Financial guru Dave Ramsey believes you can save $22,995 over 30 years by skipping coffee. Meanwhile, financial coach and author Ramit Sethi thinks skipping coffee isn't how millionaires got there.

Ramsey and Sethi have helped countless clients get out of debt, budget efficiently, and achieve life goals like buying a house or saving for retirement. However, their perspectives on living a rich life and how to get there from scratch are unique.

Both Had Money Losses Before Bouncing Back

With real estate and finance specialization, Ramsey lived a rich life before all hell broke loose. By age 26, he was $4 million in real estate debt and moved to file for bankruptcy in 1988.

A few years later, in 1992, he started his first radio show, "The Money Game", at a struggling radio station, which later became "The Dave Ramsey Show." He never looked back after that.

Meanwhile, Sethi came from a middle-class family and had to rely on grants and scholarships to complete his education at Stanford. While he managed to earn enough to get by, he invested his first scholarship check in stocks to lose half of it immediately.

As a student of technology and psychology, he understood early on that money is a mental game, and financial stability is about saying "yes" to your money and not restricting yourself for life to reach that golden retirement day.

Buying vs. Renting A House

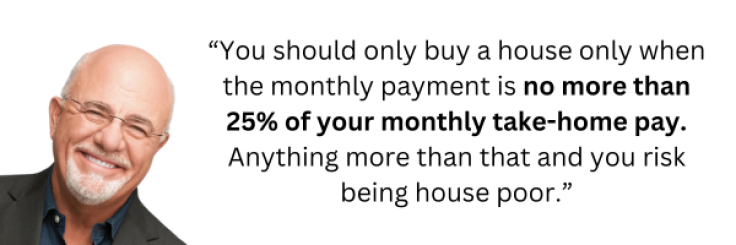

One of the most debated topics today is whether you should buy or rent a house, as prices for both have skyrocketed in this new decade. Ramsey believes in the American Dream of buying a home for the long-term, but only when you are ready.

He means you should be able to buy a house with an excellent down payment on no more than a 15-year fixed-rate mortgage, capped at 25% of your take-home salary.

Ramsey explained that when you rent, the monthly payment is higher than your landlord's mortgage payment because the owner has to make money after clearing all liabilities.

He added that as housing costs like insurance premiums and repairs mount over time, the landlord makes up for it by bumping the rent on the next lease renewal.

Meanwhile, Sethi, the host of Netflix's "How To Get Rich," believes you can lose money even if you sell a house at a profit due to "phantom costs," like taxes, insurance, maintenance, repairs, agent fees, and closing costs.

The average US homeowner was estimated to have spent over $13,000 on home improvements, maintenance, and emergency costs last year.

Sethi believes renting is cheaper than buying a house in many US cities. He believes that the American dream of owning a single-family rental with a family and a dog is decades of marketing efforts by the government and real estate institutions.

Although Sethi will buy a house in the future, which would be a "terrible decision," he enjoys the limited liabilities of renting. He would only purchase if the "numbers" make sense.

If you plan to buy a house to rent it out, Sethi urged buyers to look at the downpayment as a costly purchase first before thinking of it as an investment.

Getting Out of Debt

Ramsey has helped countless people pay off over $1 billion in debt in the last few decades. His favourite approach is the debt snowball method rather than the avalanche method.

He argues that finding motivation by clearing debt fast is sometimes more important than repaying the highest-interest credit card debt, which can take a long time.

The snowball method is clearing the smallest outstanding debt regardless of interest rates. When you clear the smallest one quickly while making monthly minimums for the rest, you use that extra money for the following loan account.

When you see real progress, like reducing your loan accounts, it can boost your motivation to attack the next loan with more commitment.

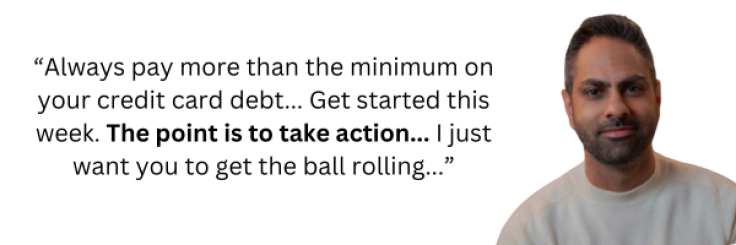

As a psychology graduate, Sethi's view on debt repayments aligns with Ramsey's approach. While he also favours the snowball repayment method for clearing debt, Sethi urged clients to work towards repaying more than the monthly minimum on all debt whenever possible.

