/Danaher%20Corp_%20logo%20on%20phone-by%20Piotr%20Swat%20via%20Shutterstock.jpg)

Headquartered in Washington, D.C., Danaher Corporation (DHR) is a global science and technology powerhouse focused on biotechnology, life sciences, and diagnostics. With a market capitalization of nearly $149 billion, it sits in the “large-cap” territory, a space reserved for companies valued above $10 billion.

This scale gives Danaher the muscle to build bioprocessing systems, precision laboratory instruments, genomic technologies, and clinical diagnostic platforms that anchor drug development, scientific research, and patient care across hospitals, laboratories, and biopharma facilities worldwide.

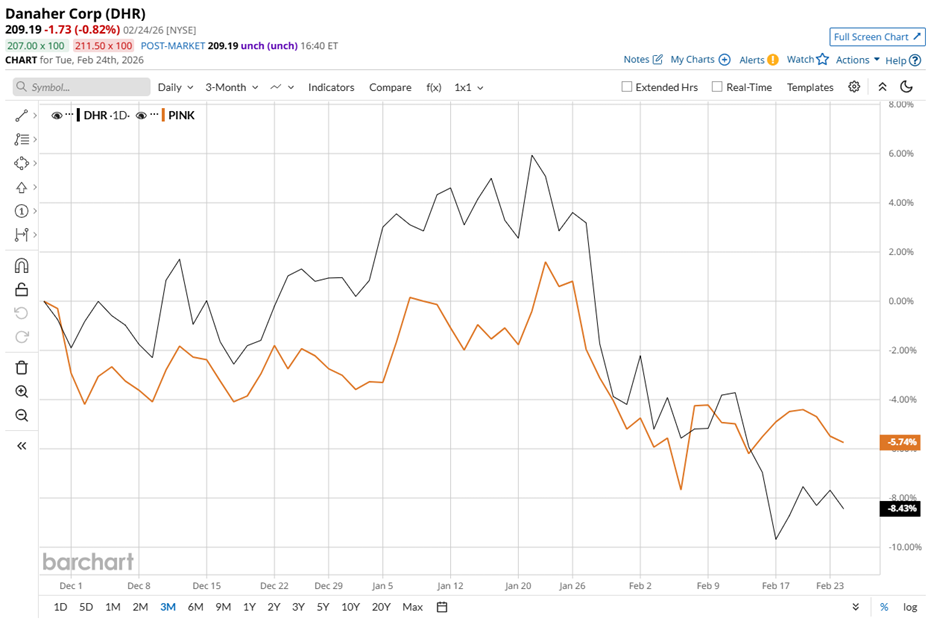

The stock, however, tells a more tempered story. Danaher’s shares are trading 13.8% below their January high of $242.80 and have slipped 7.8% over the past three months. Over the same stretch, the Simplify Health Care ETF (PINK) declined 3.9%, underscoring Danaher’s relative underperformance in the near term.

Over the last 52 weeks, the shares have edged marginally lower, trailing PINK’s 19.1% gain. Year-to-date (YTD), DHR stock is down 8.6%, compared with a 2.2% decline for the broader benchmark.

Technically, the tone has softened. Since mid-October 2025, DHR stock was trading comfortably above both its 50-day and 200-day moving averages, signaling steady momentum. However, the posture shifted in late January, and now the stock has been trading below its 50-day moving average of $226.26 and its 200-day moving average of $209.73.

The catalyst may well lie in strategic expansion. On Feb. 17, Danaher’s shares fell 2.9% after the company agreed to acquire Masimo Corporation (MASI) for $180 per share in cash, implying an enterprise value of roughly $9.9 billion. Masimo brings pulse oximetry and patient monitoring solutions deeply embedded in acute care settings.

Masimo embeds its pulse oximetry and patient monitoring platforms across acute care settings, generating durable clinical demand and high-margin recurring revenue.

Investors initially pulled back shares out of caution toward large healthcare deals, but the roughly 15x projected 2027 EBITDA multiple with synergies and 18x without underscores disciplined pricing and strengthens Danaher’s long-term position in patient monitoring and specialty diagnostics.

Against peers, the comparison adds perspective. Danaher’s rival Agilent Technologies, Inc. (A) has delivered an 8% gain over the past 52 weeks and is down 8.6% YTD. DHR stock’s relative lag highlights the market’s current preference elsewhere within the tools and diagnostics space.

Yet analysts remain firmly in place, holding their ground with steady conviction despite the recent pullback. Among 23 analysts covering the stock, the consensus rating stands at “Strong Buy.”

Moreover, the average price target of $264.05 represents 26.2% upside from current levels, implying that the Street expects the recent weakness to give way to renewed momentum as operational execution regains center stage.