/Charles%20River%20Laboratories%20International%20Inc_%20chart%20and%20logo-by%20IgorGolovniov%20via%20Shutterstock.jpg)

Wilmington, Massachusetts-based Charles River Laboratories International, Inc. (CRL) provides drug discovery, non-clinical development, and safety testing services. It is valued at a market cap of $7.6 billion.

Companies worth $2 billion or more are typically classified as “mid-cap stocks,” and CRL fits the label perfectly, with its market cap exceeding this threshold, underscoring its size, influence, and dominance within the diagnostics & research industry. By partnering with global research institutions and commercial disruptors, the company aims to accelerate the timeline from basic research to regulatory approval while maintaining a disciplined approach to capital allocation and operational efficiency.

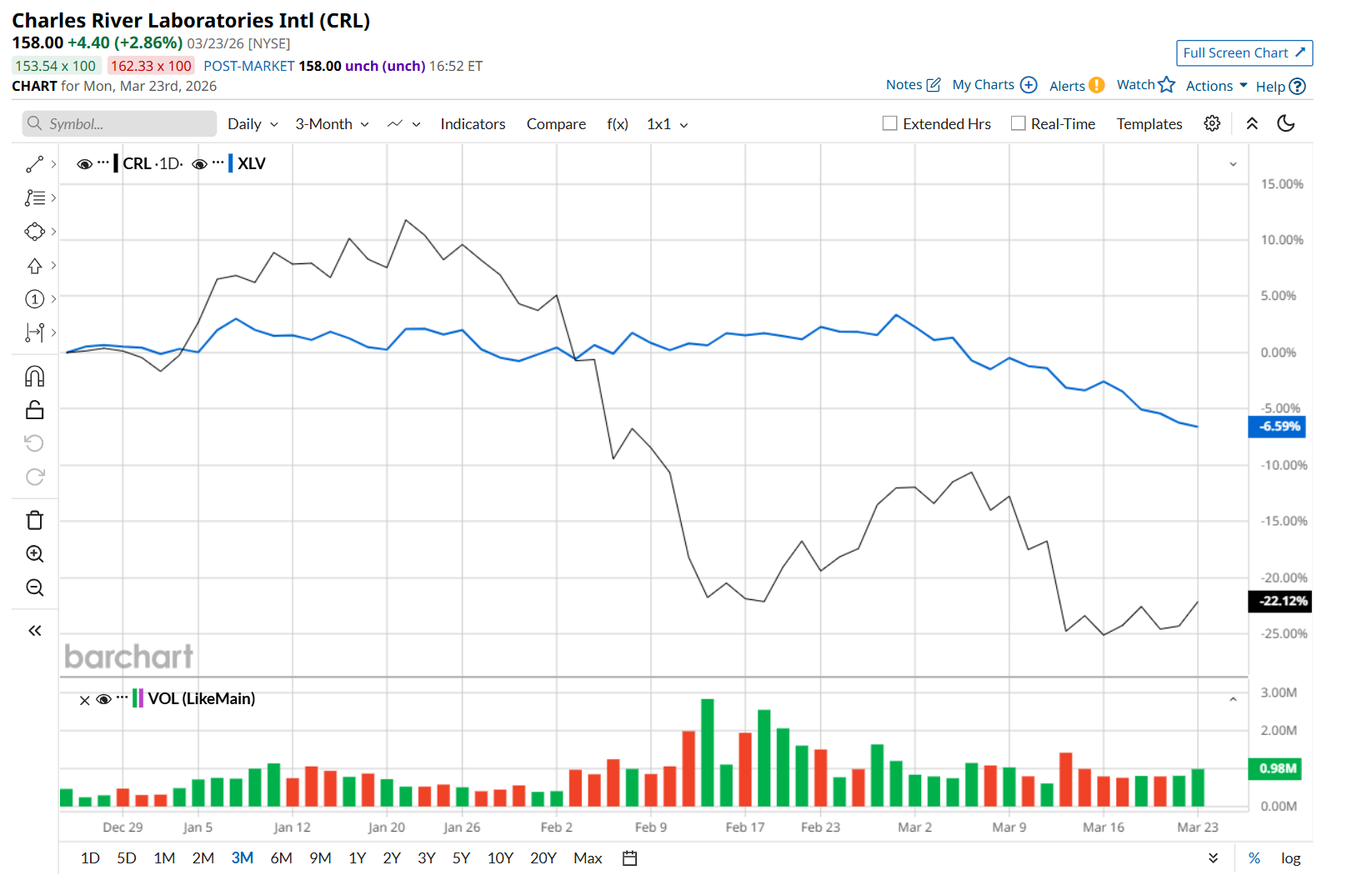

This healthcare company has dipped 31% from its 52-week high of $228.88, reached on Jan. 13. Shares of CRL have declined 22.1% over the past three months, notably underperforming the State Street Health Care Select Sector SPDR ETF’s (XLV) 6.6% drop during the same time frame.