He experienced that most people need to learn how much they owe or where the money for repayments comes from. Sethi also explores ways to reduce the debt burden, such as negotiating interest rates with creditors for temporary relief.

It can save you thousands of dollars in interest payments if they agree. He believes in taking action rather than perfecting it because once you get the ball rolling, you can always tweak it when required.

Budgeting Approach

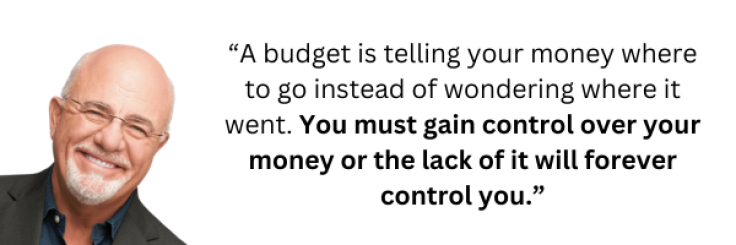

Ramsey's take on budgeting is pretty straightforward. You focus on detailing your monthly cash inflows and outflows covering your four walls: food, shelter, utilities, and transportation.

From his experience, Ramsey believes that setting aside 10% of your income to give away to charities or similar causes is a great way to start budgeting with the right spirit of generosity.

For him, it is vital to stay accountable for your money moves and urges everyone to compel their partners to vote on financial decisions because it matters in the long run. One pro tip he shares is that every month is different, and one should create a new budget every month with the necessary changes.

While having a new budget every month helps you understand your money-saving progress and associated behaviours better, you also ensure having accounted for unplanned expenses that can crop up in time.

Meanwhile, Sethi's approach to budgeting is more about spending on what you love and mercilessly cutting down on things you don't. He believes budgeting shouldn't be depriving yourself but more on avoiding things that don't matter.

Sethi's conscious spending plan (CSP) ditches the spreadsheets and budgeting apps to give you a new perspective on money.

He believes this strategy is about spending first while avoiding the feeling of dread and guilt. His CSP covers a guilt-free spending part, which can be challenging to prepare for and minimize, like getting that extra cocktail at happy hour or boarding an Uber despite a surcharge.

He believes setting aside 20%-30% of your net pay for these expenses helps better manage surprise bills and liquidity crunch. Sethi understands that deciding how much you will spend works better than planning how much you want to save so that all non-negotiables are taken care of without leaving out the fun stuff.

Retirement Planning

Ramsey experienced that most people on track to reach their retirement goals have a plan they have worked hard to stick with for a long time. These people are focused, have weathered stressful market upheavals, and can clearly understand when to retire, what they want, and how much money is needed to fulfil those obligations.

Ramsey assumed that investing 15% of a $56,000 annual gross income in decent growth-stock mutual funds via tax-advantaged retirement vehicles like 401(k)s or Roth IRAs over 25 years can create a tax-free corpus of $1.1 million.

You also avoid taxes on withdrawals. He described the fear, anxiety, and impulsiveness around kids' college fees, monthly expenses, and market volatility as constants, but one must persevere to invest for retirement regardless, diligently. It's a marathon, and patience becomes your greatest strength.

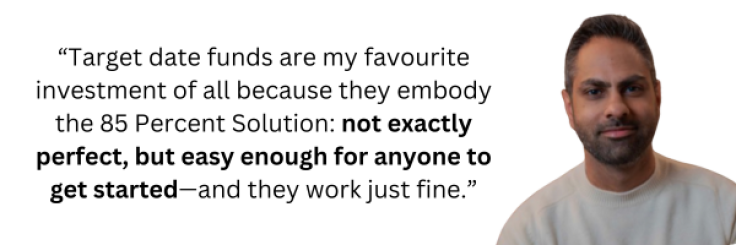

On the other hand, Sethi is a big fan of target-date funds regarding retirement investing. He said you only need to know the date you want to retire, and "the computer knows how old you are; it knows roughly when you're going to retire — let's say 65 [years old] — and then it creates a nice portfolio for you."

Target-date funds distribute your cash in multiple assets like stocks, bonds, and cash markets to help you build a giant enough egg nest for retirement by the date you choose. In turn, portfolio diversification also minimizes your exposure to market volatility.

Sethi loves them because they are simple to invest in, don't require an understanding of stock technicals, and charge as low as 0.2% as investment fees relative to the 2% on traditional investment vehicles. Hence, it is suitable for new investors.