I want to share a strategy that can help your children get a huge jump start on their retirement. Many clients I work with wish they’d started saving at a much younger age, and they worry their children may make the same mistakes. So, many of them hope to teach their children how to manage their own money.

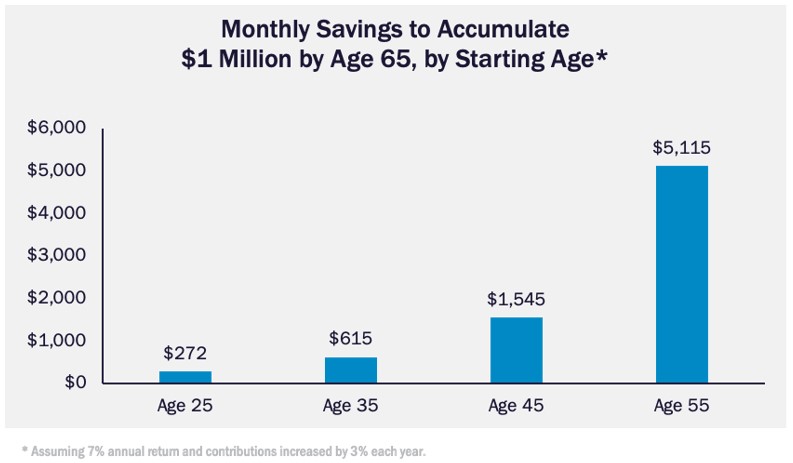

One of the most important lessons to teach is how important it is to save. Most people don’t realize how much they need to save for retirement. For instance, using a common 4% sustainable withdrawal rate in retirement, you’d need to save $1 million by retirement in order to have $40,000 of sustainable annual income in retirement.

That savings goal can feel pretty daunting, especially for younger people. But the biggest advantage young people have when it comes to retirement is that they have a lot of time for their savings to grow. The earlier they start saving and investing, the more wealth they’ll build.

But let’s get real… I’ve yet to meet the teen who is thinking about their retirement. A simple strategy that parents can implement to jump start their children’s retirement savings is to help them fund a Roth IRA.

Say your kid earns $3,000 from a job in 2023. If the income is W-2, they can contribute 100% of their earned income up to $6,500 to a Roth IRA, or $3,000. If income is 1099, the contribution limit is reduced by 7.65% (half of the self-employment tax) or $229.50 and can contribute $2,770.50 to the Roth IRA.

They probably won’t have the cash to make contributions themselves (even if they wanted to), but this is where parents can step in by giving them a tax-free cash gift (up to $17,000 per person for 2023) that can be used to fund the Roth IRA. In most states, if the child is a minor, you’d have to start with a minor Roth IRA where the parent is the custodian of the account, and then you can convert the account to a regular Roth IRA owned by the child once they are legally an adult.

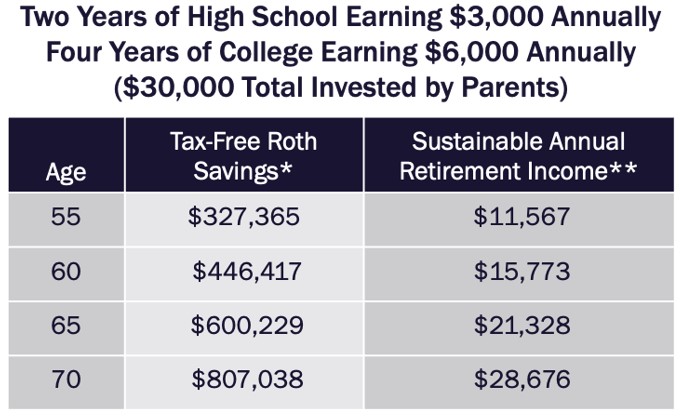

How big an impact can this have on your kids’ lives? Assume they contribute $3,000 a year as a high school junior and senior, and $6,000 a year during all four years of college (so $30,000 in total contributions). If they earn a 6.8% annual return from ages 16 to 40, 6.4% from ages 41 to 60 and 6.1% after age 60 (the expected returns from 80% stock, 70% stock and 60% stock allocations, respectively), they’d have more than $600,000 of tax-free retirement savings by age 65, which could yield more than $21,000 of sustainable tax-free income throughout retirement.

In addition, this creates an opportunity to teach your kids some basic investing concepts, such as what retirement accounts are and the time value of money. Hopefully, they’ll become accustomed to the annual contributions and carry those good habits forward into their adult lives.

That’s a legacy you can be proud of.