How does it feel to know that some people will pay less for Medicare coverage than you do, but you will all get the same benefits?

It can be tough to understand, especially when you have been a diligent saver over the years, have worked hard to accumulate what you have and have really embraced the “millionaire next door” concept. Meanwhile, another person, possibly paying less for the same coverage, did not work as hard as you over the years and was not as much of a diligent saver as you.

Unfortunately, paying a higher price tag doesn't get you better coverage when it comes to IRMAA and Medicare premiums.

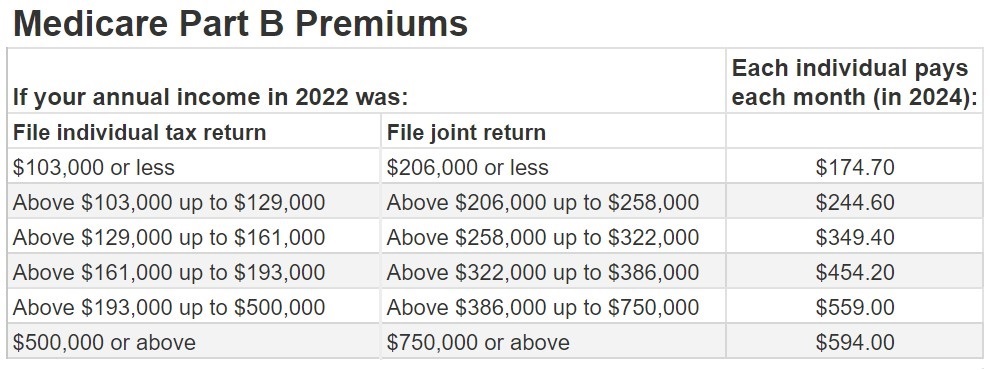

Let's first explain what IRMAA is and how this all works together. IRMAA stands for “income-related monthly adjustment amount.” It’s an add-on cost that some Medicare Part B and Part D beneficiaries may be required to pay. The chart below outlines what 2024 Medicare Part B premiums will cost based on income. You can see that the more you earn, the more your Medicare coverage costs you.

Remember that this chart goes back two years, so the income you have when you are 63 will determine your costs when you turn 65. So, for example, let's say that you sold a business at the age of 63. Then, at age 65, you would have to pay the consequence of that, so that's why it's important to be aware of your income starting as soon as 63 — even though you're not on Medicare yet. The good news is that you can appeal and request a redetermination, especially if you’ve had a life-changing event, such as lowered income due to retirement.

Dealing with a retirement tax bomb

Our goal for most of the clients we work with is to keep them in that first tier, so they have to pay only the $174.70. This can be tough, considering that we primarily work with people who have been diligent savers and are likely to have high required minimum distributions (RMDs) that they must take when they turn 73 or 75.

We call this a retirement tax time bomb because RMDs, combined with your Social Security and, potentially, a pension, may force you into higher Medicare tiers as time goes along. Our clients get good news, though, because we are able to help them plan for this.

We do this with strategies to help lower their income when the time comes. One popular strategy that many people are looking into right now is a Roth conversion, in which you move money from your tax-deferred investment to your tax-free investment.

For example, let's say you have a traditional IRA. You can convert some or all of it to a Roth IRA and pay the taxes now. Why would you want to do that? Because taxes are lower now than what we expect them to be in the future.

If you are 63 and younger, then the planning is a bit cleaner for you since you don't have to worry about Medicare premium increases when doing the Roth conversions. If you are 63 or older, then you need to be careful. We’re often asked if it makes sense to convert knowing that we will have to pay more in Medicare premiums now. This is not always smart to do, but you have to ask yourself: Would you rather pay higher Medicare premiums during a shorter amount of time or defer this problem to the future and have to pay increased Medicare premiums for potentially the rest of your life? Many of our clients prefer to pull the bandage off quickly rather than bringing on pain slowly over time.

What if Medicare premiums rise?

Something that really concerns me is that the cost of Medicare is likely to rise in the future. Why do I think this? Because it has generally risen steadily over the last 20 years, and it's projected to continue rising. This means that people will be paying more for Medicare as their retirements continue. It also means that the income tiers shown in the chart above could go even lower, making more people subject to income-related adjustments, making it even more important to ensure lower income in retirement, when it means the most.

My last thought on IRMAA: Do not lose the majority of your Social Security benefit as you progress throughout retirement. As most of us know, Medicare premiums are taken out of our Social Security payments. With the cost of Medicare continuing to increase, those who are in the higher income tiers may find themselves without any Social Security check left. In fact, they may actually have to pay the government above and beyond their Social Security benefit to cover their Medicare costs.

Also, keep in mind that Social Security cost-of-living adjustments (COLAs) have not kept up with inflation or rising Medicare costs over time, which makes this even more of a concern. Why work for 40 years, pay into a system and then not see the rewards? The good news is that there are ways you can preserve your Social Security check and ensure that you maximize your retirement savings — and make your money last as long as you do.

The appearances in Kiplinger were obtained through a PR program. The columnist received assistance from a public relations firm in preparing this piece for submission to Kiplinger.com. Kiplinger was not compensated in any way.