While the broader market has spent 2026 nursing a stress headache, courtesy of the U.S.-Iran war, surging oil prices, and recession whispers, one stock has decided that the memo simply does not apply to it. Sandisk Corporation (SNDK) is on a tear that would make even the most seasoned Wall Street veterans do a double-take.

Most people still picture Sandisk as that little memory card brand collecting dust in their camera bag. However, that perception is dangerously outdated. Over the past few years, the company has repositioned itself as one of the hottest names in the artificial intelligence (AI) space, and the market has rewarded that transformation handsomely.

The Nasdaq 100 Index ($IUXX) managed an 8.14% gain in 2026. Sandisk, which joined the index on April 20, has lapped that figure several times over, posting a three-digit return year-to-date (YTD). Investors are piling into the stock hand over fist, chasing the explosive demand for the flash storage chips the company manufactures at scale.

The thesis is straightforward. Rapid AI and cloud workload expansion are pushing data center NAND exabyte growth well beyond the capabilities of the overall supply. The imbalance has placed Sandisk's enterprise SSD portfolio squarely in the driver's seat, deepening its hyperscaler engagements and unlocking structurally higher pricing power that flows directly into earnings.

With growth prospects of this magnitude on the table, all eyes are now locked on what comes next. On March 31, Sandisk announced it would release its Q3 fiscal year 2026 earnings on Thursday, April 30, after the closing bell. The stock surged 11% on that news alone, then added another 9% the following session. Anticipation, it turns out, is its own catalyst.

So let us dig into Sandisk's playbook to figure out exactly where the stock goes from here.

About Sandisk Stock

The Milpitas, California-based Sandisk, spun out of Western Digital Corporation (WDC), is a leading developer, manufacturer, and provider of data storage devices and solutions built on NAND flash technology. With a market cap of $146.1 billion, its product lineup spans solid state drives, embedded products, removable cards, USB drives, and wafers and components.

