Nayib Bukele, the president of El Salvador, helped make global history last summer after receiving an overwhelmingly favorable vote for his proposal to adopt bitcoin as a legal currency. The decision went into effect in September and, over the course of the last eight months, the cryptocurrency’s volatile nature has already begun to rear its head in damaging ways.

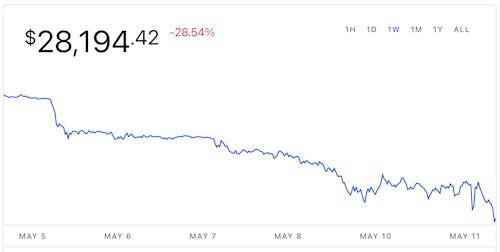

The value of bitcoin, which can fluctuate with as little as a post from Elon Musk, has dropped significantly in the wake of an ongoing war in Ukraine and rising inflation in the U.S. Bitcoin has now fallen below 50 percent of its all-time high.

Normally, this drop wouldn’t be of much importance to anyone who isn’t significantly invested in a crypto-focused future, but because El Salvador’s economy is tied to the currency, the consequences have been steep: Government bonds for the Latin-American country are trading at an average of 40 percent of their original value.

Cascading spiral —

To make matters worse, Fitch Ratings, an American credit rating agency and one of the biggest of its kind in the world, has downgraded El Salvador to a CCC rating, a designation that suggests the institution in question is vulnerable to nonpayment.

Here’s an excerpt from the agency’s statement on the demotion:

In Fitch's view, weakening of institutions and concentration of power in the presidency have increased policy unpredictability, and the adoption of bitcoin as legal tender has added uncertainty about the potential for an IMF program that would unlock financing for 2022-2023.

Ultimately, El Salvador is in a position where it is saddled with debt, at risk of high borrowing costs due to a lowered credit rating, and still linked to the whims of bitcoin’s volatility. If anything, this decision to adopt bitcoin as legal tender serves as a cautionary tale about misplaced trust in the future of cryptocurrency.

This development also arrives on the heels of a Fortune report that points out more fissures in the viability of crypto, as Coinbase, the largest cryptocurrency exchange in the world, has not only reported a 19 percent drop in monthly users during Q1, but in the event of bankruptcy, users would potentially lose everything stored in their accounts.

Despite the obvious holes in bitcoin — difficult to use for daily transactions, limited to people who have immediate internet access, and the general volatility of its value — there just isn’t the same level of scrutiny as there is with other blockchain adjacent tech like NFTs.