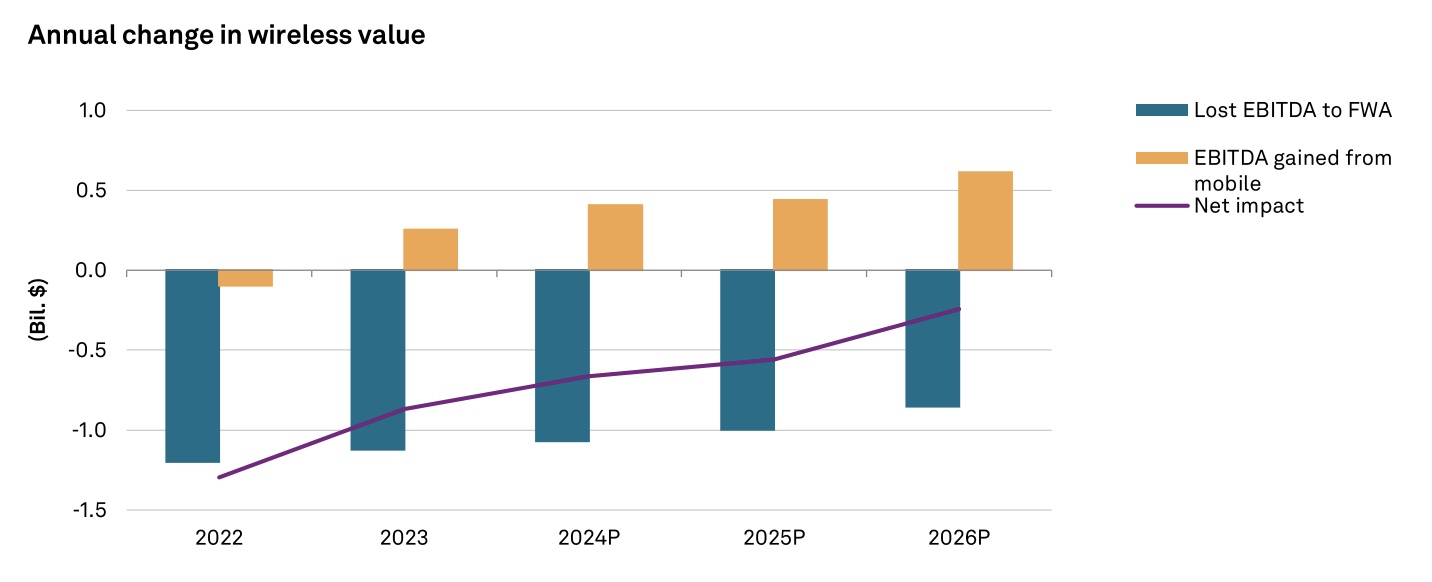

A report published Monday by S&P Global Ratings suggests that the revenue lost for cable operators from customers opting for Fixed Wireless Access (FWA) services is greater than the gains generated from new "junior cable" mobile services.

S&P analyst Chris Mooney said that, amid this dynamic "wireless convergence" marketplace, Charter Communications and Comcast are “better positioned than other cable providers" that are dabbling in mobile, primarily because of their respective wholesale mobile virtual network operator (MVNO) agreements with Verizon.

These MVNO deals date back to a 2011 spectrum sale, in which Comcast, along with the erstwhile Time Warner Cable and Brighthouse Networks, sold wireless spectrum to Verizon for $3.6 billion and wholesale use of its network into perpetuity.