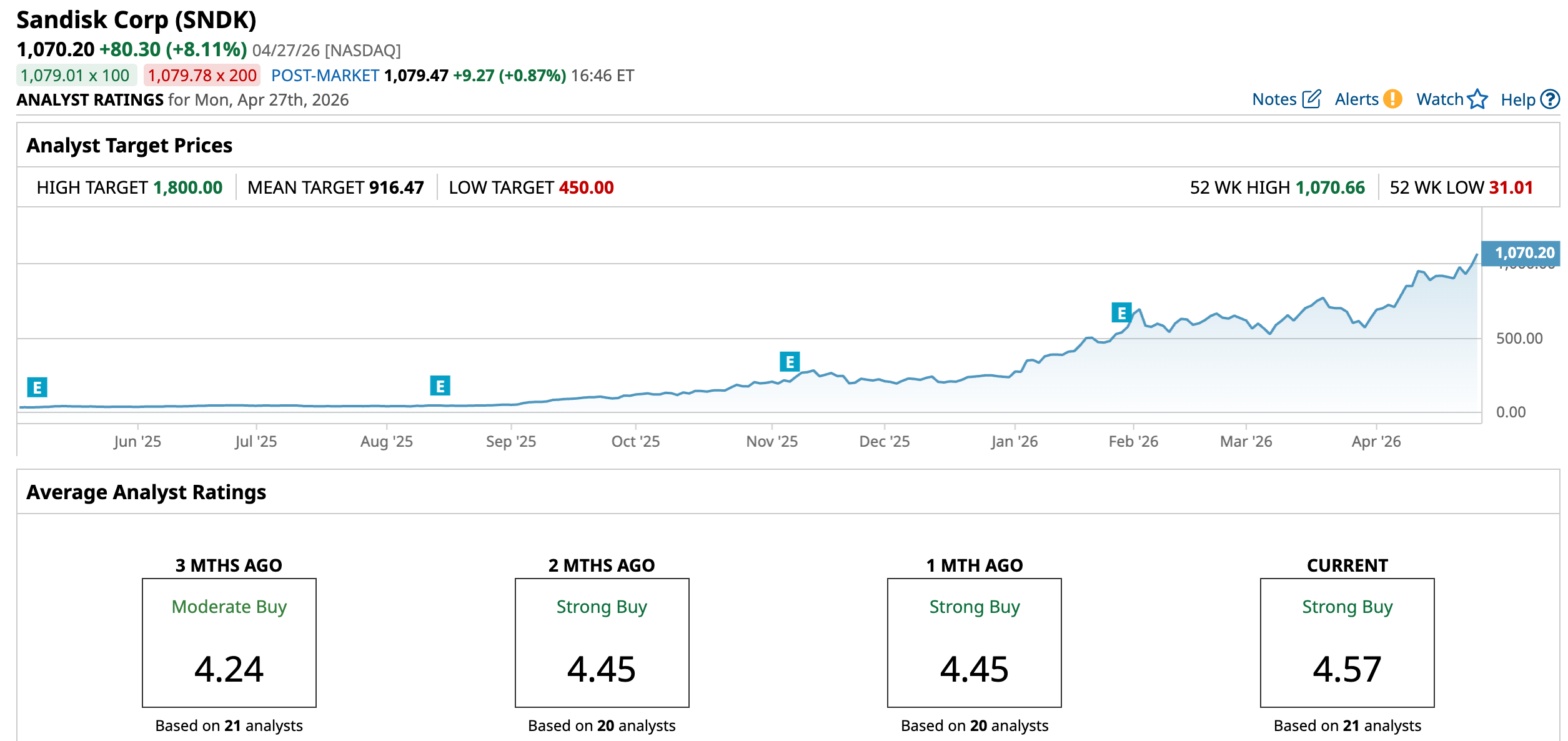

Coming to price performance, SNDK stock skyrocketed 3,158% in the past 52 weeks. In 2026 alone, it has surged 350.84% year-to-date (YTD), with the past month alone delivering a 73.78% gain, a pace that has left most of the market's other high-flyers looking pedestrian by comparison.

What makes the valuation case even more compelling is the price tag attached to all of this growth. SNDK stock is currently trading at just 23.90 times forward adjusted earnings, a multiple that sits below the industry average. For a company posting triple-digit returns and expanding its pricing power in real time, the discount seems like an open invitation.

Sandisk Surpasses Q2 Earnings

Sandisk reported its Q2 fiscal 2026 earnings on Jan. 29, owing to which the stock rose 2.2% on the day itself, then added 6.9% and 15.4% in the two trading sessions that followed. This marked three consecutive days of gains after an earnings print.

The numbers earned every bit of that reaction. Revenue surged 61.2% year-over-year (YOY) to $3 billion, comfortably clearing the Street's estimate of $2.69 billion. EPS grew 615.3% from the year-ago value to $5.15, blowing past the analyst forecast of $3.40.

AI continued to drive a step change in demand, with data center and edge workloads expanding both system complexity and storage requirements. Delving deeper, non-GAAP operating income climbed 386.3% to $1.1 billion, non-GAAP net income rose 443.3% to $967 million, and non-GAAP EPS increased 404.1% to $6.20.

The balance sheet told an equally clean story. Sandisk closed the quarter with $1.6 billion in cash against $603 million in debt. The company paid down an additional $750 million of debt during the quarter, ending with a net cash position of $936 million. Retiring debt aggressively while revenue accelerates is the hallmark of a business operating from genuine strength.

Free cash flow backed that up in full. Sandisk generated $843 million in adjusted free cash flow during the quarter, representing a 27.9% free cash flow margin.

Looking ahead, management has guided Q3 revenue between $4.4 billion and $4.8 billion, with non-GAAP EPS forecast between $12 and $14. They also flagged that the market will be even more undersupplied in Q3 than it was in Q2, signaling that pricing power is not softening anytime soon.

Analyst estimates reflect the full weight of that optimism. Wall Street projects Q3 fiscal 2026 EPS of $13.40, marking a 2,333.3% YOY increase. Full-year fiscal 2026 EPS estimates stand at $39.01, implying 2,091.6% annual growth, followed by another 129.2% jump to $89.39 in fiscal year 2027.

What Do Analysts Expect for Sandisk Stock?

Wells Fargo has raised its price target on SNDK stock to $975 from $675, though it held its “Equal Weight” rating on the shares. The firm candidly admitted it has "clearly missed SNDK," revising its EPS estimates aggressively to $125 for 2026 and $150 for 2027.

