Last month, semiconductor process control supplier KLA Corporation (KLAC) announced that it would enact a 10-for-1 forward stock split of its outstanding common stock. The stock comes with a hefty price tag at the moment, shy of the $2,000 mark per share. Hence, the objective of this stock split is to make the shares more accessible, especially to retail investors, and increase liquidity.

KLA believes that this aligns with its long-term capital allocation strategy. The company’s split-adjusted quarterly dividend for August 2026 is expected to be $0.23 per share.

With the split shares set to start trading on June 12, we take a closer look at KLA now…

About KLA Corporation Stock

KLA Corporation, based in Milpitas, California, is a top supplier of process control and yield management technology for semiconductor manufacturing. The company creates sophisticated inspection equipment, metrology platforms, and computational analytics that help manufacturers identify defects, measure critical features, and guarantee quality across chip fabrication. The company has a market capitalization of $252 billion.

KLA partners with customers worldwide to deliver tools and services for producing wafers, reticles, integrated circuits, packaging, and printed circuit boards. By bringing together experts in physics, engineering, and data science, the company provides process-enabling solutions that fuel innovation in the electronics industry and help customers achieve manufacturing superiority.

KLA Corporation's stock surged over the past year due to booming demand for AI semiconductors, strong earnings beats, and its dominant market position in process control. As chipmakers invest heavily in advanced AI processors and memory, the company’s critical inspection tools become essential, driving revenue growth and investor confidence.

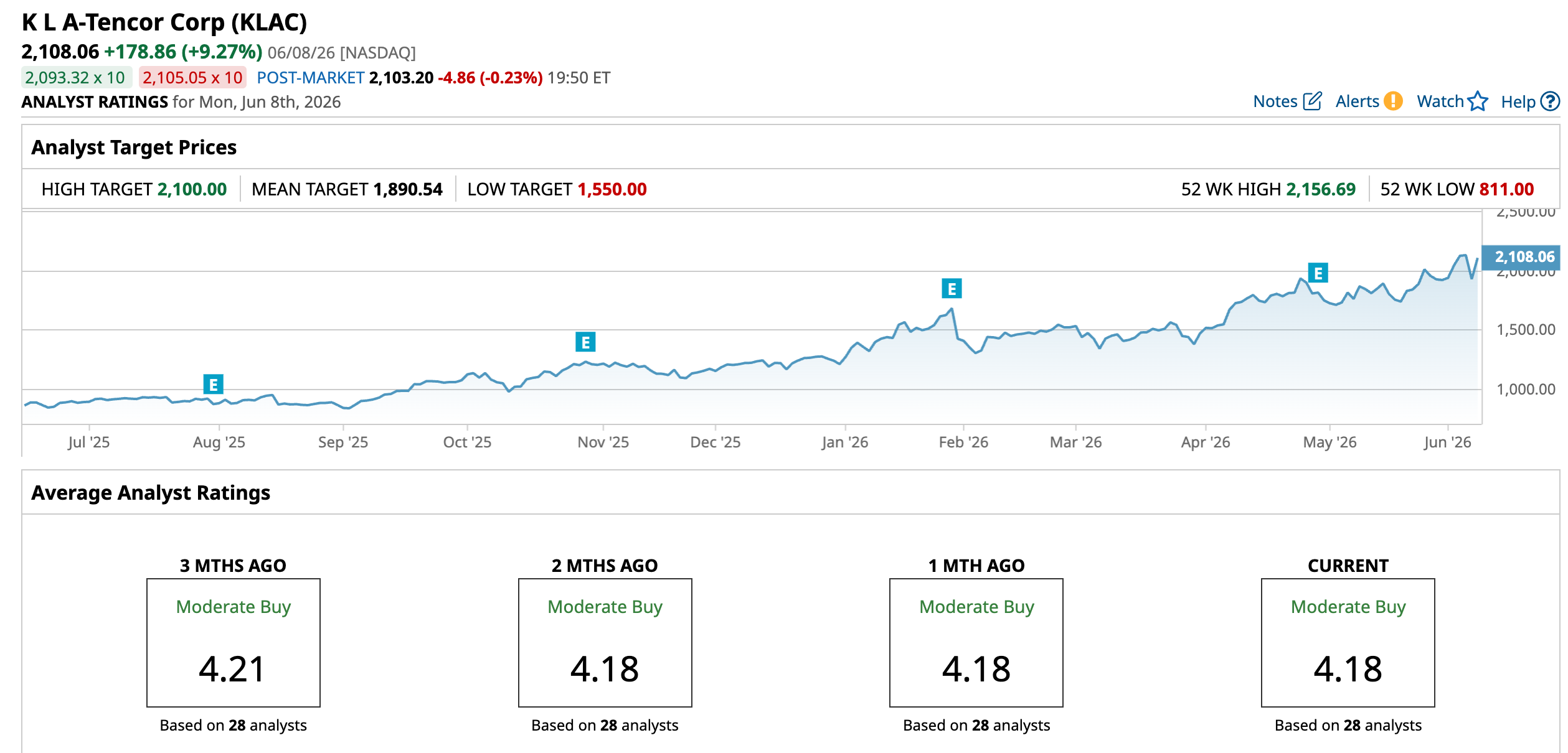

Over the past 52 weeks, the stock has gained 160.9%, while it is up 73.5% year-to-date (YTD). It reached a 52-week high of $2,156.69 on June 4, but is down 2.3% from that level.

