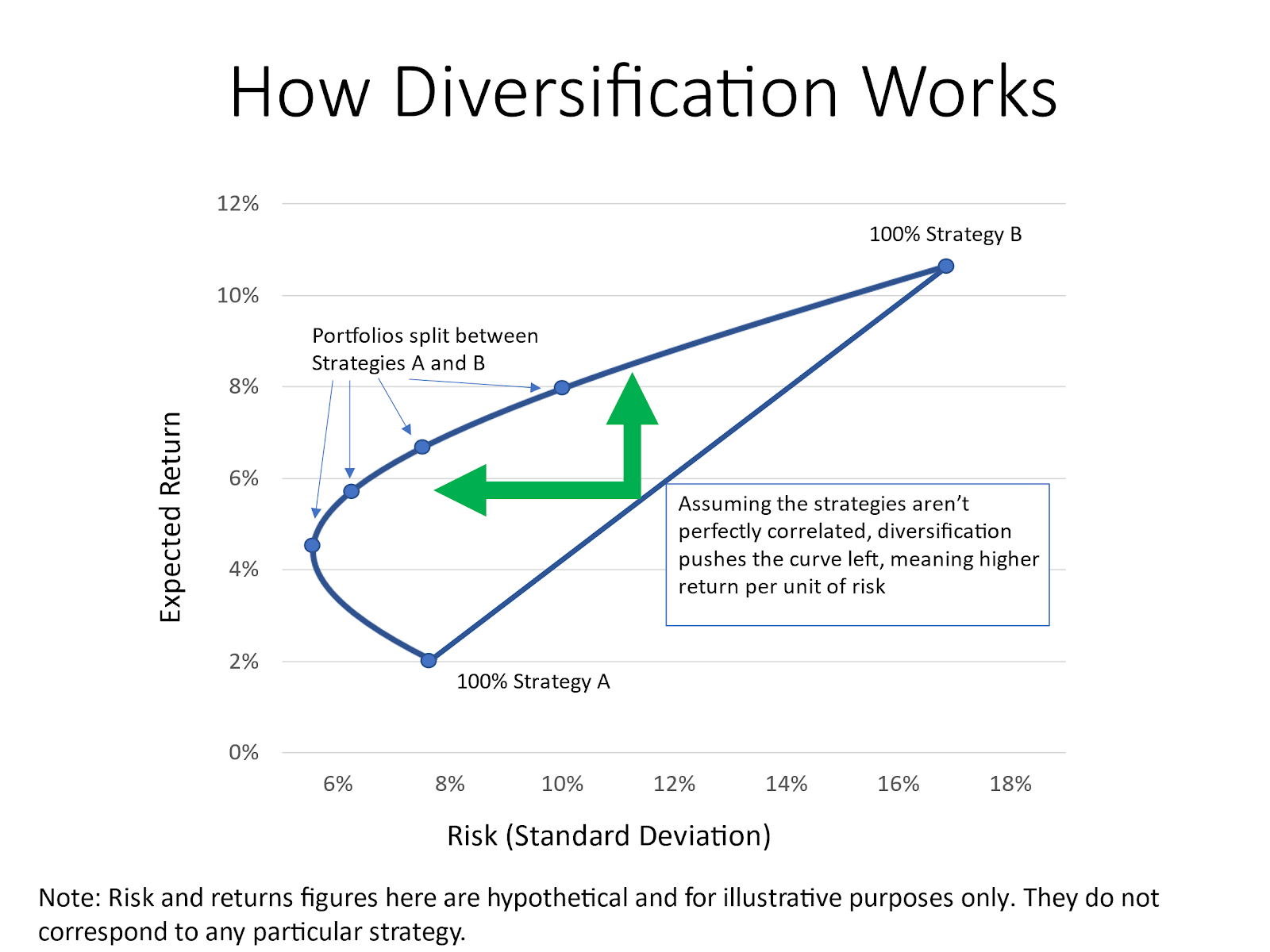

Take a look at the graphic example below. This is for illustrative purposes and does not correspond to any particular strategy.

It shows how diversification increases your return for a given level of risk or lowers your risk for a given level of return.

Strategy A has an expected return of 2% with a risk, or "standard deviation," of 8%. Strategy B has an expected return of 11% with a risk of 16%.

A portfolio split 50-50 between the two will have an expected return of 6.5%, which is the average between 2% and 11%.

But the expected risk won't be the average risk of Strategy A and Strategy B. It will be lower. The straight line gets pushed into a curve.

This is the magic of diversification.

Don't worry if you get lost in the math. The key takeaway is that diversification done right will lower your risk for a given expected return or boost your expected return for a given level of risk.

And the lower the correlation between your assets, the bigger the diversification benefit.

How to check if your portfolio is diversified

So, how do you know if your portfolio is diversified? You can get technical if you're into that sort of thing.

Morningstar, Yahoo Finance, Portfolio Visualizer and a host of other services offer tools that allow you to measure how correlated the assets in your portfolio are and what your portfolio's expected risk and return would be. Your 401(k) provider may offer something similar.

Frankly, folks, you don't need to get all that precise.

In fact, leaning too heavily into the math can give you a false sense of security. Common sense and a couple of basic concepts will likely get you close enough.

One rule of thumb quoted by financial advisers is the "100 minus your age" principle. The idea here is that your allocation to stocks should be roughly equal to 100 minus your age.

If you're 70 years old, you should have about 30% of your money in stocks and the rest in bonds or other safer assets that tend not to move in step with the market.

This is a broad guideline, not an iron-clad law of the universe. Depending on your current wealth, your attitude toward risk and your other sources of income, your ideal number might be higher or lower than that.

You should also diversify within your stock allocation.

As a general rule, you probably don't want more than a couple percent of your portfolio in any single stock. (This rule can bend if you're an aggressive trader, again based on your wealth, your risk tolerance and your objectives.)

An S&P 500 index fund is arguably all the diversification you need, particularly for smaller portfolios. Something like the SPDR S&P 500 ETF Trust (SPY) will give you exposure to a broad swath of America's largest, most dominant companies.

But the S&P 500 isn't the only game in town, and there are stretches of years or even decades at a time when small-cap, mid-cap, real estate and foreign stocks outperform it.

Diversifying with mutual funds or exchange-traded funds that focus on these sectors can potentially reduce your risk and boost your returns over time.

Diversification is a lot like horseshoes and hand grenades: You don't have to hit an exact target.

Close is usually going to be good enough.