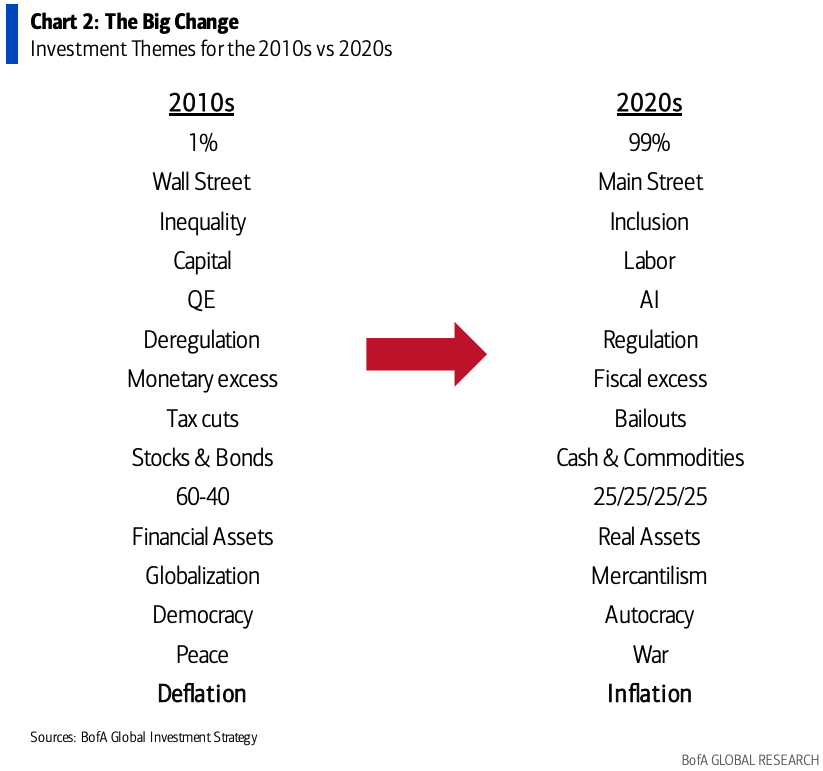

The 2010s were marked by the Global Financial Crisis from the end of the previous decade. It was an era of recuperative, ultra-accommodative monetary policy, relative peace, and low inflation that helped investors outperform many of the world’s top hedge funds using simple buy-and-hold equity strategies. But the 2020s have already been far different.

A global economic wrecking ball called COVID-19 welcomed investors into the new decade. And that wrecking ball, along with the fiscal and monetary responses to it, led to an inflationary hangover in 2021 that has forced central banks into a series of historic and aggressive interest rate hikes over the past two years. Now, there’s war in the Middle East and Eastern Europe, and geopolitical tensions are brewing between the U.S. and China. The 2020s are a whole new decade, with a whole new attitude, and Bank of America Research sees 15 major themes that will define it.

In a Monday research note, a Bank of America team led by chief investment strategist Michael Hartnett broke down changes they expect to see (and are already seeing) in the economy this decade—as well as what those changes could mean for investors. Looking through their findings, one thing’s for sure: from the threat of war to the impact of AI, there is a lot of upheaval and uncertainty on the horizon.

From peace to war

The first and most frightening theme change between the 2010s and the 2020s is the shift from “peace to war.”

Hartnett and his team warned that there has been a “reversal of globalization” in recent years, and that could lead to more inflationary trade barriers, sanctions, or embargoes. The Israel-Hamas conflict also “adds to belief that war not peace will dominate the 2020s.” If the conflict worsens leading energy producing superpowers to get involved, it could even threaten the supply of oil and gas globally.

“War is expensive and inflationary,” the BofA team wrote. “Periods of global peace are an exception, periods of war the norm.”

The conflicts in the Middle East and Ukraine are historic, and with tensions between the U.S. and China still brewing, it’s all starting to feel awfully like “a new cold war,” according to Kevin Philip, a partner at the wealth management firm Bel Air Investment Advisors. “The world has already transitioned from the free flow of capital and globalization orthodoxy … to a new regime of bipolar spheres of influence,” he warned.

BofA seconded his remarks with one of its many mind-expanding charts for the report, showing “600 years of War,” and how this scary period is thankfully nothing like the horrors of the mid-20th century in terms of death toll.

