Crown Castle Inc. (CCI), headquartered in Houston, Texas, owns, operates and leases more than 40,000 cell towers and approximately 90,000 route miles of fiber supporting small cells and fiber solutions across every major U.S. market. Valued at $39.4 billion by market cap, the company manages and offers wireless communication coverage and infrastructure sites in the U.S. and Australia.

Shares of this leading provider of wireless infrastructure have underperformed the broader market over the past year. CCI has declined 15.2% over this time frame, while the broader S&P 500 Index ($SPX) has rallied nearly 31.4%. In 2026, CCI stock is up 1.5%, compared to the SPX’s 7.6% rise on a YTD basis.

Narrowing the focus, CCI’s underperformance is also apparent compared to the Pacer Benchmark Data & Infrastructure Real Estate SCTR ETF (SRVR). The exchange-traded fund has gained about 12.5% over the past year. Moreover, the ETF’s 24.8% gains on a YTD basis outshines the stock’s single-digit returns over the same time frame.

On Apr. 22, CCI shares closed up by 1.3% after reporting its Q1 results. Its FFO of $1.02 per share surpassed Wall Street expectations of $1.01 per share. The company’s revenue was $1 billion, meeting Wall Street forecasts. CCI expects full-year FFO in the range of $4.38 to $4.49 per share.

For the current fiscal year, ending in December, analysts expect CCI’s FFO per share to decline 3.2% to $4.22 on a diluted basis. The company’s FFO surprise history is impressive. It beat the consensus estimate in each of the last four quarters.

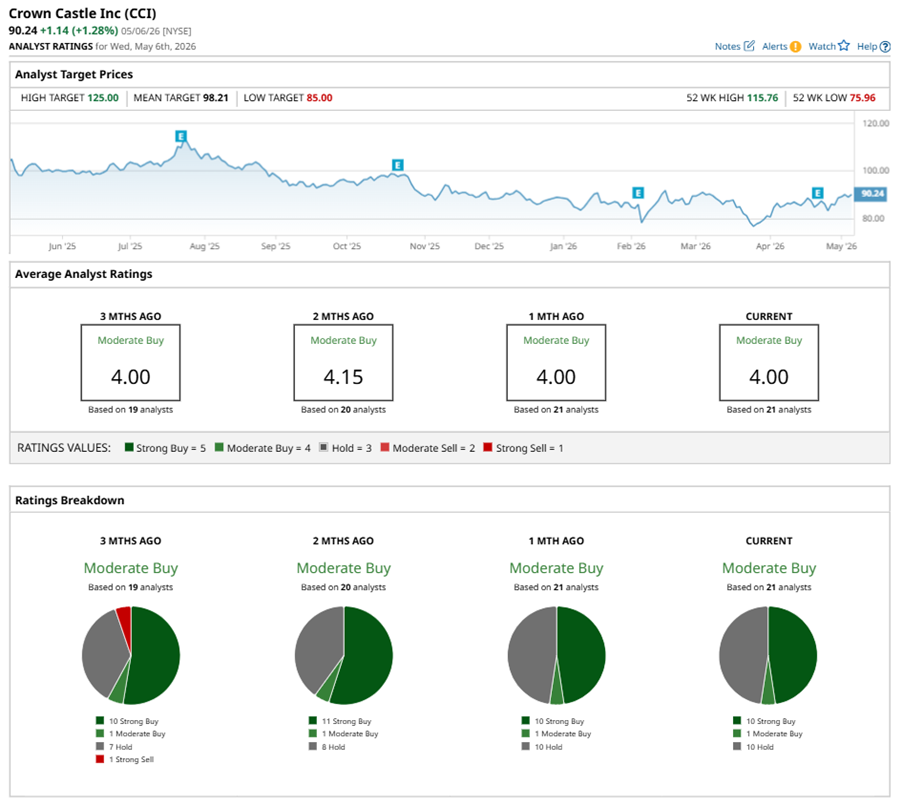

Among the 21 analysts covering CCI stock, the consensus is a “Moderate Buy.” That’s based on 10 “Strong Buy” ratings, one “Moderate Buy,” and 10 “Holds.”

This configuration is less bullish than two months ago, with 11 analysts suggesting a “Strong Buy.”

On May 6, Truist Financial Corporation (TFC) analyst Matthew Niknam kept a “Hold” rating on CCI and raised the price target to $95, implying a potential upside of 5.3% from current levels.

The mean price target of $98.21 represents an 8.8% premium to CCI’s current price levels. The Street-high price target of $125 suggests a notable upside potential of 38.5%.