Cleveland, Ohio-based TransDigm Group Incorporated (TDG) designs and produces highly engineered aerospace components, primarily serving the commercial and military aircraft sectors. Valued at a market cap of $72 billion, the company is scheduled to announce its fiscal Q2 earnings for 2026 in the near future.

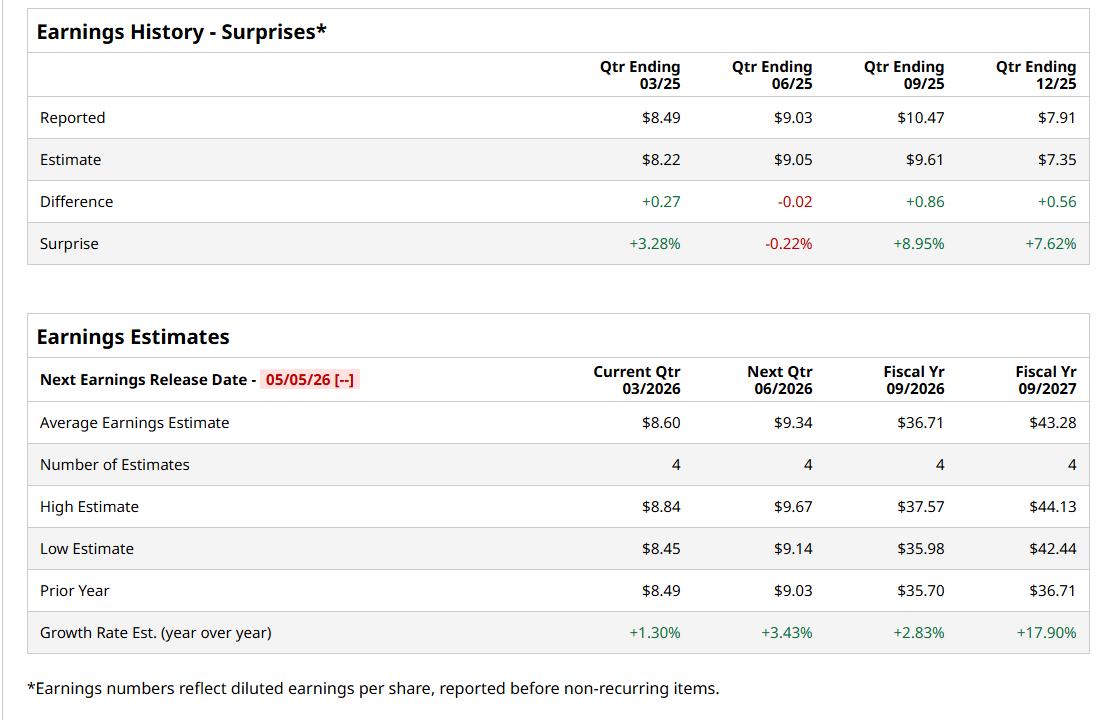

Before this event, analysts expect this aerospace & defense company to report a profit of $8.60 per share, up 1.3% from $8.49 per share in the year-ago quarter. The company has topped Wall Street’s bottom-line estimates in three of the last four quarters, while missing on another occasion. Its earnings of $7.91 per share in the previous quarter outpaced the forecasted figure by 7.6%.

For the current fiscal year, ending in September, analysts expect TDG to report a profit of $36.71 per share, representing a 2.8% increase from $35.70 per share in fiscal 2025. Furthermore, its EPS is expected to grow 17.9% year-over-year to $43.28 in fiscal 2027.

