If interest rates come down, according to our fixed income investment guru, “the reductions will likely be at the short end of the yield curve with rates holding steady at the longer end.” Or in layman’s terms, if we move to a more typical yield curve, you’ll see rates on long-term bonds (underlying annuity rates) be substantially higher than on short-term securities and CDs. That may also mean that rates on new annuity contracts are holding steady — although maybe not for long.

For our typical investor, Sally, who is 70, her lifetime income from a $500,000 investment sits at about $42,000 per year, or 8.4%, which means nearly double the current short-term rate of, say, 4.25%. But do you give that advantage away in taxes? That answer and more below.

Taxes on immediate annuities vs short-term securities

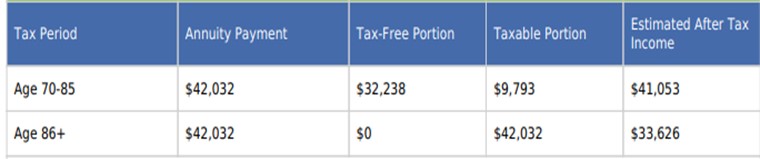

For our investor above, here’s a portion of the information she got on March 24 in her annuity quote.

We learn this from her report:

- Only $9,800, or 23%, of her payment is taxable during an initial exclusion period

- Her initial exclusion period continues to age 85

- Assuming an overall income tax rate of 20%, she receives: 97.5% of her annuity payment after taxes through age 85 and 80.0% of her annuity payment after taxes at ages 86 and over

This means her after-tax yield during the exclusion period is 8.21%. If short-term rates settle at their long-term average of 3.50% and she nets 2.80% after tax, she’s more than tripling her after-tax income — until she’s 85. Of course, the annuity is not preserving principal, and thus the allocation to this annuity should be limited. You can find out your income and tax benefits here.

Where does the tax benefit come from? The general rule to consider is that when purchasing an immediate annuity from personal savings, your already-taxed principal is excluded from tax. Once you recover the principal from your purchase, though, taxes kick in on the full payment. However, later in life when the annuity exclusion disappears, you may have medical or other expenses that will help you offset the higher taxes.

Also consider that women tend to live longer than men, so their annual annuity payments are smaller than those of men, everything else being equal. However, the exclusion formula does not reflect gender so that the tax tables figure both genders will have the same life expectancy, and thus women are advantaged by having a smaller percentage of income taxed (23.0% vs 27.5% for this example).

Tax benefits across your entire plan

We understand that your tax bill is not the sum of taxes on individual sources of income like annuity payments, Social Security payments, dividends, interest, IRA withdrawals, etc., but on your aggregate taxable income less deductions and exclusions. So, we need to dig a little deeper into our investor’s plan for retirement income to view the total tax bill as follows.

She has $2 million in retirement savings, with half in a rollover IRA, and her house is worth $1 million with no mortgage. She can count on $36,000 in Social Security benefits and $26,400 in pension payments each year. Her savings, with 30% in stocks and 70% in taxable bonds, will produce an additional $90,000 of income.

Her current plan would leave her about $20,000 short of her income goal, which is intended to cover all her bills, including premiums for long-term care and health insurance, the cost of renovations to her home and 529 contributions for her grandkids.

To help her figure out how to get that extra $20,000 in income, Sally went to Go2Income. Without taking greater investment risk, a Go2Income plan allocated a portion of her fixed income portfolio to annuities like the above. The plan also incorporated a HomeEquity2Income program for both income and liquidity to address the possibility of long-term care or a health crisis. Bottom line, she found the $20,000 and then some.

But here’s the bonus. While you’d think more income equals more and a higher rate of taxes, her Go2Income plan actually reduces the taxes by $4,500 and lowers the tax rate from over 13% to below 10%. Wow!

What drives Go2Income planning tax outcomes?

Besides considering the usual — inflation, percentage of safe income, legacy objectives, etc. — the Go2Income plan considers the following when it comes to taxes:

Difference between personal and rollover savings. Taxes on the money you save in a 401(k) or rollover account are deferred until they arrive in your bank account as payments. That benefits savings, but you have to account for the taxes upon retirement. Adjustments in other accounts can help keep your tax rate as low as possible, particularly using the exclusion benefit on income annuities above. Or using a QLAC to defer taxes is another tax benefit that is granted annuities. (To learn more about a QLAC, read my article For Longevity Protection, Consider a QLAC.)

Difference between immediate and deferred income annuities. A deferred income annuity defers payments and taxes on that batch of savings into the future. Immediate annuities have the tax benefits above, and using a mix of these annuities within the annuity asset class can contribute to tax reduction.

Tax-free drawdowns from home equity. Accessing the equity in your home can be a source of tax-free income. Using this strategy for a temporary period and then combining with a deferred income annuity can be effective, as you can see in my article How Your Home Can Fill Gaps in Your Retirement Plan.

What to do about taxes in your planning?

A lot of planning systems don’t consider taxes in their allocation.

When you do your planning or review your adviser’s plan for you, look at:

- All income streams. Social Security benefits, annuity payments, IRA distributions, dividends, interest and capital gains

- All accounts that are sources of income

- Taxes in all life stages and objectives — Income, liquidity, and legacy

- Taxes when reallocating from current strategy or rebalancing new plan

- Both the immediate and long-term impact of plan allocations

The federal government creates ways to save on tax payments for several reasons, including to promote retirement savings and to make retirement more comfortable. It makes sense to take advantage. Visit Go2Income and build your own retirement income plan that minimizes your taxes.