Last year, a British oil exploration company and a tech start-up joined forces on a project to permanently lock away untapped fossil fuel reserves in Greenland.

The idea was simple: the energy company, Greenland Gas and Oil, would not extract oil from an area on the east coast that it had exploration licences for. Instead it would monetise keeping the oil in the ground via a partnership with the tech company, Carbonbase, which works on offsetting carbon emissions.

The mechanics were more complex. The partnership aimed to sell NFTs, digital collectibles that come with ownership certificates, linked to the unexplored land. The profits would then be used in part to compensate the energy company and the oil would stay underground. And, since the Greenland government had stopped issuing new exploration licences, the energy company would not be able to simply apply for another and tap a different part of the country.

The pitch to buyers was that they could be sure their NFT investment was doing some environmental good. The tokens would also be paired with a new type of “non-production” carbon credit the venture hoped to develop, which owners could use to compensate for their own emissions.

But, after months of discussions, the partnership ran into problems. Carbonbase and Greenland Gas and Oil did not agree on how to structure the joint venture. Carbonbase also discovered that the country of Greenland had never successfully produced any oil, a fact that they said undermined the whole idea. Pursuing the project “would have destroyed our public reputation” and looked like “greenwashing”, says Max Song, founder of Carbonbase.

Eric Sondergaard, chief operating officer at Greenland Gas and Oil, concedes the scheme was not “perfect” and that it would have been better if an oil producing company was “turning off the flow of oil or gas from a wellhead”. But, he says, it was easier for a group not yet tapping reserves to win investor backing for such a proposal: “once the [oil] development wheels are in motion, it is harder to convince shareholders to opt for a blockchain alternative.”

The attempt is just one example in a mass of tech ventures that hope to fuse concerns about global warming with the public’s interest in Web3 technology. A surfeit of start-ups have burst on to the scene this year, variously promising to “green” bitcoin, make NFTs sustainable and solve niggling problems in carbon markets once and for all.

These projects range from the relatively mundane to the outlandish and wacky, with interest coming from major corporations as well as fringe groups. One River Digital Asset Management launched “the world’s first carbon-neutral crypto asset fund” last year, while the world’s largest meatpacking group, JBS, has developed a blockchain platform to trace its cattle supply chain in an effort to combat deforestation. Diamond miner De Beers is using blockchain technology to track the provenance of its gems.

Many new initiatives focus on the booming market for carbon offsets — each of which is supposed to represent a tonne of carbon permanently removed or avoided from the atmosphere. They have soared in popularity in the past 18 months as companies seek to compensate for their emissions. WeWork founder Adam Neumann’s venture Flowcarbon, which received funding from Andreessen Horowitz earlier this year, is one of a range of efforts to produce carbon tokens, which can either be used to compensate for emissions like traditional carbon credits or traded on certain crypto exchanges.

The trend for “tokenising” carbon offsets, or converting them into the sort of fungible, digital tokens familiar to crypto traders has been notable: millions of credits have been digitised since late 2021.

Used well, analysts say Web3 technologies could bring greater integrity to the carbon market and help verify the credentials of products labelled as “sustainable”. But critics say complicated new initiatives could just as easily exacerbate existing problems in two unregulated markets (offsets and crypto finance), lure more people into a space with its own big emissions problem, and contribute to more greenwashing.

William Pazos, cofounder of AirCarbon Exchange, says some new groups are not displaying “the level of rigour that’s necessary” to come up with credible climate solutions. “They are ticking the boxes: the climate box, the blockchain box — all these buzzwords that potentially could make them very wealthy.”

A messy market

It was only a matter of time before advocates of blockchain — the distributed digital ledgers on which cryptocurrencies run and that have been hailed as solutions to everything from poverty to identity theft — turned to climate change.

These supporters say the technology, which keeps an unchangeable record of transactions, can bring greater clarity to the messy market for carbon offsets. “Distributed ledgers are going to help with transparency” and with tracking the purchase and use of credits, says James Cameron, policy adviser at Systemiq, the advisory group. Carbon-crypto initiatives might also be a way for retail buyers, who have traditionally found it difficult to buy offsets, to access the market.

But Pete Howson, who researches environmental technologies at the UK’s Northumbria University, says he fears some tech pioneers “don’t understand the way the carbon market works”.