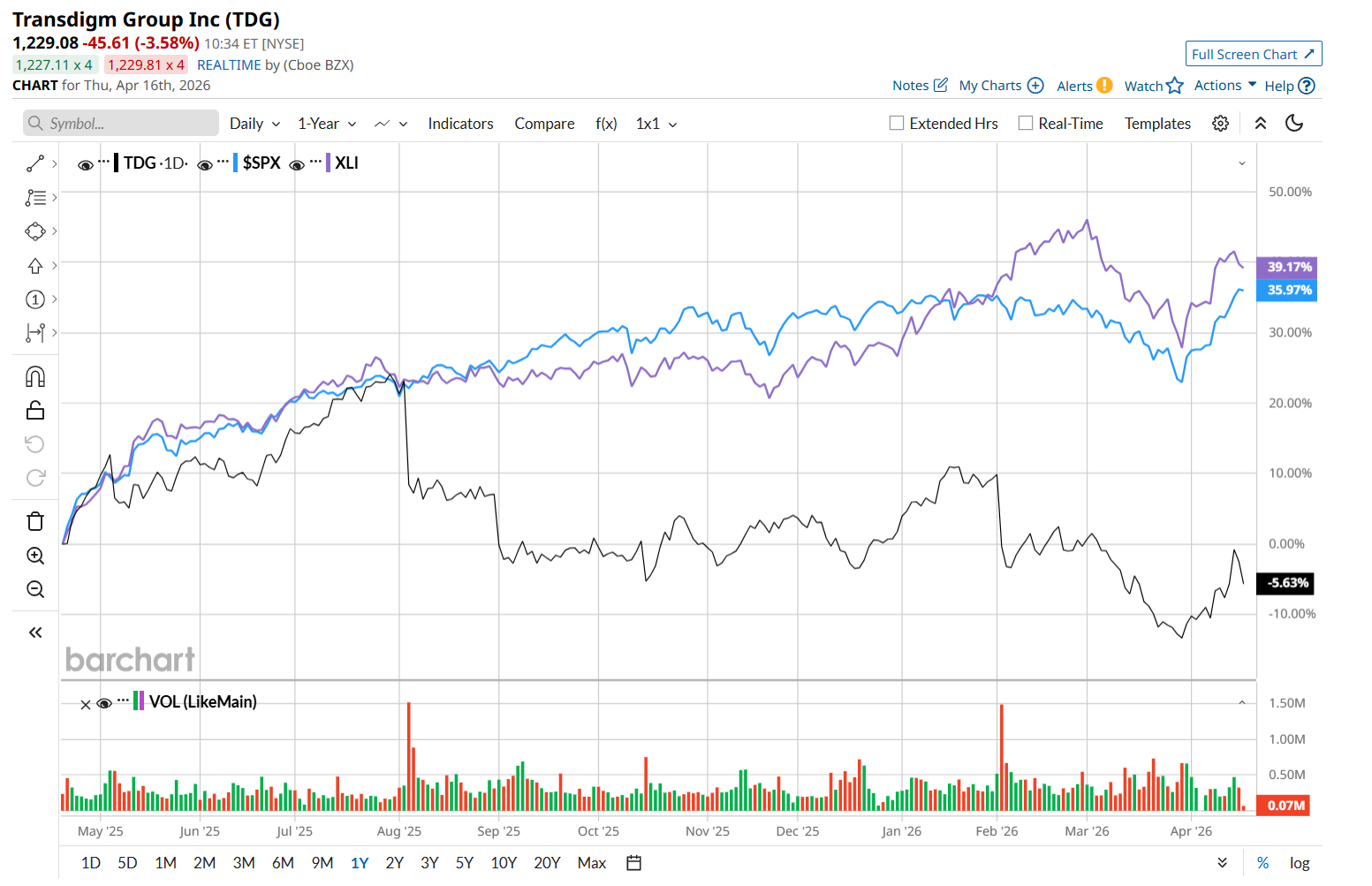

TDG has declined 5.8% over the past 52 weeks, considerably underperforming both the S&P 500 Index's ($SPX) 30.1% return and the State Street Industrial Select Sector SPDR ETF’s (XLI) 37.4% uptick over the same time period.

On Apr. 14, TDG’s shares soared 5.2% after the company announced preliminary second-quarter results highlighting strong financial performance. It reported estimated net sales of up to $2.545 billion and adjusted EBITDA of as much as $1.335 billion. The solid results boosted investor confidence in the company’s ability to sustain its industry-leading margins, supported by strong demand in both the commercial aftermarket and defense segments.

Wall Street analysts are moderately optimistic about TDG’s stock, with a "Moderate Buy" rating overall. Among 23 analysts covering the stock, 14 recommend "Strong Buy," and nine suggest "Hold." The mean price target for TDG is $1,551, indicating a 26.1% potential upside from the current levels.