Haleon plc (HLN) is one of the world's largest consumer healthcare companies, formed from the combined consumer health divisions of GSK (GSK), Pfizer (PFE), and Novartis (NVS), and went public in July 2022. Haleon operates across six major therapeutic categories: oral health, vitamins, minerals and supplements (VMS), pain relief, respiratory health, digestive health, and therapeutic skin health.

Its iconic brand portfolio includes Sensodyne, Advil, Centrum, Panadol, Voltaren, and Theraflu, spanning markets across North America, EMEA, Latin America, and Asia Pacific, making it a go-to name in the everyday wellness and self-care space.

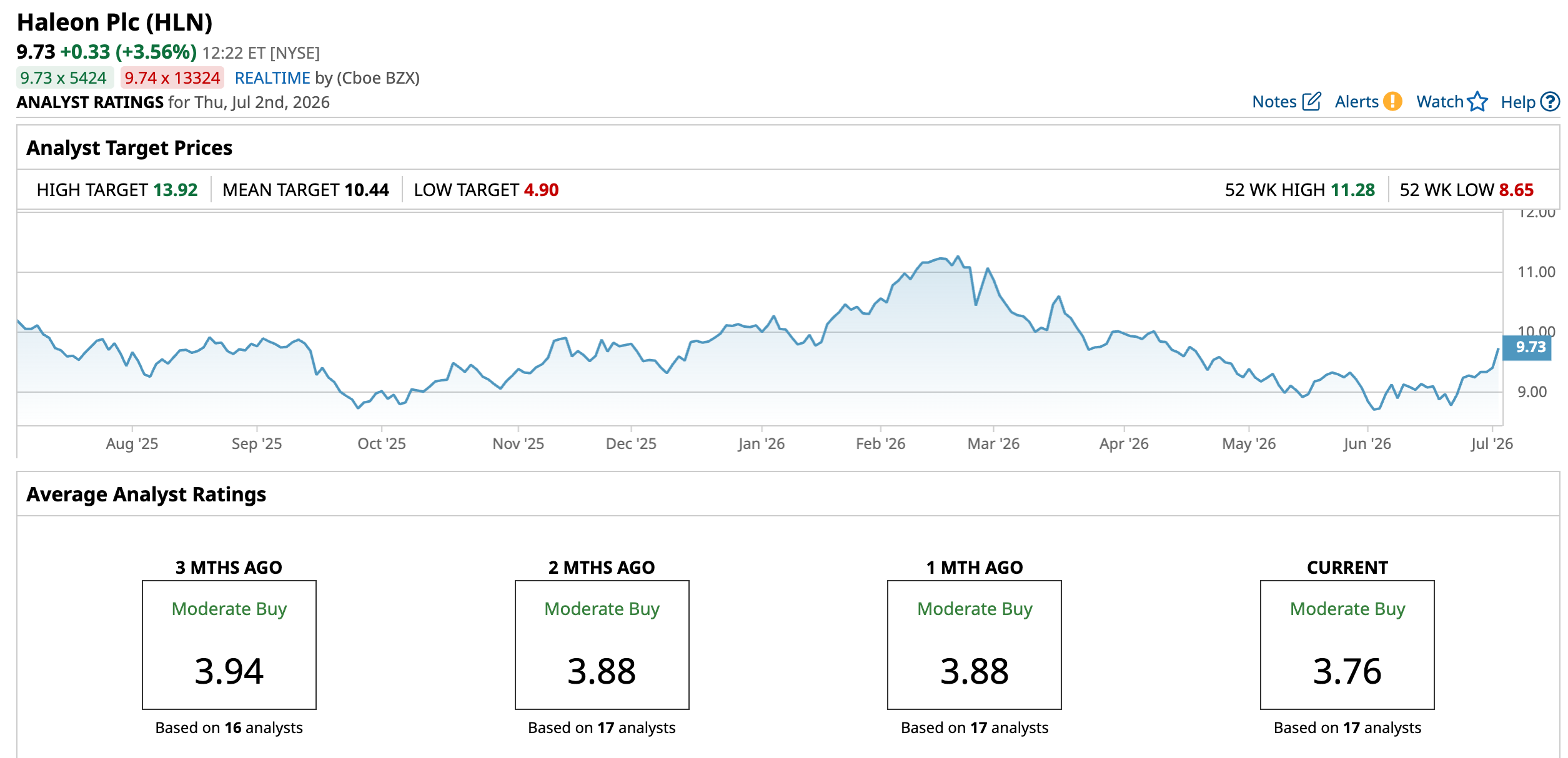

Haleon Stock Performance

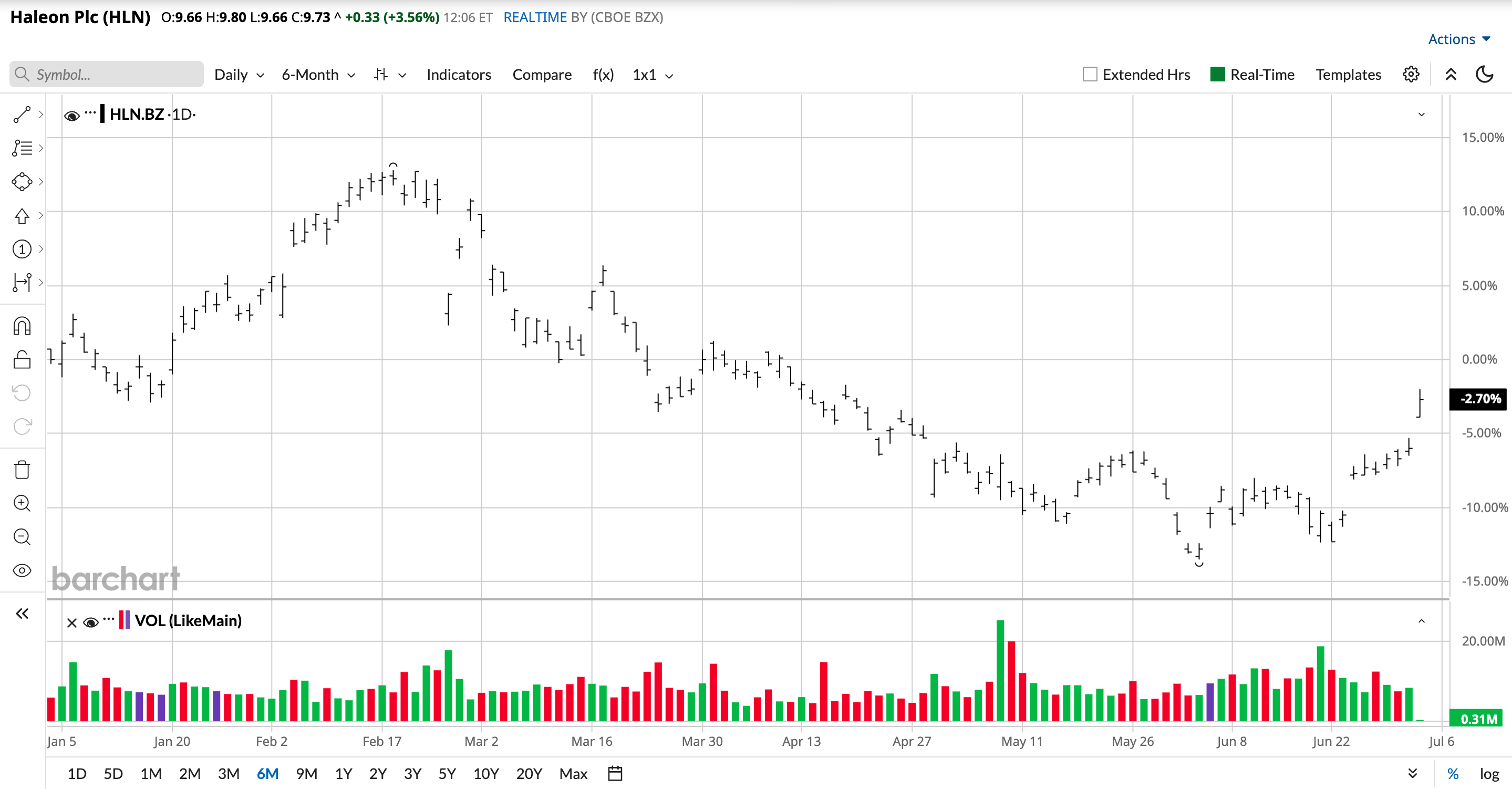

HLN shares are trading well below the 52-week high of $11.28, reflecting a meaningful pullback from peak levels amid investor concerns over top-line softness and macroeconomic headwinds weighing on consumer spending. The stock's 52-week low stands at $8.65, with a market capitalization of approximately $41.44 billion.

Compared to the S&P 500 Consumer Staples Index ($SRCS), which has broadly held up as a defensive play in 2026, HLN has underperformed its sector peers, dragged down by cold and flu season weakness and sluggish North American volumes, despite strong margin improvement and oral health momentum.

Haleon Posts Mixed Results

Haleon reported full-year 2025 revenue of £11.0 billion with 3.0% organic growth, falling short of its stated medium-term guidance range of 4-6%. The revenue miss was primarily driven by a weak cold and flu season and low consumer confidence in North America, with analysts having penciled in growth closer to 3.5% for the year. On the earnings front, however, Haleon surprised to the upside: the company reported $0.129 in earnings per share, beating the consensus estimate of $0.124 by $0.005.

Despite the top-line shortfall, Haleon delivered adjusted operating profit growth of 10.5% and expanded gross margins by 220 basis points, significantly exceeding its annual target of 50-80 basis points, with adjusted gross profit margins reaching 65.2%. Oral Health led the portfolio with 7.9% growth to £3.46 billion, benefiting from innovation and premiumization initiatives, while Asia-Pacific emerged as the regional growth leader with 5.2% organic revenue growth. Pain Relief and VMS delivered steady contributions, while Respiratory Health declined due to the muted cold and flu season.

