Cerebras Systems (CBRS) has cracked the code on speed. The company's wafer-scale technology runs the fastest artificial intelligence (AI) infrastructure on the planet, and fast AI prints money in ways slow AI simply cannot. The edge pulled in serious names. OpenAI and Amazon's (AMZN) AWS both came knocking, with momentum building ever since.

The OpenAI deal alone would make any investor spill their coffee in excitement. Cerebras locked in a multi-year agreement worth more than $20 billion, under which OpenAI would deploy 750 megawatts of Cerebras high-speed inference over the next several years.

The two companies also co-launched Codex-Spark together, a model purpose-built for near-instant coding and sharpened specifically for interactive work. Even so, CBRS stock dropped 10.5% in extended trading on Tuesday, June 23, as Wall Street spotted something it did not like buried inside the Q1 FY2026 results.

Cerebras projected Q2 FY2026 core gross margins of 36% to 38%, down from 47% in the prior quarter, dampening enthusiasm around an otherwise impressive earnings report. The company posted a loss of $0.22 per share on revenue of $193.4 million, outperforming analysts’ expectations for a $0.29 loss on $180.8 million in revenue.

The single figure eclipsed everything else: the blockbuster deal, the revenue surge, all of it. So, let us now see if CBRS stock still makes a worthy investment.

About Cerebras Stock

Founded in 2015, the Sunnyvale, California-based Cerebras Systems builds advanced AI computing infrastructure for data centers and supercomputer-scale deployments. The company built its name on proprietary wafer-scale processor technology, designed from the ground up to deliver significantly higher performance for AI training and inference workloads.

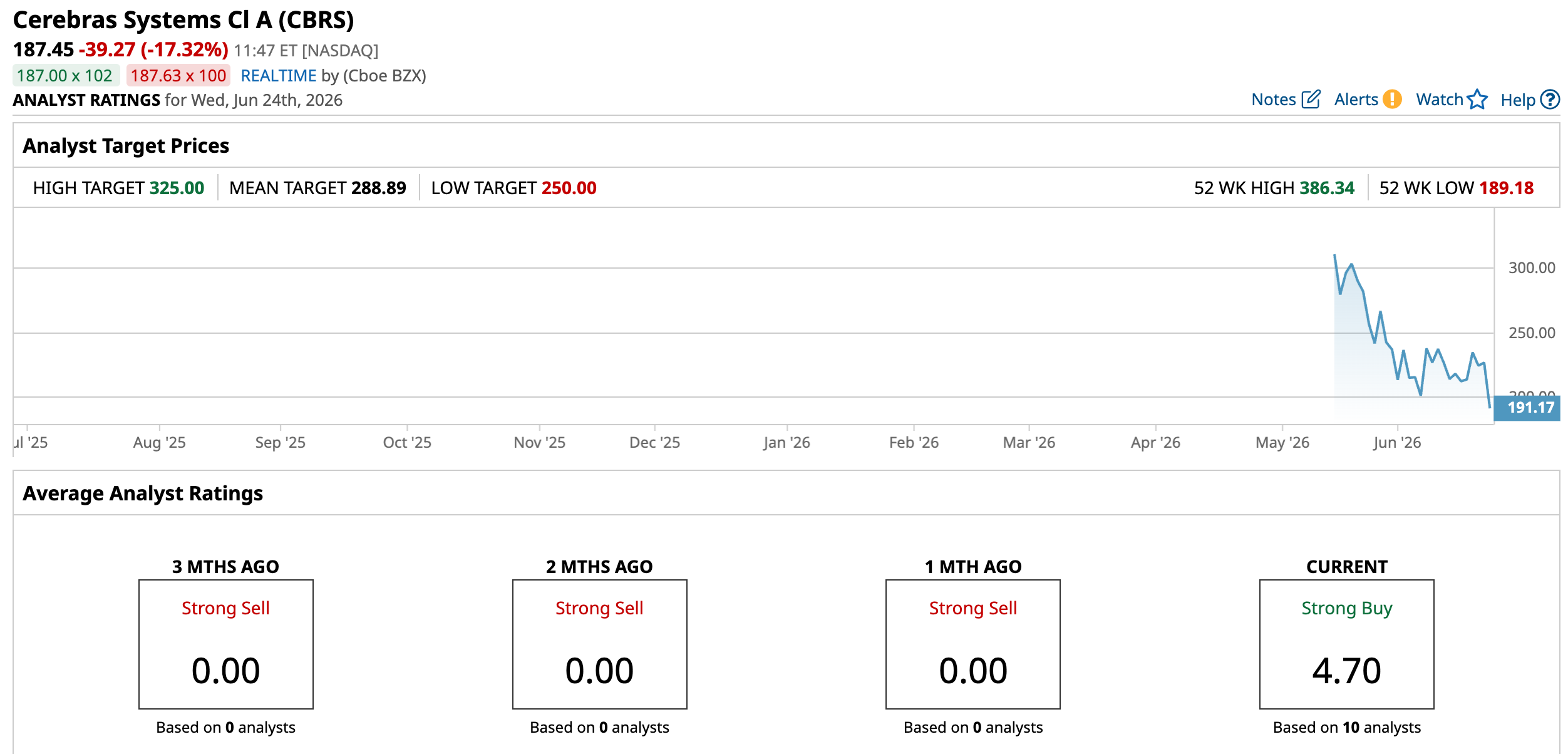

With a market cap of $48.8 billion, Cerebras is not a small bet. However, the stock's recent performance paints a bit of a tug of war. CBRS stock slipped 25.89% over the past month, and the shares have shown no signs of life lately, losing 10.34% across the last five trading sessions.