The sector is notoriously complicated, with its own well-rehearsed problems: a lack of liquidity, opaque pricing and concerns about the quality of credits. Since the late 1990s the decentralised market has only become more complicated as it has grown. Thousands of projects that generate offsets exist, such as tree planting schemes that can sell credits either directly to end users or via middlemen. Different project types are governed by various complex rules, set by one of a number of third-party carbon offset standard setters such as Verra.

Some offsets are of a reliable quality, but others may not deliver the climate benefits they promise. That makes it hard for non-experts to know what to buy, who to buy from and what to pay.

The blockchain community is the latest to take up the gauntlet. Tokenising credits has become a popular starting point. The process can involve some mystifying jargon, but the goal tends to be the same: the creation of digital versions of existing offsets that are simpler for people to understand, more liquid and transparently priced.

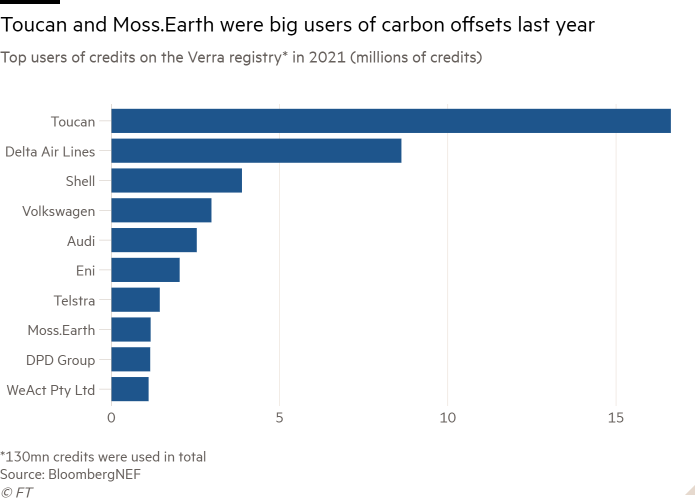

Carbon tokens have been launched by companies including Toucan, JustCarbon and Moss.Earth. Hype about the prospect of the tokens has bubbled up on social media. But the tokens have also drawn the attention of corporate investors: last year Anthony Scaramucci’s alternative investment firm SkyBridge Capital bought nearly 40,000 of Moss.Earth’s tokens to offset the “historic carbon footprint” of its bitcoin holdings.

Adrian Rimmer, cofounder of JustCarbon, says the design of carbon tokens is easier for non-expert buyers to understand than the traditional offset market, which he describes as “horrible”. “It requires an unfeasibly large amount of knowledge,” he says.

And while traditional offsets can come from thousands of different environmental projects and are difficult to compare, each of the new digital tokens on offer — JustCarbon’s JCRs or Moss.Earth’s MCO2s, for example — are uniform and trade at the same price. Each company decides on a range of offsets, such as any from forestry schemes, that can be converted into its standardised token.

‘No idea what you’re buying’

Not everyone is convinced. Louis Redshaw, managing director of carbon consultancy Redshaw Advisors, says adding another layer of complexity to the already confusing carbon market is probably “not making it better”. Blockchain may be no more useful for elucidating the process than “a good spreadsheet”, he says. Redshaw insists the complicated nature of many projects is reason enough to be wary: “If you can’t understand what it is you’re getting into you shouldn’t get into it,” he says.

Steve Zwick, a senior media relations manager for Verra, the offsets registry, says creating standardised tokens from a broad category of offsets masks key information, such as which project a credit came from. Such details are important, since some offsets are of dubious quality. “That transparency element is critical, especially now with new buyers coming in. You’ve got to make sure the labelling is right,” says Zwick.

While buyers of Moss.Earth’s tokens know they are underpinned by credits from a list of forest protection schemes published by the company, they do not know which specific project a given token is linked to. The group said its design ensured token fungibility.

Last year Vaughan Lindsay, chief executive of offset seller Climate Impact Partners, told the Financial Times that efforts to make credits fungible “remind me of collateralised debt instruments . . . If you keep rolling stuff up, you have no idea what you’re buying.”

Another risk is the temptation to use the tokens for financial speculation. Offsets are supposed to be bought to compensate for specific emissions, rather than endlessly traded. But the owners of tokenised credits can easily be swept up in the powerful currents of decentralised finance.