BofA struck a decidedly more bullish chord, lifting its price target to $1,080 from $900 while maintaining a “Buy” rating. The firm told investors that NAND pricing has moved up "massively."

It sees this cycle outlasting previous ones, driven by the mix shift toward data centers, sustained AI inferencing demand, and rational supply additions from NAND manufacturers. A longer cycle means a longer runway, and that runway translates directly into earnings growth.

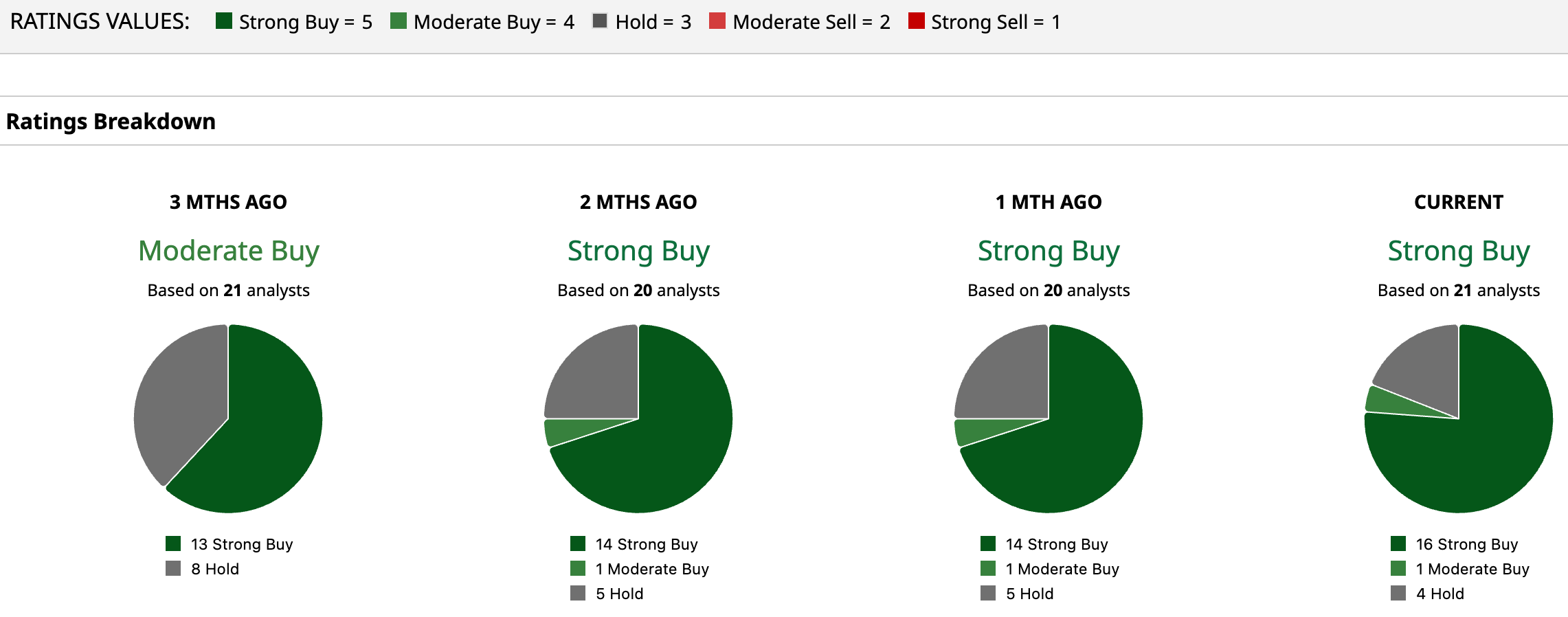

Wall Street has assigned SNDK stock an overall rating of “Strong Buy.” Among 21 analysts, 16 rate the stock a “Strong Buy,” one assigns it a “Moderate Buy,” and four suggest “Hold.”

The stock already trades above its average price target of $916.47, which in most cases would flash a caution signal. Here, however, the Street-high target of $1,800 points to a gain of 68.2% from current levels, and with earnings on the horizon, the next move could close that gap faster than most expect.