/Honeywell%20International%20Inc%20operations%20facility%20by-JHVEPhoto%20via%20iStock.jpg)

Charlotte, North Carolina-based Honeywell International Inc. (HON) provides industrial automation, building automation, and energy and sustainability solutions businesses. Valued at $70.3 billion by market cap, its business is aligned with powerful megatrends – automation and energy transition, underpinned by its Honeywell Accelerator operating system and Honeywell Forge IoT platform. The diversified industrial conglomerate is expected to announce its fiscal second-quarter earnings for 2026 before the market opens on Thursday, Jul. 23.

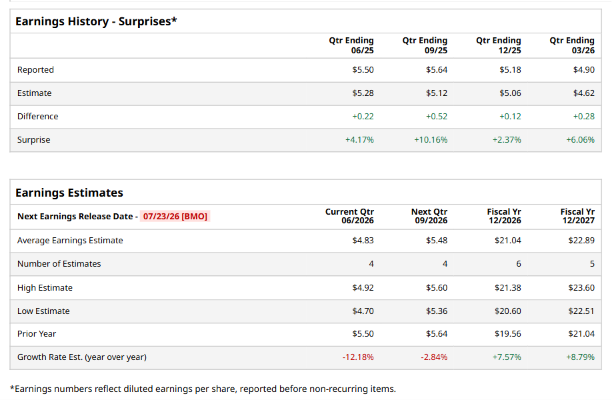

Ahead of the event, analysts expect HON to report a profit of $4.83 per share on a diluted basis, down 12.2% from $5.50 per share in the year-ago quarter. The company has consistently surpassed Wall Street’s EPS estimates in its last four quarterly reports.

For the full year, analysts expect HON to report EPS of $21.04, up 7.6% from $19.56 in fiscal 2025. Its EPS is expected to rise 8.8% year over year to $22.89 in fiscal 2027.

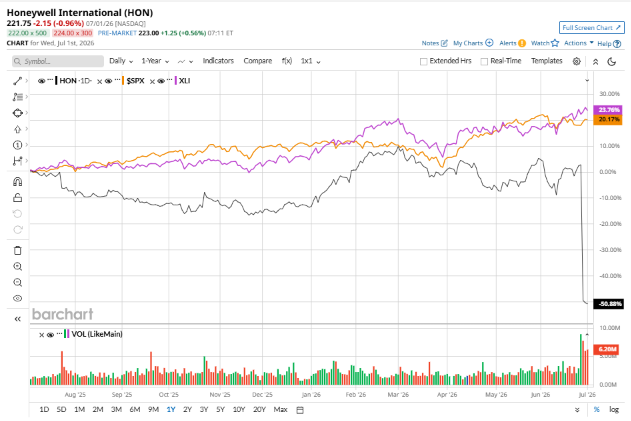

HON stock has significantly underperformed the S&P 500 Index’s ($SPX) 20.7% gains over the past 52 weeks, with shares down 50.8% during this period. Similarly, it considerably underperformed the State Street Industrial Select Sector SPDR ETF’s (XLI) 23.9% gains over the same time frame.

HON lagged as the market favored AI/tech over diversified industrials, with macro uncertainty and uneven manufacturing weighing on sentiment.

On Apr. 23, HON shares closed down by 2.6% after reporting its Q1 results. Its revenue was $9.1 billion, missing analyst estimates of $9.3 billion. The company’s adjusted EPS of $2.45 beat analyst estimates by 5.6%.

Analysts’ consensus opinion on HON stock is reasonably bullish, with a “Moderate Buy” rating overall. Out of 25 analysts covering the stock, 14 advise a “Strong Buy” rating, one suggests a “Moderate Buy,” nine give a “Hold,” and one recommends a “Moderate Sell.” HON’s average analyst price target is $457.27, indicating a potential upside of 106.2% from the current levels.