Looking ahead, management reaffirmed confidence in its medium-term revenue growth guidance of 4-6%, underpinned by its Win as One strategy, strong brand equity, and a healthy innovation pipeline. For FY 2026, guidance calls for 3-5% organic growth and high single-digit operating profit growth, with sequential improvement expected as North America, China, and Latin America accelerate. Distribution wins at Walmart (WMT), Target (TGT), and Costco (COST) are expected to drive better growth in Q2 and beyond, while the company's five-year productivity target of £800 million in gross savings by 2030 continues to support long-term margin expansion.

Haleon Partners with Microsoft

Haleon has entered into a five-year strategic partnership with Microsoft (MSFT) to accelerate its AI-powered digital transformation, forming a key pillar of the consumer healthcare giant's "Win as One" growth strategy. Building on its existing deployment of Microsoft 365 Copilot, the collaboration will expand the use of agentic AI, security, and identity technologies across Haleon's global operations, automating routine tasks, boosting employee collaboration, and driving enterprise-wide productivity gains.

The two companies will jointly develop AI applications across critical business functions, while Haleon deepens its commitment to Microsoft Azure as its primary cloud platform, leveraging scalable infrastructure, advanced analytics, and enterprise-grade security. The deal signals Haleon's ambition to embed AI at scale as a driver of structural efficiency, complementing its ongoing £800 million productivity-savings target and margin-expansion roadmap through 2030.

Should You Buy HLN?

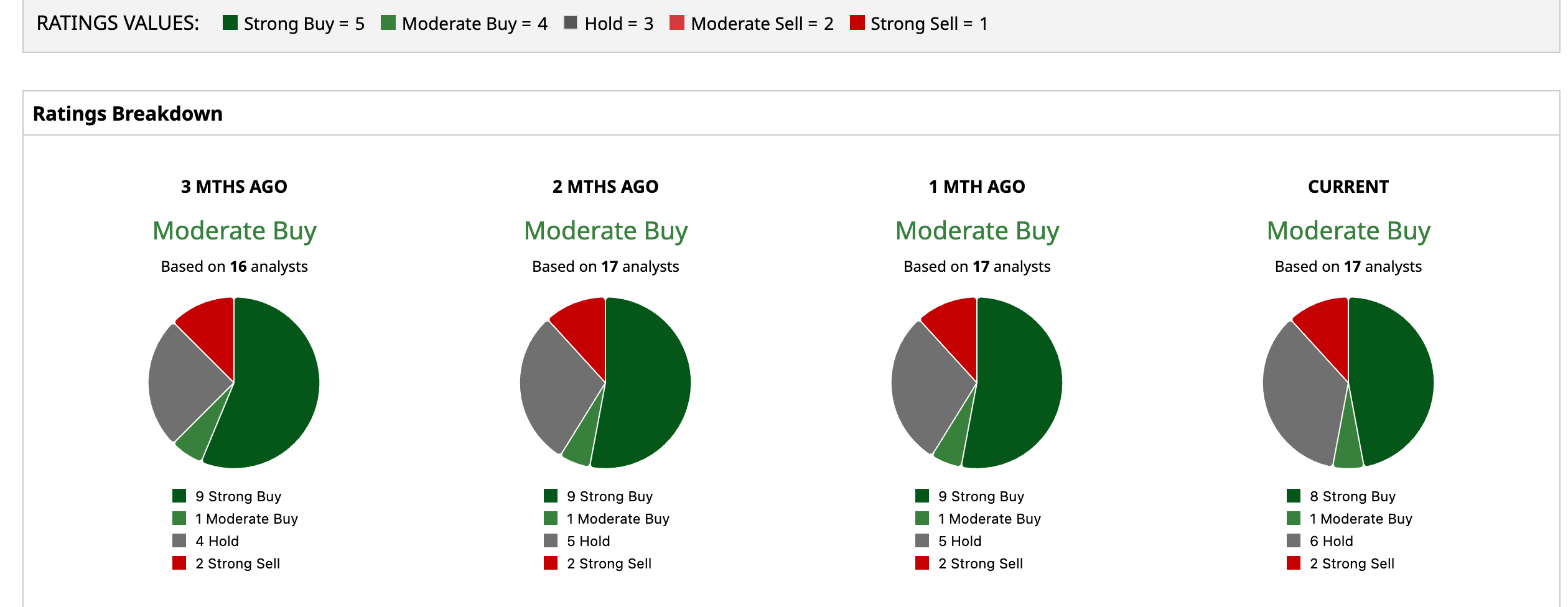

Haleon's five-year Microsoft partnership reinforces its productivity-first narrative, adding an AI-driven efficiency layer to an already compelling margin expansion story. Wall Street appears cautiously optimistic with a consensus "Moderate Buy" rating across 17 analyst ratings, including eight “Strong Buy,” one “Moderate Buy,” six “Hold,” and two “Strong Sell” recommendations. The mean price target of $10.44 implies 7.3% upside from current levels, modest but meaningful for a defensive consumer health name with durable brand equity and a clear path to its medium-term 4-6% growth guidance.