The Bank of England (BoE) already faced a tough decision at its next meeting on 5 May. How to quell inflation without scuppering the UK economy? GDP, employment, and inflation data this week just made the BoE’s job a whole lot harder. That’s potential bad news for GBP/USD, which rode high on a hawkish BoE at the turn of this year. Meanwhile, the US Federal Reserve is now steadfast in its commitment to raise interest rates in the face of high inflation.

Everything was different prior to the BoE’s March meeting. One of the first major central banks to begin raising interest rates in December of last year, the BoE was expected to keep better pace with the Fed in terms of policy tightening. A 15 bps points rise in December, followed by a 25 bps in February and March. Voting patterns in February pointed to the prospect of 50 bps clips at one stage, before a more cautious BoE in March brought down future expectations of interest rate hikes.

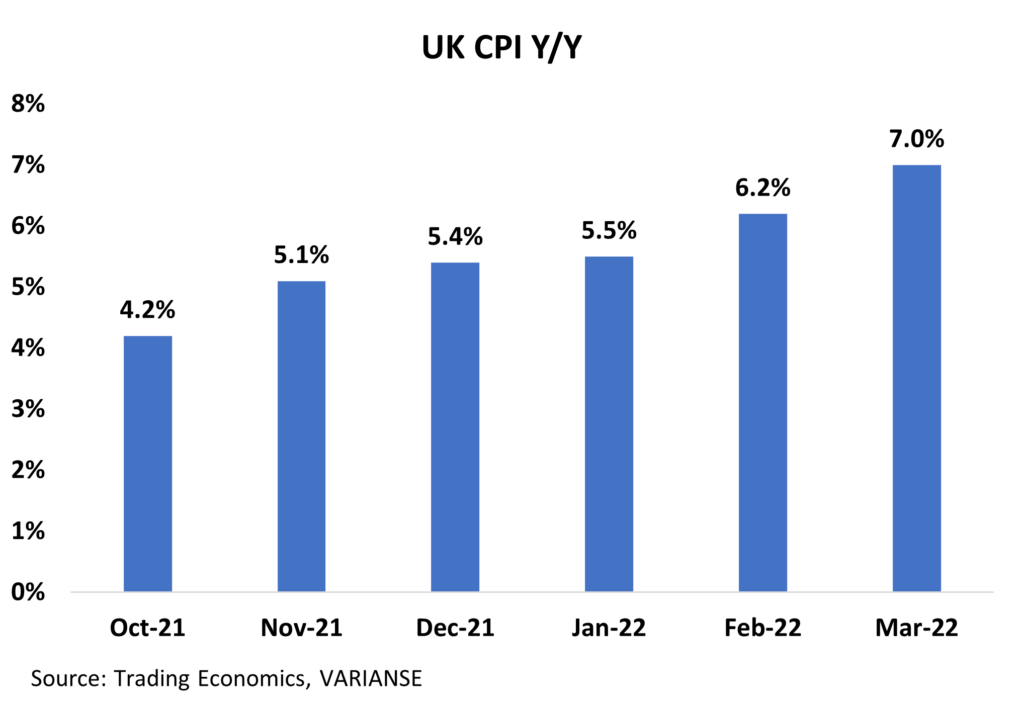

In that context, the Bank of England (BoE) would have found Wednesday’s March UK CPI report unsettling. Headline CPI accelerated to 7% y/y - its highest rate since 1992 – up from an already eye-watering 6.2% y/y in February. Worse still for the BoE, inflation for the full quarter stood at 6.2% y/y, well above the 5.7% y/y forecasted in the BoE’s February Monetary Policy Report and the implied estimate of 5.8% in the March Monetary Policy Summary. Higher energy prices due to war in the Ukraine has certainly been a key factor behind rising inflation.

Revisiting the counterfactual on inflation had there been no war, however, doesn’t make the BoE’s job any easier going forward. UK core CPI, which excludes energy, food, alcohol, and tobacco also accelerated for a sixth consecutive month to 5.7% y/y in March. The February UK Labour Market Report also indicated a further fall in employment and a rise in headline wage growth. These are all signs that underlying inflation pressures may be on the rise.

At the same time, February UK GDP data released showed a sharp deceleration in economic activity in March with the prospect of flat growth moving into Q2, according to National Institute of Economic and Social Research (NIESR). Evidence of slowing growth and a persistent but uncertain inflation outlook, pose a serious challenge for the BoE and its capacity to keep pace with the US Federal Reserve in terms of tightening policy. Ceteris paribus, this means downside pressure on GBP/USD could persist.