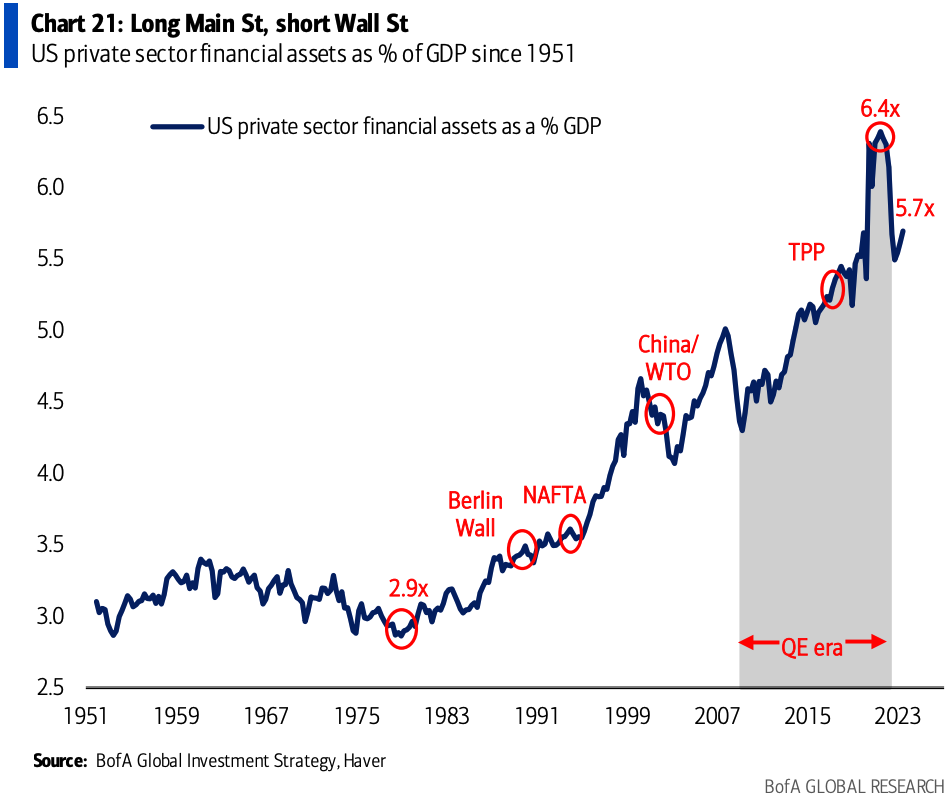

Wall Street to Main Street

Another key theme Bank of America cited was the shift from an economy that provided a decade of success for Wall Street to something that is more likely to help Main Street.

Hartnett and his team noted that the value of financial assets (Wall Street) relative to the value of the economy (Main Street) surged in the 2010s. But the next decade may favor Main Street businesses—and workers. BofA expects “structural policies” from regulation to reshoring to help U.S. business, “reverse wealth inequality and raise the value of labor.”

On top of that, politicians are more likely to favor Main Street voters’ “desire for greater government spending” than Wall Street’s calls for fiscal discipline, Hartnett and his team wrote. That should boost the value of the Main Street economy relative to Wall Street’s financial assets.

Something BofA didn’t note, but supportive of this theory, is how the only wage growth across the inflationary economy has come among blue-collar workers. And that does not include the large wage gains won by the 10% of the economy that is unionized, including UPS drivers and Big Three auto workers.

Bigger governments and bigger debts

Bigger governments come with more debt. And that’s apt to be an influential theme in the 2020s, according to BofA. The U.S. governments’ deficit in the third quarter surged to 8% of GDP, and the national debt is now over $33.7 trillion. It’s a path that may prove to be unsustainable at some point, and investors should take note of the consequences for bond yields.

Hartnett argued that a lack of fiscal discipline in Washington is “a big reason why bond yields have risen so dramatically in recent years.”

“A new investment risk is that bond yields may need to rise to levels that cause greater fiscal spending discipline,” he said, warning that 2024 is also “a huge election year which is not a political incentive for discipline.”

The AI age and an era of regulation

The rise of artificial intelligence has already been an influential theme in the 2020s. And Bank of America’s strategists believe that AI will ultimately boost worker productivity and increase profits, but the timing of that outcome is still uncertain.

“Bears will point out that from steam power to the internet there has always been a lag between innovation and widespread social, corporate and economic adoption,” Hartnett and his team wrote.

AI may well usher in the “4th industrial revolution,” but it’s a “disruptive technology” that could also have negative impacts. After all, the fastest way for AI to increase productivity would be to put workers out of a job, BofA warned.

The risks brought about by AI, coupled with the dominance of big tech giants over the past decade, could lead to increasing regulation and antitrust scrutiny in the 2020s.

“The social & wealth inequality that has resulted from tech disruption, the monopolistic power of Big Tech, plus unintended consequences of greater AI, clearly threaten the sector’s singular dominance via greater regulation & taxation,” Hartnett and his team wrote. “Hence the sectors increasing claims to be a sector of national security.”

Deflation to inflation

Finally, the 2010s were a decade of low, relatively stable inflation in the U.S., but Hartnett and his team believe that is now over. While the Federal Reserve has made some serious progress in taming inflation since they began raising interest rates in March of 2022, BofA’s experts said the central bank is likely to give up before the job is done.

“We believe the next recession prompts policy panic well before inflation is close to the Fed’s target of 2%,” they wrote.

For investors, that means that assets that typically perform during periods of low inflation and interest rates, like tech and growth stocks, could underperform assets that typically perform well when prices are rising, like cash, commodities, and value stocks.

“In 2023 deflationary US tech/growth stocks have rallied but we are sellers into a 2023 recession, and we would buy inflation assets such as commodities, real estate, value cyclicals as recession begins,” Hartnett and his team wrote.