On a forward-adjusted basis, KLA’s price-to-earnings (non-GAAP) ratio of 52 times is significantly higher than the industry average of 25.12 times.

KLA Corporation Soars in Q3 With Market Share Dominance in Process Control

KLA reported strong results in the third quarter of fiscal 2026 (quarter ended Mar. 31), as the company’s leadership in process control continues to gain momentum. Since 2021, KLA’s share of process control, 58% in 2025, has grown by 360 basis points and is approximately seven times that of the nearest competitor.

Sustained strength in investment in both leading-edge foundry/logic and high-bandwidth memory (HBM) led to the company reporting a revenue of $3.42 billion, up 11.5% year-over-year (YOY). This was also higher than the $3.38 billion that Wall Street analysts had expected. Its non-GAAP EPS also rose by 11.8% YOY to $9.40, surpassing the $9.16 that analysts had expected.

KLA stated that its results can be directly correlated to AI, as the company’s systems apply to AI-driven operations. In fact, over the past five years, the company’s entire product portfolio has been enabled with increasing AI capabilities.

Wall Street analysts are optimistic about KLA’s future earnings. They expect the company’s EPS to climb by 6.3% YOY to $9.97 for Q4 FY2026. For fiscal 2026, EPS is projected to surge 11.4% annually to $37.06, followed by 34.3% growth to $49.77 in fiscal 2027.

What Analysts Think About KLA Corporation’s Stock

Last month, analysts at Citigroup maintained a bullish “Buy” rating on KLA and raised the price target from $1,800 to $2,064. In April, Needham raised the price target on KLAC from $1,800 to $2,000, while keeping a “Buy” rating. Needham analysts believe that the company is very confident about the 2027 acceleration. The analyst firm stated that it considers KLA a through-cycle share gainer, while competitors experienced fluctuating shares within the cycle. Wells Fargo analyst Joseph Quatrochi maintained an “Overweight” rating for KLAC while raising the price target from $1,900 to a Street-high of $2,100.

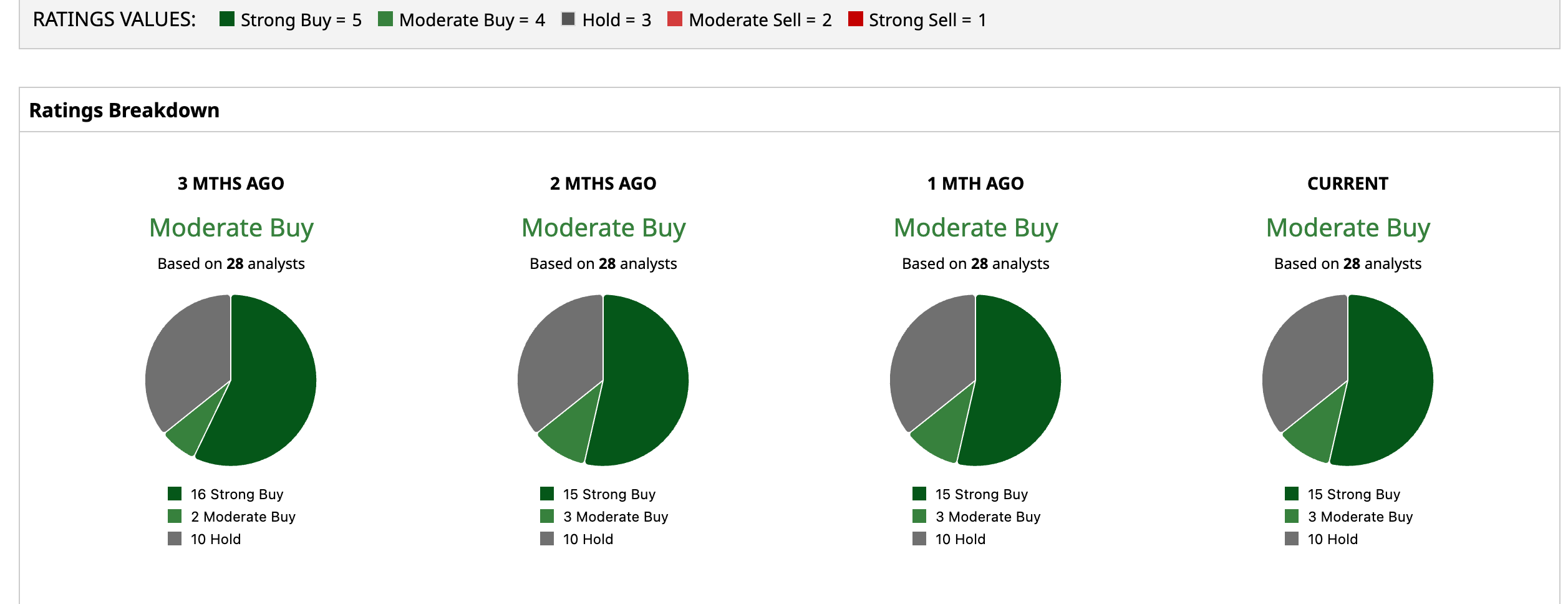

KLA Corporation has become a popular name on Wall Street, with analysts awarding it a consensus “Moderate Buy” rating overall. Of the 28 analysts rating the stock, 15 analysts have given it a “Strong Buy” rating, three analysts rated it “Moderate Buy,” while 10 analysts are taking the middle-of-the-road approach with a “Hold” rating. The consensus price target of $1,890.54 represents a 10.32% downside from current levels. And, the Street-high price target of $2,100 indicates a marginal .40% downside.