On the valuation front, CBRS stock is currently trading at 60.14 times forward sales. The multiple sits well above the broader industry average, signaling a hefty price tag on the company's growth potential despite the stock’s volatile journey.

A Closer Look at Cerebras’ Q1 Earnings

On June 23, Cerebras unveiled its results for Q1 FY2026, wherein core revenue grew 92.3% year-over-year (YOY) to $191.3 million. The breakdown told an equally strong story. Core revenue from the hardware segment rose 60% YOY to $111.562 million while revenue from the Cloud and Other Services segment rose 167.4% from the year-ago value to $79.8 million.

The profitability picture looked just as clean. Core gross profit grew 112.4% from the year-ago value to $89.1 million, pushing core gross margin to 46.5%, up from 42.1% in the prior year's period. Core hardware gross margins came in at 42% while core cloud and other services gross margins reached a healthier 52.9%.

Core operating loss narrowed 81.8% YOY to $3.5 million and core net loss narrowed 83.1% YOY to $2.5 million, both heading in exactly the right direction. Moreover, adjusted EBITDA landed at $12.7 million, swinging hard from a $15.4 million adjusted EBITDA loss in the year-ago quarter.

The balance sheet held its ground too. Cash and cash equivalents stood at $1.7 billion at quarter-end, up from $701.7 million on Dec. 31, 2025, giving the company plenty of runway to keep swinging big.

Beyond the OpenAI headline, Cerebras kicked off a multi-year partnership with AWS to bring fast inference to an even bigger scale through global distribution for every startup, AI-native company, and enterprise player, essentially planting its flag across the entire market.

Looking ahead, management projects core revenue of approximately $194 million for Q2 FY2026, up 88% YOY, with core gross margin in the range of 36% to 38% and core operating margins in the range of negative 30% to negative 32%.

For full FY2026, the company expects core revenue of $855 million to $865 million, up 69% YOY at the midpoint, core gross margin in the range of 38% to 41%, and core operating margins in the range of negative 28% to negative 32%.

On the other hand, analysts forecast full FY2026 loss per share to widen 100.1% from the prior year to $1.14. FY2027 is where the tide turns, though, with EPS expected to rebound 180.7% from the prior year to $0.92.

What Do Analysts Expect for Cerebras Stock?

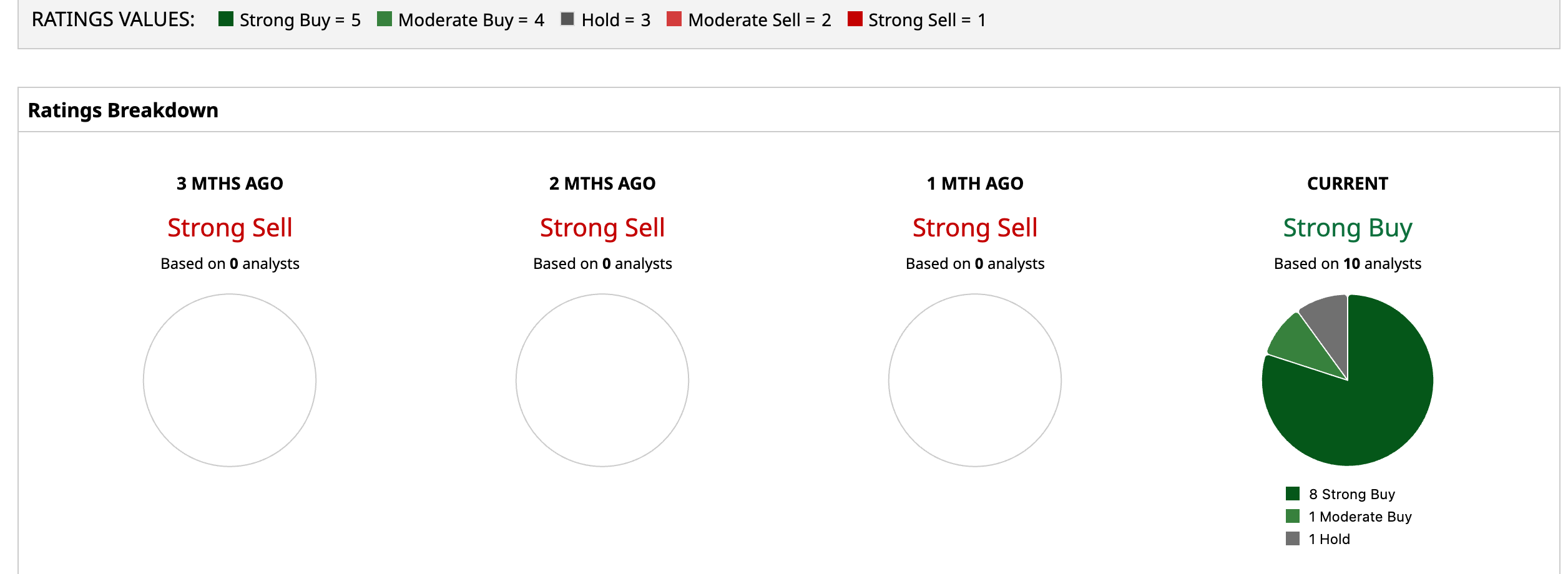

Analyst sentiment has not budged from the bullish corner. The stock is carrying an overall rating of “Strong Buy.” Among 10 analysts covering the stock, eight carry “Strong Buy” ratings, one holds a “Moderate Buy,” and one stays on the sidelines with a “Hold.”

To that end, the stock’s average price target of $288.89 represents potential upside of 54.12%. Meanwhile, the Street-High target of $325 suggests a gain of 73.4% from current levels.