Moreover, on a YTD basis, shares of CRL are down 20.8%, compared to XLV’s 6.5% loss. In the longer term, CRL has fallen 5.6% over the past 52 weeks, lagging XLV’s 1.3% downtick over the same time frame.

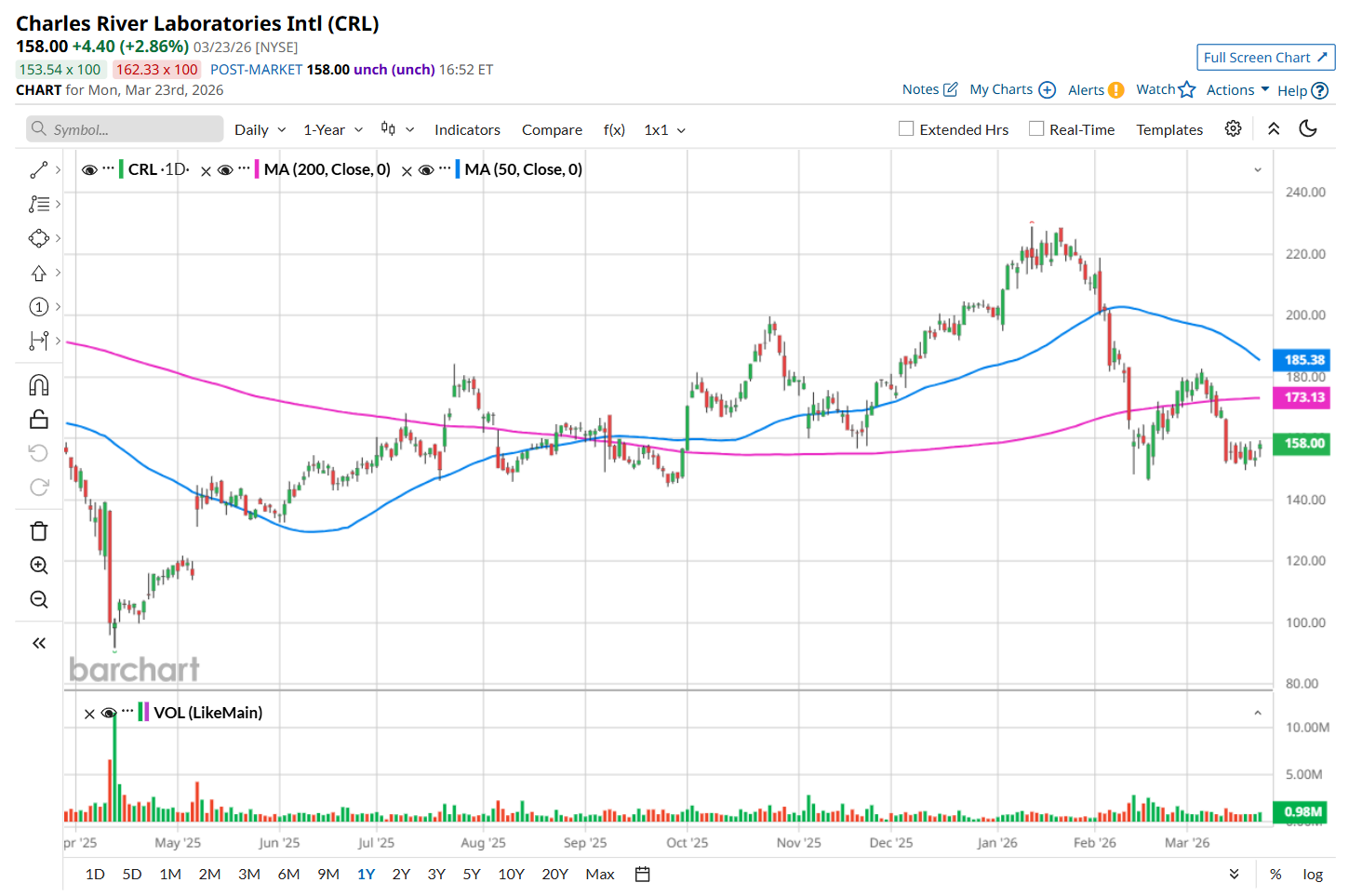

To confirm its bearish trend, CRL has been trading below its 200-day moving average since early March and has remained below its 50-day moving average since early February.

On Feb. 18, CRL shares tumbled marginally despite posting better-than-expected Q4 results. The company’s adjusted EPS of $2.39 topped analyst expectations of $2.33, while its revenue of $994.2 million surpassed consensus estimates by a slight margin. It expects fiscal 2026 adjusted EPS to be between $10.70 and $11.20.

CRL has outpaced its rival, IQVIA Holdings Inc. (IQV), which decreased 10.2% over the past 52 weeks and 25.9% on a YTD basis.

Despite CRL’s recent underperformance, analysts remain moderately optimistic about its prospects. The stock has a consensus rating of "Moderate Buy” from the 16 analysts covering it, and the mean price target of $202.36 suggests a 28.1% premium to its current price levels.