Twenty-nine billion pounds is a lot of money. It’s how much we estimate the total annual revenue to British electricity generating stations increased as a result of last year’s energy crisis – from £20.5 billion before COVID (in 2018 and 2019) to £49.5 billion in 2022. The indications are that these revenues increased by about twice as much as overall generation costs.

Getting at the numbers is not easy. Britain has a competitive market for “wholesale” electricity, the bulk electricity sold by major generating companies from fossil fuel (overwhelmingly gas), nuclear and renewable energy power stations.

The price is set in an auction between the electricity consumers (large industries or electricity suppliers that purchase electricity for their clients) and its generators. Consumers submit the demand they are expecting during the next day, and generators offer a block of electricity to meet this demand for a certain price. The price in this “day-ahead” market reflects the cost of the highest-priced block needed to match demand.

Renewables and nuclear plants are relatively cheap to operate. But fossil fuels, although more expensive, are still required to meet demand nearly all the time. This means that gas largely sets the day-ahead price, with a margin. In 2021, the electricity price followed gas prices 98% of the time in Britain, despite gas generating only 40% of the country’s electricity.

But this is just the beginning of the pricing complexities. In practice, much gas and electricity is traded through forward contracts. Your electricity suppliers need to know they can buy the electricity their customers will demand, so they “buy forward” from generators on contracts ranging from months to more than a year ahead – usually at prices reflecting conditions at the time of contracting.

On purely day-ahead prices, the total revenue in 2022 would have soared by almost £40 billion. Our best estimate of forward-contract structures brings this down to the £29 billion indicated for last year.

However, this likely means some of the huge day-ahead prices in 2022 have been shifted forward into this year, whatever happens to gas generation costs (in reality, gas prices fell slightly during the first half of 2023).

Furthermore, gas-powered electricity generators buy their gas in advance, to be sure they have the fuel to generate – so a lot of their generation this year could reflect last year’s gas prices.

Our first conclusion: whatever happens to gas prices, don’t expect electricity prices to drop fast.

Soaring revenues

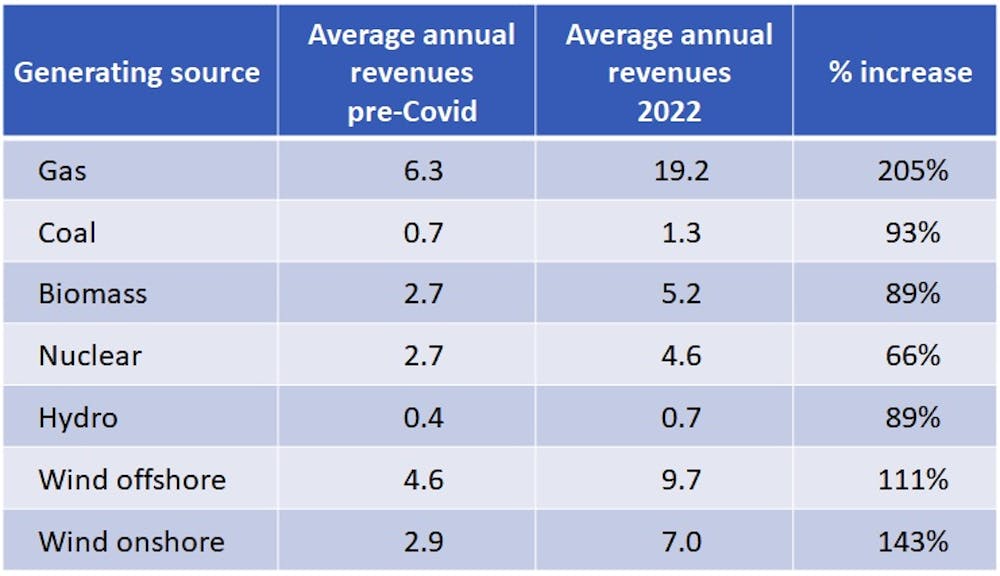

A key finding from our research is how revenue changed for different generators, with the growth for renewables of particular note. We estimate their revenue doubled from £7.7 billion pre-COVID to £15.5 billion in 2022 – yet there is no reason to think their costs increased.

Nuclear benefited too – but proportionately less than renewables. Nuclear generators sell more electricity on a year-ahead basis, given its predictable cost and output levels.

How revenues changed for different electricity generators (£ billion/year):

Perhaps the biggest surprise regards gas generation. Since these companies’ costs shot up following the start of the Ukraine war, it seems no surprise that their prices did too. We estimate their total annual revenue rose by about £13 billion, roughly trebling from the pre-COVID average of £6.3 billion. But the evidence suggests that this increase was, in fact, much bigger than the increase in their costs.

An industry metric called the “spark spread” historically gave gas generators an operating margin of about £5 for each megawatt hour (MWh) of electricity generated. That quadrupled in 2021 and doubled again in 2022, to an average of over £40 per MWh. This correlates with our best estimate that, while gas generators paid more for gas, their bill rose by a lot less than the £13 billion increase in their total revenue.

So what happened?

Electricity is supposed to be a competitive market, with competition holding down prices. But in reality, there is little competition between gas and other generating sources in Britain, since these other sources can’t increase their output or rapidly build more capacity when gas generators put their prices up.

Until at least 2020, a major factor constraining higher prices in the wholesale market was imports through interconnectors from mainland Europe. Yet, factors including post-Brexit trade frictions and low hydro (Norway) and nuclear (France) generation have impeded the inflows of competitive electricity from continental Europe over the past few years.

Exacerbated further by the gas crisis in Europe, this meant electricity generators in Britain were able to raise prices further above costs.

In the final quarter of 2022, the generators also knew that raising their prices even higher would not ultimately matter to customers – because in October last year, the UK government committed to subsidising energy bills down to £2,500 per household through its Energy Price Guarantee.

In addition, gas generators are exempt from paying the new Electricity Generation Levy – which imposes a tax of 45% on the revenues of electricity generators for the fraction of electricity they sell at above £75 per MWh each year. This levy is applied only to those generators who were assumed to be benefiting from the exceptional wholesale prices while their costs hadn’t increased.

Implications for the future

The real paradox is that all this happened just as non-fossil sources, with stable costs, started to account for more than half of Britain’s electricity (56% if we include nuclear).

As renewables expand further, we will start to see more periods when renewables and nuclear can meet electricity demand, so that gas no longer sets the day-ahead price and the wholesale price collapses. By 2030, non-fossil generation is expected to account for more than 75% of total electricity generation in both the UK and the EU. However, most of the time, the day-ahead price will still be set by the sliver of fossil fuels that are still required.

Given the experience of the past year, and what we will see this year in terms of high wholesale electricity prices, this doesn’t really make sense. For how long can the declining fossil fuel tail continue to wag the dog of Britain’s renewables-based electricity system?

Don’t have time to read about climate change as much as you’d like?

Get a weekly roundup in your inbox instead. Every Wednesday, The Conversation’s environment editor writes Imagine, a short email that goes a little deeper into just one climate issue. Join the 20,000+ readers who’ve subscribed so far.

Michael Grubb has received funding from the Aldersgate Group for work on electricity markets, and BEIS/DESNZ for work on the economics of energy transition

Serguey Maximov Gajardo receives funding from the Aldersgate Group for work on electricity markets.

This article was originally published on The Conversation. Read the original article.