With a market cap of $24.3 billion, Corpay, Inc. (CPAY) is a global payments company that helps businesses and consumers manage vehicle-related expenses, lodging, and corporate payments across the United States, Brazil, the United Kingdom, and other international markets. It offers a wide range of solutions, including fuel and fleet payments, AP automation, virtual and corporate cards, cross-border payments, and workforce lodging services.

The fuel card and payment products provider's shares have lagged behind the broader market over the past 52 weeks. CPAY stock has decreased 8.2% over this time frame, while the broader S&P 500 Index ($SPX) has rallied 11.7%. However, shares of the company are up 15.4% on a YTD basis, outpacing SPX’s marginal return.

Looking closer, shares of the Atlanta, Georgia-based company have underperformed the State Street Financial Select Sector SPDR ETF’s (XLF) 1.3% rise over the past 52 weeks.

Shares of Corpay climbed 11.6% following its Q4 2025 results on Feb. 4 after the company posted a strong earnings beat, with revenue rising 21% year-over-year to $1.25 billion, organic revenue growth of 11% for the third straight quarter, and adjusted EPS up 13% to $6.04, all exceeding expectations. The results highlighted robust underlying demand, led by 16% organic growth in the corporate payments segment despite a 200-basis-point headwind from lower interest rates.

For the fiscal year ending in December 2026, analysts expect Corpay’s EPS to grow 21.5% year-over-year to $24.56. The company’s earnings surprise history is promising. It beat the consensus estimates in the last four quarters.

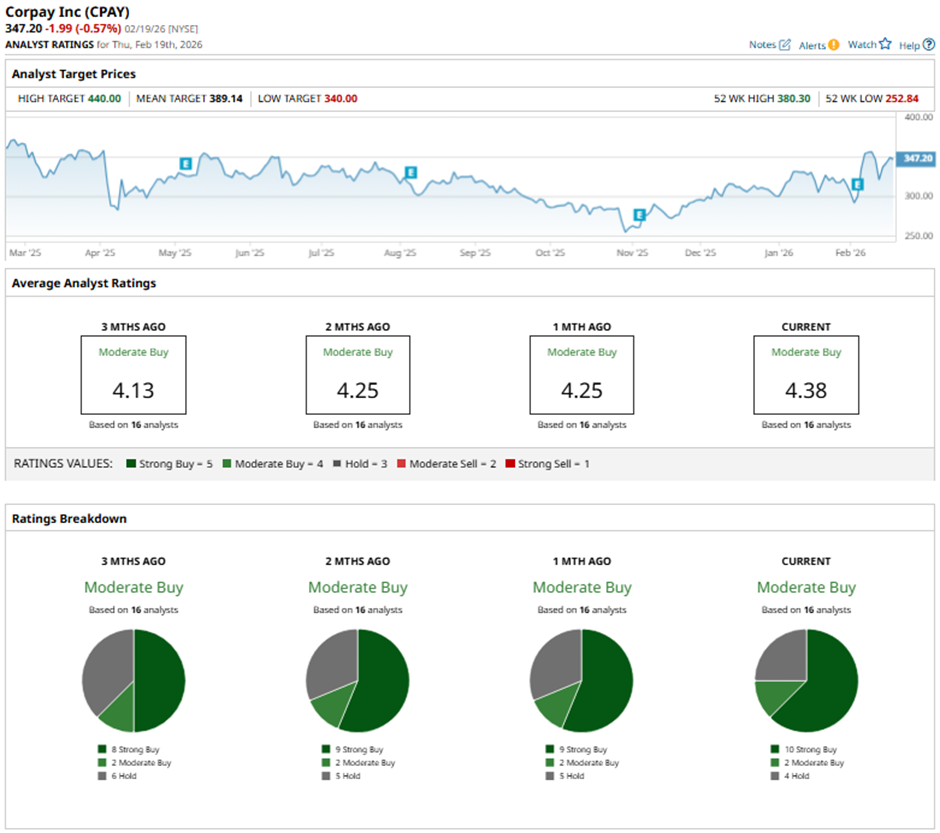

Among the 16 analysts covering the stock, the consensus rating is a “Moderate Buy.” That’s based on 10 “Strong Buy” ratings, two “Moderate Buys,” and four “Holds.”

On Feb. 5, RBC Capital raised its price target on Corpay to $363 and maintained a “Sector Perform" rating.

The mean price target of $389.14 represents a 12.1% premium to CPAY’s current price levels. The Street-high price target of $440 suggests a 26.7% potential upside.