Australia’s coal power stations will all close in 2038 – five years earlier than previously expected – and variable renewable energy capacity will need to triple by 2030 and increase sevenfold by 2050.

These are two key findings in the latest roadmap for Australia’s largest grid and electricity market, the National Electricity Market. The draft of a document known as 2024 Integrated System Plan, was released today by the Australian Energy Market Operator (AEMO). It lays out a comprehensive path for the next 20 years as we wean ourselves off coal and embrace renewables firmed by storage.

What is this plan and why does it matter?

AEMO ensures our energy market runs smoothly, including planning for the transmission needs of the future – and that’s where this blueprint comes in.

Australia’s main grid has historically been based on connecting cheap but polluting coal plants to large cities. As coal plants retire, we need a different grid, drawing renewable power from many different locations, while utilising storage.

Every two years, AEMO releases an updated plan, drawing on detailed modelling and consultation across the energy sector.

Through this process, it arrives at an “optimal development path”. That’s energy-speak for the cheapest and most effective mix of electricity generation, storage and transmission able to meet our reliability and security needs while also supporting government emissions reduction policies in the long-term interests of consumers.

Changes to our national electricity laws to include emissions reductions in its objectives came into effect in November. In response, AEMO is now only using scenarios in line with Australian Governments’ emission reduction targets.

The path laid out in this latest plan is intended to ensure the energy transition already underway will be lower cost, resilient and pragmatic. Importantly, the plan points to where we will need to build important new infrastructure – especially transmission lines – to deliver the new electricity system.

What does the update say?

The 2024 plan explores three possible scenarios:

- Step Change, which meets Australia’s emission cut commitments in a growing economy

- Progressive Change, reflecting slower economic growth and energy investment

- Green Energy Exports, framed around very strong industrial decarbonisation and surging low-emission energy exports.

The report suggests the step change scenario is the most likely of these three, closely followed by progressive change.

So what would we see under the step change scenario?

Change – and plenty of it. This scenario forecasts the retirement of 90% of Australia’s remaining 21 gigawatts of coal generation by 2034-35, with the entire fleet retired by 2038. This timeframe is five years earlier than envisaged in the 2022 integrated system plan.

AEMO notes the departure of coal from the grid could be faster still, pointing to higher operating costs, reduced fuel security and high maintenance costs as well as more competition from renewable energy in the wholesale market.

To manage the farewell to coal alongside increased electricity demand from population growth and electrification of transport, we will need to add about 6 GW of grid-scale renewable capacity every year in the coming decade. That sounds like a lot, but we’re currently rolling out almost 4 GW a year. The plan also predicts a major increase in rooftop solar – 18 GW more than in the previous plan.