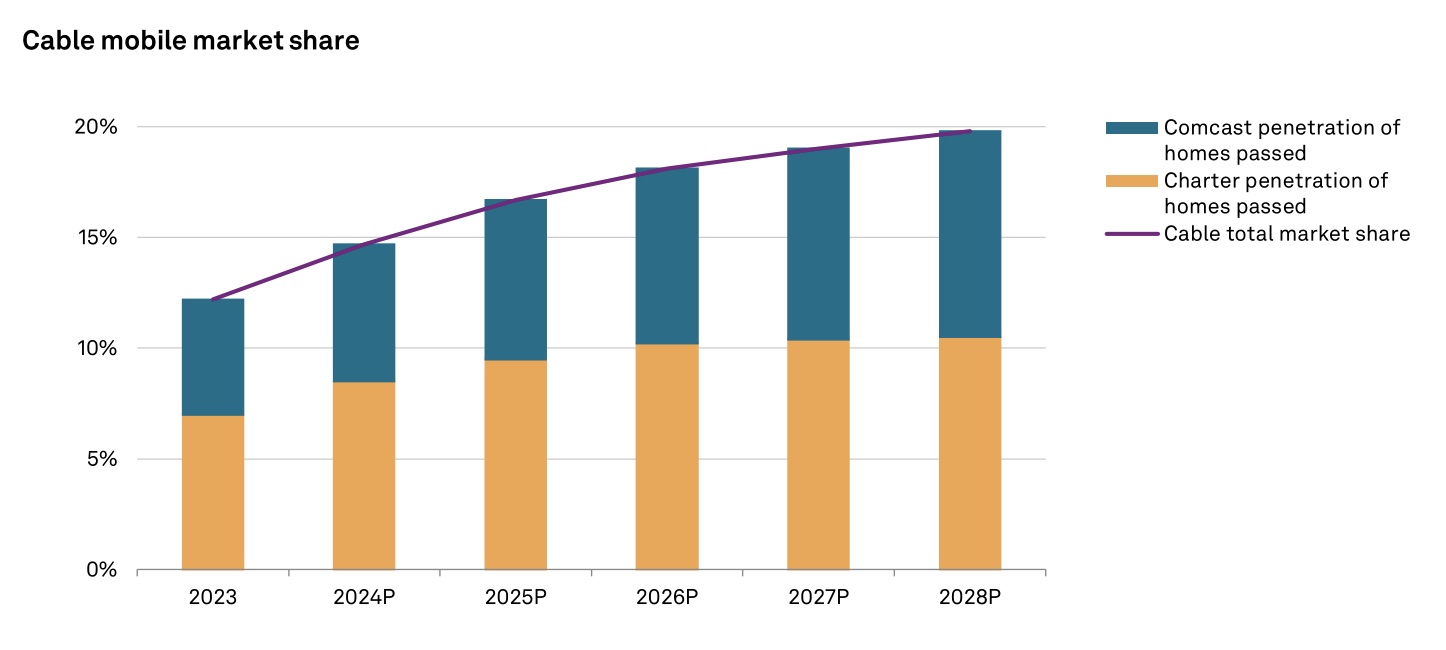

Comcast's Xfinity Mobile and Charter's Spectrum Mobile have the ability to limit how much their customers use the Verizon network and can better control costs and margins because of that. Both cable operators have robust WiFi coverage in urban areas and can offload wireless traffic accordingly. Because the two companies must pay variable fees to Verizon under the perpetual wholesale agreement, the more data they offload onto their own networks, the less expensive the MVNO costs are.

In fact, Charter states that it offloads 88% of mobile traffic onto WiFi, with Comcast even higher, at around 90% of traffic.

As Comcast and Charter develop more cost-effective ways to offload mobile traffic, their margins on mobile could eventually swell to sky-high levels, equity analyst Craig Moffett noted in his own report last November. Mooney agrees.

But smaller cable operators, Mooney said, lack the resources to develop similarly competitive wireless services.

Also Read: Charter and Comcast Rout FWA in OpenSignal’s Latest ‘Fixed Broadband Experience Report’

That could be a problem, considering wireless operators like Verizon and T-Mobile have collectively amassed more than 8 million FWA customers in the U.S. in just the past couple of years.These fixed 5G wireless home internet plans are typically cheaper compared to cable internet.

Also read: Charter CEO Chris Winfrey Dismisses FWA as ‘Cellphone Internet’

Smaller MSOs are responding to the lost wireline broadband market share and revenue by trying to turn the tables and encroach on wireless' core business. But Mooney suggested that, given their inferior MVNO economics, the "modest" margins available to them on the wireless side won't match their lost home broadband profitability.

Meanwhile, if Comcast and Charter focus on expanding their traffic offload and scale of coverage, Mooney believes that both cable giants could generate EBITDA margins as much as 15-20% in the next four years.

Charter’s aggressive, volume-focused strategy focuses on low price promotions, which helps attract and create a “stickier consumer,” according to S&P.

Comcast, however, has favored a strategy that focuses on profitability and conservative pricing over low-price promotions, is likely to generate more immediate profit and EBITDA growth.