Verra banned the tokenisation of certain credits in May. In August it launched a consultation about designing “anti-fraud measures” for crypto-carbon — new rules that could allow tokenisation to resume.

Toucan’s tokens soared in popularity at the end of last year, largely because buyers can convert them into a new cryptocurrency, Klima. But experts pointed out that many of the millions of credits underpinning Toucan’s tokens had remained unsold for years due to quality concerns. Toucan said it had tightened up its rules about which credits could be tokenised.

“If people are bundling credits and selling them, what’s important is the underlying credit,” says William McDonnell, chief operating officer of the Integrity Council for the Voluntary Carbon Market, an industry group that is drawing up rules for what constitutes a “good” credit. “Whether it’s tokenised or not, what’s important is the quality of the credits.”

Fiorenzo Manganiello, a professor of blockchain technologies at Geneva Business School, warned of scams targeting those looking for “green” crypto. “I’ve been approached three or four times by people saying they’re selling ‘green’” tokens they claimed were backed by carbon credits, he says. “In reality, they [looked like] a pump-and-dump scheme.”

Then there is the broader threat posed by a turbulent crypto market, which crashed this year. The value of Toucan’s “BCT” tokens fell from a high of nearly $9 last year to around $1.50 in August. Moss.Earth’s MCO2s dropped from more than $17 in January to under $4 this month, while JustCarbon’s JCR moved from nearly $40 in May to around $24 in August.

The emissions elephant

The crypto-climate crossover goes beyond carbon tokens. Shoppers can now participate in metaverses where they are encouraged to purchase virtual versions of fashion items such as clothing, instead of buying in the real world.

Conservation-linked cryptocurrencies are also appearing, such as one developed by Estonia-based Single.Earth. The group generates “Merit” tokens, which landowners earn each time they store 100kg of carbon in their forests. Their woodland must be at least 20 years old to be eligible, and Single.Earth monitors the process using satellites and machine learning.

However, since there is no penalty for landowners who later cut down the trees, except that they do not earn more tokens, the stored carbon could be released back into the atmosphere. Merit Valdsalu, Single.Earth co-founder, concedes this is a concern, but says she hopes the prospect of earning more tokens will incentivise landowners to keep trees standing.

The elephant in the room is the energy consumption involved in many crypto and blockchain transactions. Minting bitcoin, for example, requires huge computing power, which often runs on coal-generated electricity. That issue is drawing more attention. This year, the US Office of Science and Technology Policy called for evidence on the energy and climate implications of digital assets.

Enthusiasts have pushed back against this characterisation of crypto, arguing that many coins and blockchains are much less energy intensive than bitcoin. But the perception of digital assets as a gas-guzzling, carbon generating problem is so prevalent that an NFT auction by the UK arm of conservation charity WWF was abruptly cancelled in February following a backlash.

Despite such criticisms, many analysts do see a role for digital technologies in the fight against climate change and are encouraged by the interest in sustainability from some in the crypto community. The “recognition of the energy conundrum by major players . . . could signal a turning point for the crypto market in adapting greener algorithms,” wrote HSBC analyst Camila Sarmiento.

Banks and exchanges are exploring a middle ground between the traditional carbon market and the crypto-carbon crossover. AirCarbon Exchange has designed smart contracts that could allow credits to be sold in smaller quantities than one tonne of carbon. That could be useful for people making small, regular purchases, such as offsetting a taxi trip, says Pazos. “Just like we see calories counts on food [packaging], we’re going to see carbon counts on all types of different activities.”

Lenders including NatWest, Standard Chartered and BNP Paribas have developed a blockchain-based settlement platform, Carbonplace, which aims to make buying offsets simpler and enhance the traceability of transactions. Buyers receive tokens representing credit ownership, which include the details of the offsets — not digital versions of the credits.

Even the UN Framework Convention on Climate Change has taken an interest: it supported the creation of the Climate Chain Coalition initiative in 2017, which works to “advance blockchain . . . and related digital solutions” to mobilise climate finance and action on climate.

But for now, the proliferation of new companies and the “low barriers to launching new projects” make it “hard to understand who you want to work with,” says Claudia Herbert, from the advisory group Carbon Direct. “We’re seeing the lessons of the [real-world offsets market] being relearnt.”