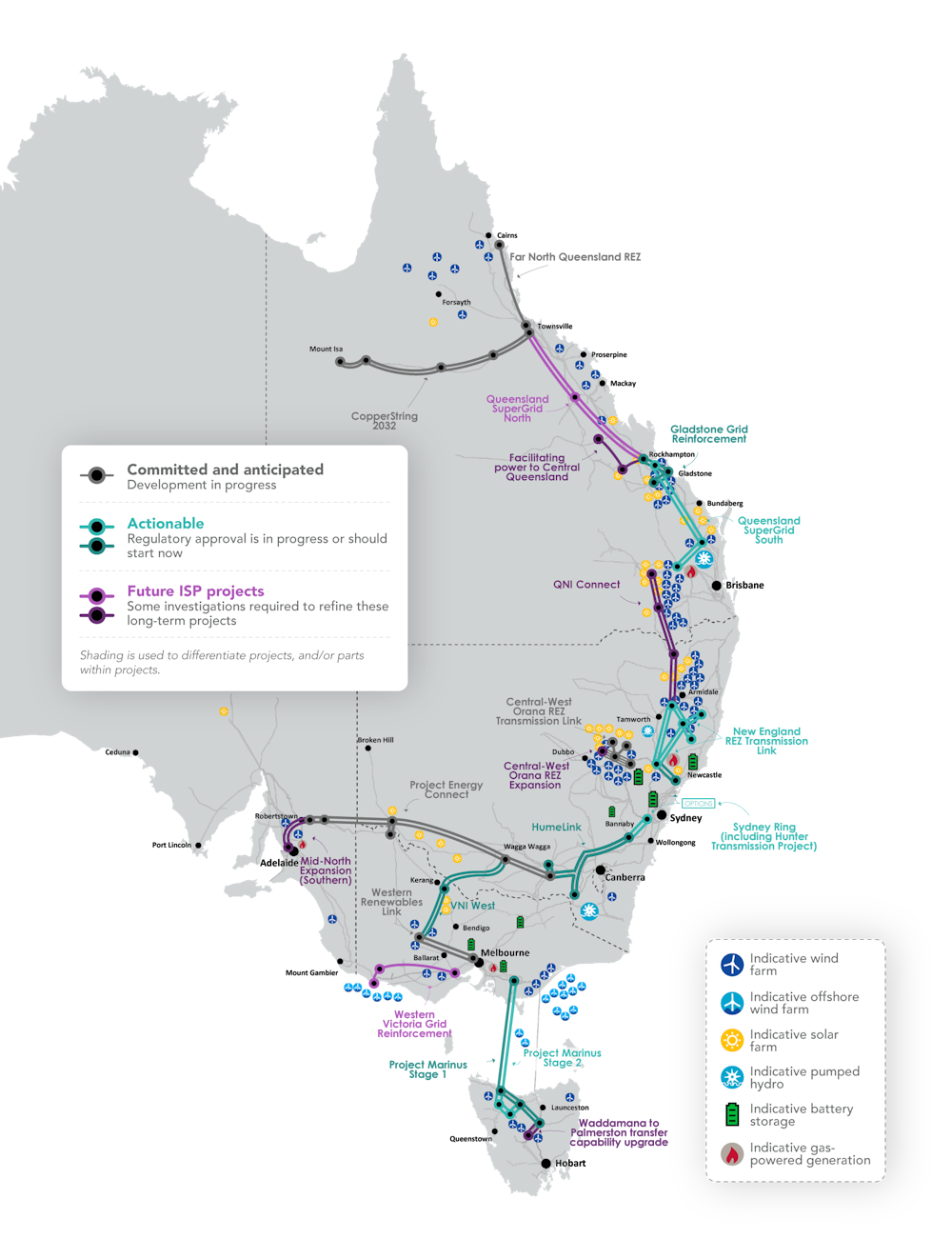

AEMO’s 2024 plan suggests close to 10,000km of new transmission lines will be needed to deliver this least-cost system by 2050. There is slightly less transmission here compared to the previous plan, due to higher transmission costs, and more power from sources requiring less transmission. Since the last plan, some minor transmission projects have been built, but the timelines for most larger projects have been pushed back.

These delays are partly due to community opposition to new transmission lines. AEMO has now explicitly flagged social license as a key challenge to delivering the new energy system.

Firming and gas

The 2024 plan calls for a quadrupling of the grid’s firming capacity, which smooths out peaks and dips in renewable generation and reduces the chance of energy shortages for consumers.

This will come from grid-scale batteries, pumped hydro, coordinated consumer batteries used as virtual power plants – and, perhaps controversially, gas-powered generation.

Under the plan, there will be 50 GW (and 654GWh) of dispatchable storage, as well as 16 GW of flexible gas.

That’s a significant boost to gas capacity, which was projected to be just over 9GW of gas capacity under the last plan.

Why do we need this capacity? AEMO pictures these gas plants not as day-in, day-out generators, but as a infrequently used backup to ensure the grid stays reliable and secure.

So this increase in gas power capacity doesn’t actually mean a increase in gas generation, or the amount of gas burnt. In fact, AEMO projects a significant decline in gas power over the short to medium term.

But from 2033, as the last coal is burned in our coal plants, AEMO does expect an increase in gas generation. This may be fossil gas, but some may be hydrogen or biomass-derived gas.

Shifting from regular use to infrequent use as a backup will pose challenges for the existing fossil gas network, AEMO points out.

Does this threaten the clean energy transition? No. If we can banish almost all fossil fuel generation from our main grid by 2034, we will be doing well. Even if this were all fossil gas – which it won’t be – the emissions intensity of Australia’s main grid would be miniscule – around 0.01 tonnes per MWh, or 60 times lower than today.

Dylan McConnell's current position is supported by the 'Race for 2030' Cooperative Research Centre.

This article was originally published on The Conversation. Read the original article.